Jul 18, 2026

Inflation Reduction Act: Tax Credit Opportunities

Sustainability Strategy

In This Article

Match IRA tax credits to projects, maximize bonuses, and monetize via direct pay or transfer across energy, buildings, fleets.

Inflation Reduction Act: Tax Credit Opportunities

The IRA can cut project cost by thousands - or millions - if I match the right tax credit to the right project and set up labor, sourcing, and filing rules early. For many organizations, the biggest levers are clean power credits, building deductions, fleet and charging credits, and select industry credits. Some credits can be used against taxes, some can be sold, and some can be paid out in cash to tax-exempt and public entities.

Here’s the short version:

Clean electricity: Solar, storage, and similar projects may qualify for ITC/PTC rules, now shifting to 45Y/48E for many projects placed in service from 2025 on.

Buildings:179D can provide $0.50 to $5.00 per square foot for energy-efficient commercial building work.

Vehicles:45W offers up to $7,500 for light-duty clean vehicles and up to $40,000 for heavy-duty vehicles.

Charging:30C can cover 30% of cost, up to $100,000 per unit, in eligible census tracts.

Industry: Credits like 45V for hydrogen can be worth up to $3.00 per kilogram, based on emissions rates.

Bonus rules matter: Meeting wage and apprenticeship rules can move a clean power credit from 6% to 30% or from $0.005/kWh to $0.025/kWh.

How I get the money matters: I may use the credit, sell it, or, if eligible, claim direct pay from the IRS.

A few points shape almost every IRA decision:

Timing matters. Many credits run through 2032, but rule changes started in 2025 for several clean electricity credits.

Project setup matters. Ownership, site choice, labor records, and domestic content can change credit value.

Paperwork matters. IRS registration, placed-in-service records, payroll support, and tax filings can decide whether a credit holds up.

Exchange Energy Tax Credits with the Inflation Reduction Act

Quick comparison

Area | Main credit(s) | What it does | Who should look first |

|---|---|---|---|

Clean power and storage | 48, 45, 48E, 45Y | Cuts upfront cost or pays by power output | Building owners, power project sponsors, public entities |

Commercial buildings | 179D | Deduction tied to energy savings | Building owners, architects, engineers on public/nonprofit work |

Fleet | 45W | Credit for business-use clean vehicles | Fleet managers, schools, local governments, companies |

Charging/refueling | 30C | Credit for charging equipment in eligible areas | Fleet operators, site hosts, property owners |

Industry | 45V, 45Q, 48C, 45Z | Supports hydrogen, carbon capture, fuels, manufacturing | Manufacturers and heavy industry |

If I am screening projects now, the first step is simple: map each project to one credit, test bonus eligibility, and decide early whether the value will come through tax use, transfer, or direct pay.

Key IRA Tax Credits for Clean Energy, Buildings, Transportation, and Industry

IRA Tax Credits for Clean Energy: Key Credits, Values & Bonus Opportunities

This section helps link each project type to the credit structure that fits it best. That matters early. The right credit can change whether a project moves now, comes in at a lower cost, or clears the return threshold more easily. Before you model project economics, map the project to the right credit first.

Project Type | IRC Section | Core Benefit | Bonus Opportunities | Eligible Claimants |

|---|---|---|---|---|

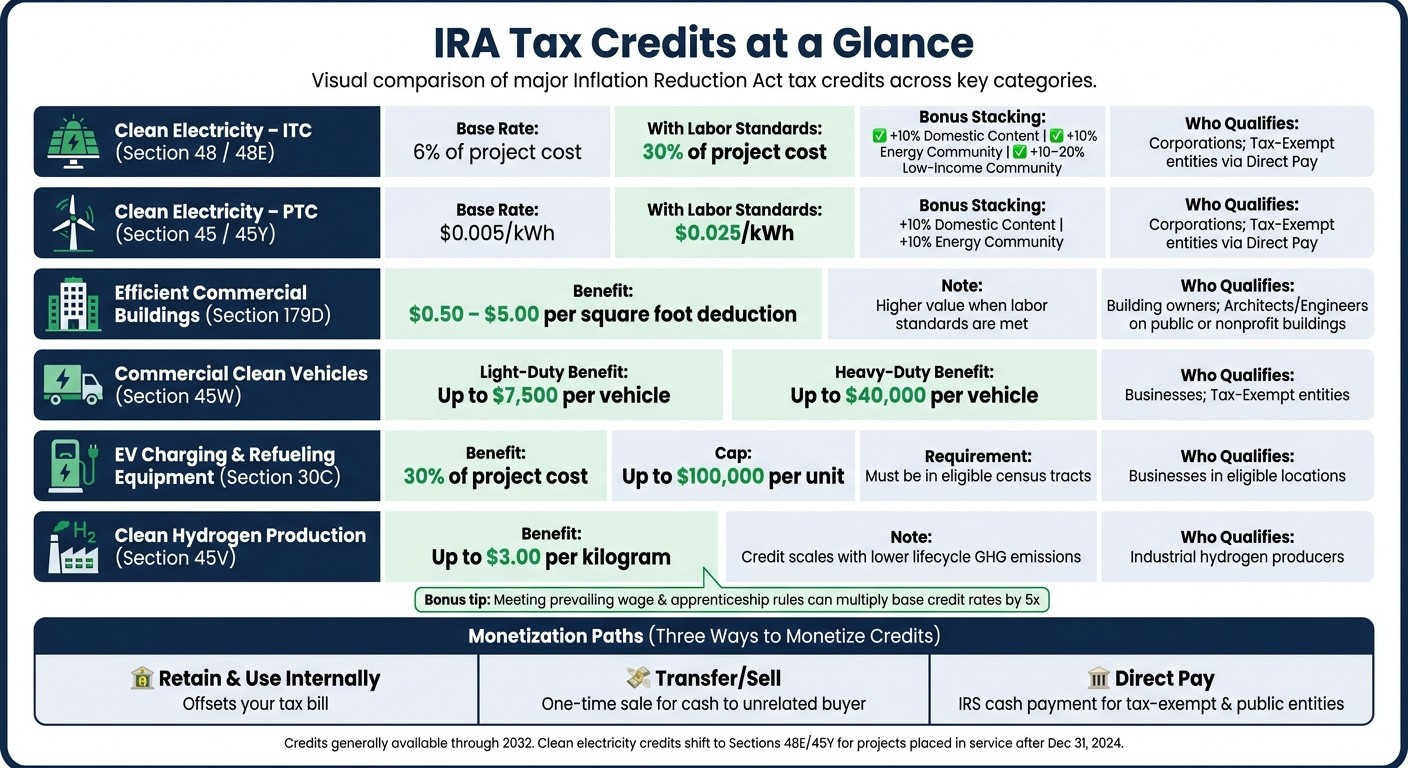

Clean Electricity (ITC) | 48 / 48E | 6% (30% with labor standards) | +10% Domestic Content; +10% Energy Community; +10–20% Low-Income | Corporations; Tax-Exempts via Direct Pay |

Clean Electricity (PTC) | 45 / 45Y | 0.5 cents per kWh (2.5 cents per kWh with labor standards) | +10% Domestic Content; +10% Energy Community | Corporations; Tax-Exempts via Direct Pay |

Efficient Commercial Buildings | 179D | $0.50–$5.00/sq ft | Higher value with labor standards | Building owners; designers for public/nonprofit buildings |

Commercial Clean Vehicles | 45W | Up to $7,500 (light-duty) / $40,000 (heavy-duty) | N/A | Businesses; Tax-Exempt entities |

EV Charging / Refueling | 30C | 30% of cost | Up to $100,000 per unit | Businesses in eligible census tracts |

Clean Hydrogen | 45V | Up to $3.00/kg | Based on lifecycle GHG emissions | Industrial producers |

Project structure shapes the payout. Some credits cut upfront cost. Others pay off over time based on output.

Clean Electricity Credits: ITC, PTC, and Technology-Neutral Credits

The Investment Tax Credit (ITC) gives an upfront credit based on eligible project costs. That often makes it a strong fit for solar, battery storage, and geothermal. The Production Tax Credit (PTC), by contrast, pays over 10 years based on actual kilowatt-hours generated, which tends to line up better with high-output assets such as wind.

On their own, the base rates are pretty small: 6% for the ITC and $0.005 per kWh for the PTC. If a project meets prevailing wage and apprenticeship rules, those rates jump to 30% and $0.025 per kWh - a fivefold increase [3]. In plain terms, capex-heavy projects often lean toward the ITC, while assets expected to produce a lot of electricity often lean toward the PTC.

Starting January 1, 2025, facilities placed in service after December 31, 2024, generally move to the technology-neutral Sections 48E and 45Y if they are zero greenhouse gas emissions facilities [3]. Projects placed in service before that date stay under legacy Sections 48 and 45. Bonus value can also stack through domestic content, energy community siting, and low-income community rules, adding +10%, +10%, and +10–20%, respectively [3].

That same screening mindset carries into buildings, fleets, and industrial assets, even though the credit mechanics shift.

Building, Vehicle, and Charging Infrastructure Credits

Section 179D applies to energy-efficient commercial buildings and gives a deduction of $0.50 to $5.00 per square foot, with more value available when labor standards are met. One detail people sometimes miss: designers working on government or nonprofit buildings, including architects and engineers, can claim the deduction directly even if they do not own the building.

These credits tend to land best when building upgrades and fleet changes are already part of the capital plan. In other words, they work well when tax planning and project planning are moving together.

For fleet managers, Section 45W provides up to $7,500 for light-duty clean vehicles and up to $40,000 for heavy-duty vehicles used for business use. Section 30C covers 30% of project cost, up to $100,000 per unit, for businesses in eligible census tracts. Paired together, Sections 45W and 30C can help support both fleet electrification and the charging buildout behind it.

Industrial and Manufacturing Credits

Hard-to-abate projects have their own credit stack, especially around hydrogen, capture, and clean fuels.

Section 45V for clean hydrogen offers up to $3.00 per kilogram. The actual credit amount depends on lifecycle greenhouse gas emissions, so lower-emissions production earns a higher credit.

Other industrial credits worth screening include advanced energy project credits under Section 48C, carbon capture incentives under Section 45Q, sustainable aviation fuel credits under Section 40B, and clean fuel production credits under Section 45Z. These tend to matter most for manufacturers and heavy industry. In that setting, the IRA is not just a subsidy. It becomes a design input for process change, fuel switching, and supply chain shifts.

How Organizations Can Monetize IRA Credits

Once a project lines up with an IRA credit, the next step is simple in theory and often tricky in practice: how do you turn that credit into dollars and cents? Most organizations have three paths. They can keep the credit and use it against their own tax bill, sell it for cash, or claim direct pay if they qualify. The best option depends on tax status, cash needs, and timing.

Feature | Retain and Use Internally | Transferability | Direct Pay |

|---|---|---|---|

Eligibility | Taxable entities with enough tax liability to use the credit | Eligible taxpayers with transferable credits | Applicable entities for most credits; certain other taxpayers for specified credits |

Cash Flow | Full credit value offsets tax liability | Cash from selling the credit | Cash payment from the IRS |

Counterparties | IRS | Unrelated buyer | IRS / Federal Government |

Key Risks | Insufficient tax liability | Eligibility, diligence, recapture, and indemnity issues | Registration and documentation errors |

Direct Pay for Tax-Exempt and Public Entities

Elective payment, often called direct pay, is the rule under IRC §6417 that allows eligible entities to receive a cash payment from the IRS equal to the value of certain credits, even if they have no federal income tax liability[5][8][11]. That said, it does not apply to every credit. Teams should confirm the exact credit section before treating a project like it can be settled in cash[10][11].

Eligible entities include tax-exempt organizations under Section 501(a), state and local governments, U.S. territories, Indian tribal governments, Alaska Native Corporations, rural electric cooperatives, the Tennessee Valley Authority, and agencies or instrumentalities of those governments[4][8][11]. That list is longer than many people expect, which is why early eligibility review matters.

The process usually begins with IRS pre-filing registration through Energy Credits Online (ECO). Each eligible project needs its own registration number, and that number must appear on the original tax return that makes the elective payment election. The IRS strongly recommends filing registration at least 120 days before the planned filing date[6][7][9][12]. In day-to-day work, the problems tend to be pretty predictable:

Missed registration timing

Mismatches between project records and tax filings

Wrong ownership or placed-in-service assumptions

Incomplete support for wage or apprenticeship rules where they apply

Transferability and Tax Credit Sales

For taxable entities that generate more credits than they can use, transferability under IRC §6418 allows certain eligible credits to be sold one time for cash to an unrelated buyer[10][13][14]. That can turn a future tax item into near-term liquidity, which is a big deal for sponsors trying to keep projects moving.

There is a firm limit here: credits can be transferred only once, and re-transfers are not allowed[13][14]. Partnerships may also qualify as eligible taxpayers for transfers, even if tax-exempt entities or other applicable entities own them in whole or in part[13].

Buyers usually want to see the full paper trail. That often includes project contracts, ownership and title records, placed-in-service support, wage and apprenticeship records when needed, basis calculations, energy-modeling or production assumptions when relevant, and legal opinions or tax diligence memos. On the seller side, it is common to see representations and warranties, escrow or reserve terms, and indemnity duties if the credit is later challenged[13][14].

Capital Planning for climate resilience and sustainability portfolios

Monetization should be built into project design from the start, not handled as a tax choice after the deal is done. The path you choose can shape debt sizing, debt service coverage ratios, grant stacking, covenant compliance, and project sequencing. A finance-and-tax model that compares after-tax returns, net present value, cash timing, deal costs, and risk allocation across all three paths is the right place to begin[10][13][14].

Ownership structure matters too. It determines who can claim the credit, who can elect direct pay if eligible, and whether the credit can be transferred. Some organizations also phase projects so that the simplest assets to qualify are placed in service first. That can bring in earlier cash flow or tax value, which may help fund later stages.

Create an IRA credit steering group early so ownership, procurement, and tax structuring are lined up before contracts are signed.

That choice should feed straight into the screening and modeling process that comes next.

Integrating IRA Credits into a Sustainability Roadmap

Once credits are modeled, the next move is portfolio design: which projects go first, and why.

IRA credits can help teams put the right projects at the front of the line - projects that cut emissions, improve resilience, and make the numbers work better. A practical place to start is a Scope 1 and 2 emissions baseline across facilities and fleets, then map Scope 3 hotspots to the projects most likely to address them.

Use the table to rank projects by emissions impact, resilience value, and readiness - not just by credit size.

Align Credits with Decarbonization and Resilience Priorities

Sustainability Initiative | Likely IRA Incentives | Key Planning Considerations |

|---|---|---|

Rooftop solar + storage | Section 48/48E, plus bonuses where applicable; direct pay for eligible entities | Confirm ownership structure and interconnection; meet prevailing wage and apprenticeship rules; integrate with resilience goals (backup power for critical loads) |

Commercial building retrofits (HVAC, envelope, electrification) | Section 179D commercial building deduction (up to $5.00/sq ft) [2][18][17] | Require pre- and post-project energy modeling to ASHRAE standards; align with science-based targets; track interactions with local building performance standards |

Fleet electrification (medium- and heavy-duty) | Use 45W and 30C together to time vehicle replacement, charging buildout, and utility upgrades | Build a fleet transition roadmap using telematics data; plan depot charging and grid capacity upgrades; coordinate with utility make-ready programs |

Hydrogen pilots | Reserve 45V for sites with a clear low-carbon hydrogen pathway and reliable emissions data | Determine production pathway and lifecycle emissions intensity; secure robust GHG accounting |

Resilient infrastructure (microgrids, backup power, critical loads) | Integrate climate risk modeling into site selection; structure projects to provide community benefits; assess long-term adaptive management |

Sequencing matters. Early waves - LED upgrades, rooftop solar, and basic controls - are often faster to permit, easier to document, and faster to turn into incentive value. That early value can help fund heavier lifts later, like industrial fuel switching or hydrogen pilots. When teams rank projects, resilience criteria should sit right beside cost of carbon abatement, including measures like critical load coverage during grid outages and storm hardening.

After projects are prioritized, the next job is protecting the credit value already on the table.

Governance, Compliance, and Reporting Controls

Getting bonus credit levels takes proof, not good intentions. A cross-functional IRA and Sustainability Steering Committee - with tax, finance, sustainability, legal, procurement, and internal audit at the table - is often the best way to keep the work moving in step. This group should set RACI roles for documentation, define investment criteria that weigh emissions cuts alongside NPV, and bring recapture, compliance, and delivery risk into enterprise risk management.

The paper trail matters more than many teams expect. Certified payroll records, apprenticeship program documentation, manufacturer certificates of origin, and component cost breakdowns should all live in one central system, with retention policies tied to IRS statute of limitations.

On the reporting side, harmonizing tax and sustainability data helps avoid a common mess: claiming emissions reductions in an ESG report that don't line up with the assumptions in a project's financial model. Standardized baselines, recognized GHG accounting frameworks like the GHG Protocol, and interval metering data help IRA-credited projects connect cleanly to Scope 1 and 2 inventories while supporting audit-ready disclosures for CDP, SBTi, or SEC climate reporting.

Execution then comes down to turning those controls into a pipeline that can actually be built and financed.

How Council Fire Can Support Implementation

Turning eligible credits into a working, multi-year decarbonization roadmap is where many organizations stall. Council Fire helps close that gap by screening facilities, fleets, and industrial processes to identify the most promising IRA-supported interventions, then building phased pipelines that fit an organization's capital budget and risk appetite.

That work includes stakeholder planning so projects deliver shared value, pairing IRA-supported solar and storage with resilience goals, and using credits as portfolio levers that shape timing, capital allocation, and project order.

Planning Framework and Next Steps

A Step-by-Step Screening and Modeling Process

Once credit types and monetization paths are set, the next move is portfolio screening. Begin with a full asset inventory. That means buildings, fleet vehicles, charging stations, renewable systems, batteries, and industrial equipment. For each asset, log the location, technology, capacity, placed-in-service timing, construction start date, procurement specs, and labor data. Then map each asset to a single credit and estimate both the base value and any bonus value.

After eligibility is mapped, turn each project into a net-cost model. The goal here is simple: show what the project will cost under the most likely monetization path, whether that is a retained credit, direct pay, or a transfer sale. Include timing, tax capacity, and transaction costs in the model. One clear example: a 1.1 MW rooftop solar project in New Jersey dropped from $1.87 million to $1.31 million after the 30% ITC [15].

This process is about more than claiming credits. It helps teams pick better projects. Once the modeling is done, rank projects based on emissions reduction, resilience value, credit value, implementation complexity, and payback period. That makes it easier to direct capital to the highest-value opportunities first.

Key Takeaways for Executives and Decision-Makers

For executives, the main job is turning eligibility into a ranked, financeable project pipeline. The difference between organizations that capture full credit value and those that leave money on the table often comes down to documentation and internal controls set up at the procurement stage, not at the end. Put those controls in place early, and assign clear owners across tax, finance, legal, sustainability, procurement, and project management. Compliance should be checked before payment milestones and before tax filing.

The groups in the strongest position are the ones treating IRA incentives as a long-term lever in capital planning and decarbonization strategy. A practical next step is to approve a cross-functional screening process, assign ownership for tax, finance, procurement, and sustainability inputs, and build a shortlist of eligible projects with early credit estimates.

FAQs

Which IRA credit fits my project best?

Match each project to the IRA credit that fits it best. For tax-exempt entities, Direct Pay can make clean energy projects far more workable because it lets them access the credit value even without tax liability.

For generation and energy system upgrades, the ITC applies to projects such as solar, wind, battery storage, and geothermal heat pumps. On the building side, efficiency work may fit 179D or residential energy credits, depending on the property type and the scope of the upgrade.

Production-led projects follow a different path. Clean hydrogen, carbon capture, and domestic manufacturing may qualify for 45V, 45Q, or 45X. In some cases, these credits also come with bonus adders in the 10% to 20% range, which can change the math in a big way.

Can my organization get cash instead of using tax credits?

Yes. Under the Inflation Reduction Act’s Direct Pay program, tax-exempt organizations, including nonprofits, can get cash reimbursements for clean energy projects that cover 30% to 70% of total project costs.

There’s an important timing step, though. To use the program, you must pre-register with the IRS at least 120 days before filing Forms 990-T and 3800.

For-profit companies have a different path. They can monetize these credits by transferring them to third parties.

What records do I need to protect the credit?

Maintain clear compliance records and steady performance tracking from start to finish.

If you’re using Direct Pay, pre-register with the IRS using Forms 990-T and 3800 at least 120 days before filing. You’ll also want records that verify:

domestic content

wage compliance

any supply chain compliance requirements

This isn’t busywork. Good documentation can save a lot of stress later, especially if questions come up during filing or review.

Related Blog Posts

Latest Articles

©2025

FAQ

01

What does it really mean to “redefine profit”?

02

What makes Council Fire different?

03

Who does Council Fire work with?

04

What does working with Council Fire actually look like?

05

How does Council Fire help organizations turn big goals into action?

06

How does Council Fire define and measure success?

Jul 18, 2026

Inflation Reduction Act: Tax Credit Opportunities

Sustainability Strategy

In This Article

Match IRA tax credits to projects, maximize bonuses, and monetize via direct pay or transfer across energy, buildings, fleets.

Inflation Reduction Act: Tax Credit Opportunities

The IRA can cut project cost by thousands - or millions - if I match the right tax credit to the right project and set up labor, sourcing, and filing rules early. For many organizations, the biggest levers are clean power credits, building deductions, fleet and charging credits, and select industry credits. Some credits can be used against taxes, some can be sold, and some can be paid out in cash to tax-exempt and public entities.

Here’s the short version:

Clean electricity: Solar, storage, and similar projects may qualify for ITC/PTC rules, now shifting to 45Y/48E for many projects placed in service from 2025 on.

Buildings:179D can provide $0.50 to $5.00 per square foot for energy-efficient commercial building work.

Vehicles:45W offers up to $7,500 for light-duty clean vehicles and up to $40,000 for heavy-duty vehicles.

Charging:30C can cover 30% of cost, up to $100,000 per unit, in eligible census tracts.

Industry: Credits like 45V for hydrogen can be worth up to $3.00 per kilogram, based on emissions rates.

Bonus rules matter: Meeting wage and apprenticeship rules can move a clean power credit from 6% to 30% or from $0.005/kWh to $0.025/kWh.

How I get the money matters: I may use the credit, sell it, or, if eligible, claim direct pay from the IRS.

A few points shape almost every IRA decision:

Timing matters. Many credits run through 2032, but rule changes started in 2025 for several clean electricity credits.

Project setup matters. Ownership, site choice, labor records, and domestic content can change credit value.

Paperwork matters. IRS registration, placed-in-service records, payroll support, and tax filings can decide whether a credit holds up.

Exchange Energy Tax Credits with the Inflation Reduction Act

Quick comparison

Area | Main credit(s) | What it does | Who should look first |

|---|---|---|---|

Clean power and storage | 48, 45, 48E, 45Y | Cuts upfront cost or pays by power output | Building owners, power project sponsors, public entities |

Commercial buildings | 179D | Deduction tied to energy savings | Building owners, architects, engineers on public/nonprofit work |

Fleet | 45W | Credit for business-use clean vehicles | Fleet managers, schools, local governments, companies |

Charging/refueling | 30C | Credit for charging equipment in eligible areas | Fleet operators, site hosts, property owners |

Industry | 45V, 45Q, 48C, 45Z | Supports hydrogen, carbon capture, fuels, manufacturing | Manufacturers and heavy industry |

If I am screening projects now, the first step is simple: map each project to one credit, test bonus eligibility, and decide early whether the value will come through tax use, transfer, or direct pay.

Key IRA Tax Credits for Clean Energy, Buildings, Transportation, and Industry

IRA Tax Credits for Clean Energy: Key Credits, Values & Bonus Opportunities

This section helps link each project type to the credit structure that fits it best. That matters early. The right credit can change whether a project moves now, comes in at a lower cost, or clears the return threshold more easily. Before you model project economics, map the project to the right credit first.

Project Type | IRC Section | Core Benefit | Bonus Opportunities | Eligible Claimants |

|---|---|---|---|---|

Clean Electricity (ITC) | 48 / 48E | 6% (30% with labor standards) | +10% Domestic Content; +10% Energy Community; +10–20% Low-Income | Corporations; Tax-Exempts via Direct Pay |

Clean Electricity (PTC) | 45 / 45Y | 0.5 cents per kWh (2.5 cents per kWh with labor standards) | +10% Domestic Content; +10% Energy Community | Corporations; Tax-Exempts via Direct Pay |

Efficient Commercial Buildings | 179D | $0.50–$5.00/sq ft | Higher value with labor standards | Building owners; designers for public/nonprofit buildings |

Commercial Clean Vehicles | 45W | Up to $7,500 (light-duty) / $40,000 (heavy-duty) | N/A | Businesses; Tax-Exempt entities |

EV Charging / Refueling | 30C | 30% of cost | Up to $100,000 per unit | Businesses in eligible census tracts |

Clean Hydrogen | 45V | Up to $3.00/kg | Based on lifecycle GHG emissions | Industrial producers |

Project structure shapes the payout. Some credits cut upfront cost. Others pay off over time based on output.

Clean Electricity Credits: ITC, PTC, and Technology-Neutral Credits

The Investment Tax Credit (ITC) gives an upfront credit based on eligible project costs. That often makes it a strong fit for solar, battery storage, and geothermal. The Production Tax Credit (PTC), by contrast, pays over 10 years based on actual kilowatt-hours generated, which tends to line up better with high-output assets such as wind.

On their own, the base rates are pretty small: 6% for the ITC and $0.005 per kWh for the PTC. If a project meets prevailing wage and apprenticeship rules, those rates jump to 30% and $0.025 per kWh - a fivefold increase [3]. In plain terms, capex-heavy projects often lean toward the ITC, while assets expected to produce a lot of electricity often lean toward the PTC.

Starting January 1, 2025, facilities placed in service after December 31, 2024, generally move to the technology-neutral Sections 48E and 45Y if they are zero greenhouse gas emissions facilities [3]. Projects placed in service before that date stay under legacy Sections 48 and 45. Bonus value can also stack through domestic content, energy community siting, and low-income community rules, adding +10%, +10%, and +10–20%, respectively [3].

That same screening mindset carries into buildings, fleets, and industrial assets, even though the credit mechanics shift.

Building, Vehicle, and Charging Infrastructure Credits

Section 179D applies to energy-efficient commercial buildings and gives a deduction of $0.50 to $5.00 per square foot, with more value available when labor standards are met. One detail people sometimes miss: designers working on government or nonprofit buildings, including architects and engineers, can claim the deduction directly even if they do not own the building.

These credits tend to land best when building upgrades and fleet changes are already part of the capital plan. In other words, they work well when tax planning and project planning are moving together.

For fleet managers, Section 45W provides up to $7,500 for light-duty clean vehicles and up to $40,000 for heavy-duty vehicles used for business use. Section 30C covers 30% of project cost, up to $100,000 per unit, for businesses in eligible census tracts. Paired together, Sections 45W and 30C can help support both fleet electrification and the charging buildout behind it.

Industrial and Manufacturing Credits

Hard-to-abate projects have their own credit stack, especially around hydrogen, capture, and clean fuels.

Section 45V for clean hydrogen offers up to $3.00 per kilogram. The actual credit amount depends on lifecycle greenhouse gas emissions, so lower-emissions production earns a higher credit.

Other industrial credits worth screening include advanced energy project credits under Section 48C, carbon capture incentives under Section 45Q, sustainable aviation fuel credits under Section 40B, and clean fuel production credits under Section 45Z. These tend to matter most for manufacturers and heavy industry. In that setting, the IRA is not just a subsidy. It becomes a design input for process change, fuel switching, and supply chain shifts.

How Organizations Can Monetize IRA Credits

Once a project lines up with an IRA credit, the next step is simple in theory and often tricky in practice: how do you turn that credit into dollars and cents? Most organizations have three paths. They can keep the credit and use it against their own tax bill, sell it for cash, or claim direct pay if they qualify. The best option depends on tax status, cash needs, and timing.

Feature | Retain and Use Internally | Transferability | Direct Pay |

|---|---|---|---|

Eligibility | Taxable entities with enough tax liability to use the credit | Eligible taxpayers with transferable credits | Applicable entities for most credits; certain other taxpayers for specified credits |

Cash Flow | Full credit value offsets tax liability | Cash from selling the credit | Cash payment from the IRS |

Counterparties | IRS | Unrelated buyer | IRS / Federal Government |

Key Risks | Insufficient tax liability | Eligibility, diligence, recapture, and indemnity issues | Registration and documentation errors |

Direct Pay for Tax-Exempt and Public Entities

Elective payment, often called direct pay, is the rule under IRC §6417 that allows eligible entities to receive a cash payment from the IRS equal to the value of certain credits, even if they have no federal income tax liability[5][8][11]. That said, it does not apply to every credit. Teams should confirm the exact credit section before treating a project like it can be settled in cash[10][11].

Eligible entities include tax-exempt organizations under Section 501(a), state and local governments, U.S. territories, Indian tribal governments, Alaska Native Corporations, rural electric cooperatives, the Tennessee Valley Authority, and agencies or instrumentalities of those governments[4][8][11]. That list is longer than many people expect, which is why early eligibility review matters.

The process usually begins with IRS pre-filing registration through Energy Credits Online (ECO). Each eligible project needs its own registration number, and that number must appear on the original tax return that makes the elective payment election. The IRS strongly recommends filing registration at least 120 days before the planned filing date[6][7][9][12]. In day-to-day work, the problems tend to be pretty predictable:

Missed registration timing

Mismatches between project records and tax filings

Wrong ownership or placed-in-service assumptions

Incomplete support for wage or apprenticeship rules where they apply

Transferability and Tax Credit Sales

For taxable entities that generate more credits than they can use, transferability under IRC §6418 allows certain eligible credits to be sold one time for cash to an unrelated buyer[10][13][14]. That can turn a future tax item into near-term liquidity, which is a big deal for sponsors trying to keep projects moving.

There is a firm limit here: credits can be transferred only once, and re-transfers are not allowed[13][14]. Partnerships may also qualify as eligible taxpayers for transfers, even if tax-exempt entities or other applicable entities own them in whole or in part[13].

Buyers usually want to see the full paper trail. That often includes project contracts, ownership and title records, placed-in-service support, wage and apprenticeship records when needed, basis calculations, energy-modeling or production assumptions when relevant, and legal opinions or tax diligence memos. On the seller side, it is common to see representations and warranties, escrow or reserve terms, and indemnity duties if the credit is later challenged[13][14].

Capital Planning for climate resilience and sustainability portfolios

Monetization should be built into project design from the start, not handled as a tax choice after the deal is done. The path you choose can shape debt sizing, debt service coverage ratios, grant stacking, covenant compliance, and project sequencing. A finance-and-tax model that compares after-tax returns, net present value, cash timing, deal costs, and risk allocation across all three paths is the right place to begin[10][13][14].

Ownership structure matters too. It determines who can claim the credit, who can elect direct pay if eligible, and whether the credit can be transferred. Some organizations also phase projects so that the simplest assets to qualify are placed in service first. That can bring in earlier cash flow or tax value, which may help fund later stages.

Create an IRA credit steering group early so ownership, procurement, and tax structuring are lined up before contracts are signed.

That choice should feed straight into the screening and modeling process that comes next.

Integrating IRA Credits into a Sustainability Roadmap

Once credits are modeled, the next move is portfolio design: which projects go first, and why.

IRA credits can help teams put the right projects at the front of the line - projects that cut emissions, improve resilience, and make the numbers work better. A practical place to start is a Scope 1 and 2 emissions baseline across facilities and fleets, then map Scope 3 hotspots to the projects most likely to address them.

Use the table to rank projects by emissions impact, resilience value, and readiness - not just by credit size.

Align Credits with Decarbonization and Resilience Priorities

Sustainability Initiative | Likely IRA Incentives | Key Planning Considerations |

|---|---|---|

Rooftop solar + storage | Section 48/48E, plus bonuses where applicable; direct pay for eligible entities | Confirm ownership structure and interconnection; meet prevailing wage and apprenticeship rules; integrate with resilience goals (backup power for critical loads) |

Commercial building retrofits (HVAC, envelope, electrification) | Section 179D commercial building deduction (up to $5.00/sq ft) [2][18][17] | Require pre- and post-project energy modeling to ASHRAE standards; align with science-based targets; track interactions with local building performance standards |

Fleet electrification (medium- and heavy-duty) | Use 45W and 30C together to time vehicle replacement, charging buildout, and utility upgrades | Build a fleet transition roadmap using telematics data; plan depot charging and grid capacity upgrades; coordinate with utility make-ready programs |

Hydrogen pilots | Reserve 45V for sites with a clear low-carbon hydrogen pathway and reliable emissions data | Determine production pathway and lifecycle emissions intensity; secure robust GHG accounting |

Resilient infrastructure (microgrids, backup power, critical loads) | Integrate climate risk modeling into site selection; structure projects to provide community benefits; assess long-term adaptive management |

Sequencing matters. Early waves - LED upgrades, rooftop solar, and basic controls - are often faster to permit, easier to document, and faster to turn into incentive value. That early value can help fund heavier lifts later, like industrial fuel switching or hydrogen pilots. When teams rank projects, resilience criteria should sit right beside cost of carbon abatement, including measures like critical load coverage during grid outages and storm hardening.

After projects are prioritized, the next job is protecting the credit value already on the table.

Governance, Compliance, and Reporting Controls

Getting bonus credit levels takes proof, not good intentions. A cross-functional IRA and Sustainability Steering Committee - with tax, finance, sustainability, legal, procurement, and internal audit at the table - is often the best way to keep the work moving in step. This group should set RACI roles for documentation, define investment criteria that weigh emissions cuts alongside NPV, and bring recapture, compliance, and delivery risk into enterprise risk management.

The paper trail matters more than many teams expect. Certified payroll records, apprenticeship program documentation, manufacturer certificates of origin, and component cost breakdowns should all live in one central system, with retention policies tied to IRS statute of limitations.

On the reporting side, harmonizing tax and sustainability data helps avoid a common mess: claiming emissions reductions in an ESG report that don't line up with the assumptions in a project's financial model. Standardized baselines, recognized GHG accounting frameworks like the GHG Protocol, and interval metering data help IRA-credited projects connect cleanly to Scope 1 and 2 inventories while supporting audit-ready disclosures for CDP, SBTi, or SEC climate reporting.

Execution then comes down to turning those controls into a pipeline that can actually be built and financed.

How Council Fire Can Support Implementation

Turning eligible credits into a working, multi-year decarbonization roadmap is where many organizations stall. Council Fire helps close that gap by screening facilities, fleets, and industrial processes to identify the most promising IRA-supported interventions, then building phased pipelines that fit an organization's capital budget and risk appetite.

That work includes stakeholder planning so projects deliver shared value, pairing IRA-supported solar and storage with resilience goals, and using credits as portfolio levers that shape timing, capital allocation, and project order.

Planning Framework and Next Steps

A Step-by-Step Screening and Modeling Process

Once credit types and monetization paths are set, the next move is portfolio screening. Begin with a full asset inventory. That means buildings, fleet vehicles, charging stations, renewable systems, batteries, and industrial equipment. For each asset, log the location, technology, capacity, placed-in-service timing, construction start date, procurement specs, and labor data. Then map each asset to a single credit and estimate both the base value and any bonus value.

After eligibility is mapped, turn each project into a net-cost model. The goal here is simple: show what the project will cost under the most likely monetization path, whether that is a retained credit, direct pay, or a transfer sale. Include timing, tax capacity, and transaction costs in the model. One clear example: a 1.1 MW rooftop solar project in New Jersey dropped from $1.87 million to $1.31 million after the 30% ITC [15].

This process is about more than claiming credits. It helps teams pick better projects. Once the modeling is done, rank projects based on emissions reduction, resilience value, credit value, implementation complexity, and payback period. That makes it easier to direct capital to the highest-value opportunities first.

Key Takeaways for Executives and Decision-Makers

For executives, the main job is turning eligibility into a ranked, financeable project pipeline. The difference between organizations that capture full credit value and those that leave money on the table often comes down to documentation and internal controls set up at the procurement stage, not at the end. Put those controls in place early, and assign clear owners across tax, finance, legal, sustainability, procurement, and project management. Compliance should be checked before payment milestones and before tax filing.

The groups in the strongest position are the ones treating IRA incentives as a long-term lever in capital planning and decarbonization strategy. A practical next step is to approve a cross-functional screening process, assign ownership for tax, finance, procurement, and sustainability inputs, and build a shortlist of eligible projects with early credit estimates.

FAQs

Which IRA credit fits my project best?

Match each project to the IRA credit that fits it best. For tax-exempt entities, Direct Pay can make clean energy projects far more workable because it lets them access the credit value even without tax liability.

For generation and energy system upgrades, the ITC applies to projects such as solar, wind, battery storage, and geothermal heat pumps. On the building side, efficiency work may fit 179D or residential energy credits, depending on the property type and the scope of the upgrade.

Production-led projects follow a different path. Clean hydrogen, carbon capture, and domestic manufacturing may qualify for 45V, 45Q, or 45X. In some cases, these credits also come with bonus adders in the 10% to 20% range, which can change the math in a big way.

Can my organization get cash instead of using tax credits?

Yes. Under the Inflation Reduction Act’s Direct Pay program, tax-exempt organizations, including nonprofits, can get cash reimbursements for clean energy projects that cover 30% to 70% of total project costs.

There’s an important timing step, though. To use the program, you must pre-register with the IRS at least 120 days before filing Forms 990-T and 3800.

For-profit companies have a different path. They can monetize these credits by transferring them to third parties.

What records do I need to protect the credit?

Maintain clear compliance records and steady performance tracking from start to finish.

If you’re using Direct Pay, pre-register with the IRS using Forms 990-T and 3800 at least 120 days before filing. You’ll also want records that verify:

domestic content

wage compliance

any supply chain compliance requirements

This isn’t busywork. Good documentation can save a lot of stress later, especially if questions come up during filing or review.

Related Blog Posts

FAQ

01

What does it really mean to “redefine profit”?

02

What makes Council Fire different?

03

Who does Council Fire work with?

04

What does working with Council Fire actually look like?

05

How does Council Fire help organizations turn big goals into action?

06

How does Council Fire define and measure success?

Jul 18, 2026

Inflation Reduction Act: Tax Credit Opportunities

Sustainability Strategy

In This Article

Match IRA tax credits to projects, maximize bonuses, and monetize via direct pay or transfer across energy, buildings, fleets.

Inflation Reduction Act: Tax Credit Opportunities

The IRA can cut project cost by thousands - or millions - if I match the right tax credit to the right project and set up labor, sourcing, and filing rules early. For many organizations, the biggest levers are clean power credits, building deductions, fleet and charging credits, and select industry credits. Some credits can be used against taxes, some can be sold, and some can be paid out in cash to tax-exempt and public entities.

Here’s the short version:

Clean electricity: Solar, storage, and similar projects may qualify for ITC/PTC rules, now shifting to 45Y/48E for many projects placed in service from 2025 on.

Buildings:179D can provide $0.50 to $5.00 per square foot for energy-efficient commercial building work.

Vehicles:45W offers up to $7,500 for light-duty clean vehicles and up to $40,000 for heavy-duty vehicles.

Charging:30C can cover 30% of cost, up to $100,000 per unit, in eligible census tracts.

Industry: Credits like 45V for hydrogen can be worth up to $3.00 per kilogram, based on emissions rates.

Bonus rules matter: Meeting wage and apprenticeship rules can move a clean power credit from 6% to 30% or from $0.005/kWh to $0.025/kWh.

How I get the money matters: I may use the credit, sell it, or, if eligible, claim direct pay from the IRS.

A few points shape almost every IRA decision:

Timing matters. Many credits run through 2032, but rule changes started in 2025 for several clean electricity credits.

Project setup matters. Ownership, site choice, labor records, and domestic content can change credit value.

Paperwork matters. IRS registration, placed-in-service records, payroll support, and tax filings can decide whether a credit holds up.

Exchange Energy Tax Credits with the Inflation Reduction Act

Quick comparison

Area | Main credit(s) | What it does | Who should look first |

|---|---|---|---|

Clean power and storage | 48, 45, 48E, 45Y | Cuts upfront cost or pays by power output | Building owners, power project sponsors, public entities |

Commercial buildings | 179D | Deduction tied to energy savings | Building owners, architects, engineers on public/nonprofit work |

Fleet | 45W | Credit for business-use clean vehicles | Fleet managers, schools, local governments, companies |

Charging/refueling | 30C | Credit for charging equipment in eligible areas | Fleet operators, site hosts, property owners |

Industry | 45V, 45Q, 48C, 45Z | Supports hydrogen, carbon capture, fuels, manufacturing | Manufacturers and heavy industry |

If I am screening projects now, the first step is simple: map each project to one credit, test bonus eligibility, and decide early whether the value will come through tax use, transfer, or direct pay.

Key IRA Tax Credits for Clean Energy, Buildings, Transportation, and Industry

IRA Tax Credits for Clean Energy: Key Credits, Values & Bonus Opportunities

This section helps link each project type to the credit structure that fits it best. That matters early. The right credit can change whether a project moves now, comes in at a lower cost, or clears the return threshold more easily. Before you model project economics, map the project to the right credit first.

Project Type | IRC Section | Core Benefit | Bonus Opportunities | Eligible Claimants |

|---|---|---|---|---|

Clean Electricity (ITC) | 48 / 48E | 6% (30% with labor standards) | +10% Domestic Content; +10% Energy Community; +10–20% Low-Income | Corporations; Tax-Exempts via Direct Pay |

Clean Electricity (PTC) | 45 / 45Y | 0.5 cents per kWh (2.5 cents per kWh with labor standards) | +10% Domestic Content; +10% Energy Community | Corporations; Tax-Exempts via Direct Pay |

Efficient Commercial Buildings | 179D | $0.50–$5.00/sq ft | Higher value with labor standards | Building owners; designers for public/nonprofit buildings |

Commercial Clean Vehicles | 45W | Up to $7,500 (light-duty) / $40,000 (heavy-duty) | N/A | Businesses; Tax-Exempt entities |

EV Charging / Refueling | 30C | 30% of cost | Up to $100,000 per unit | Businesses in eligible census tracts |

Clean Hydrogen | 45V | Up to $3.00/kg | Based on lifecycle GHG emissions | Industrial producers |

Project structure shapes the payout. Some credits cut upfront cost. Others pay off over time based on output.

Clean Electricity Credits: ITC, PTC, and Technology-Neutral Credits

The Investment Tax Credit (ITC) gives an upfront credit based on eligible project costs. That often makes it a strong fit for solar, battery storage, and geothermal. The Production Tax Credit (PTC), by contrast, pays over 10 years based on actual kilowatt-hours generated, which tends to line up better with high-output assets such as wind.

On their own, the base rates are pretty small: 6% for the ITC and $0.005 per kWh for the PTC. If a project meets prevailing wage and apprenticeship rules, those rates jump to 30% and $0.025 per kWh - a fivefold increase [3]. In plain terms, capex-heavy projects often lean toward the ITC, while assets expected to produce a lot of electricity often lean toward the PTC.

Starting January 1, 2025, facilities placed in service after December 31, 2024, generally move to the technology-neutral Sections 48E and 45Y if they are zero greenhouse gas emissions facilities [3]. Projects placed in service before that date stay under legacy Sections 48 and 45. Bonus value can also stack through domestic content, energy community siting, and low-income community rules, adding +10%, +10%, and +10–20%, respectively [3].

That same screening mindset carries into buildings, fleets, and industrial assets, even though the credit mechanics shift.

Building, Vehicle, and Charging Infrastructure Credits

Section 179D applies to energy-efficient commercial buildings and gives a deduction of $0.50 to $5.00 per square foot, with more value available when labor standards are met. One detail people sometimes miss: designers working on government or nonprofit buildings, including architects and engineers, can claim the deduction directly even if they do not own the building.

These credits tend to land best when building upgrades and fleet changes are already part of the capital plan. In other words, they work well when tax planning and project planning are moving together.

For fleet managers, Section 45W provides up to $7,500 for light-duty clean vehicles and up to $40,000 for heavy-duty vehicles used for business use. Section 30C covers 30% of project cost, up to $100,000 per unit, for businesses in eligible census tracts. Paired together, Sections 45W and 30C can help support both fleet electrification and the charging buildout behind it.

Industrial and Manufacturing Credits

Hard-to-abate projects have their own credit stack, especially around hydrogen, capture, and clean fuels.

Section 45V for clean hydrogen offers up to $3.00 per kilogram. The actual credit amount depends on lifecycle greenhouse gas emissions, so lower-emissions production earns a higher credit.

Other industrial credits worth screening include advanced energy project credits under Section 48C, carbon capture incentives under Section 45Q, sustainable aviation fuel credits under Section 40B, and clean fuel production credits under Section 45Z. These tend to matter most for manufacturers and heavy industry. In that setting, the IRA is not just a subsidy. It becomes a design input for process change, fuel switching, and supply chain shifts.

How Organizations Can Monetize IRA Credits

Once a project lines up with an IRA credit, the next step is simple in theory and often tricky in practice: how do you turn that credit into dollars and cents? Most organizations have three paths. They can keep the credit and use it against their own tax bill, sell it for cash, or claim direct pay if they qualify. The best option depends on tax status, cash needs, and timing.

Feature | Retain and Use Internally | Transferability | Direct Pay |

|---|---|---|---|

Eligibility | Taxable entities with enough tax liability to use the credit | Eligible taxpayers with transferable credits | Applicable entities for most credits; certain other taxpayers for specified credits |

Cash Flow | Full credit value offsets tax liability | Cash from selling the credit | Cash payment from the IRS |

Counterparties | IRS | Unrelated buyer | IRS / Federal Government |

Key Risks | Insufficient tax liability | Eligibility, diligence, recapture, and indemnity issues | Registration and documentation errors |

Direct Pay for Tax-Exempt and Public Entities

Elective payment, often called direct pay, is the rule under IRC §6417 that allows eligible entities to receive a cash payment from the IRS equal to the value of certain credits, even if they have no federal income tax liability[5][8][11]. That said, it does not apply to every credit. Teams should confirm the exact credit section before treating a project like it can be settled in cash[10][11].

Eligible entities include tax-exempt organizations under Section 501(a), state and local governments, U.S. territories, Indian tribal governments, Alaska Native Corporations, rural electric cooperatives, the Tennessee Valley Authority, and agencies or instrumentalities of those governments[4][8][11]. That list is longer than many people expect, which is why early eligibility review matters.

The process usually begins with IRS pre-filing registration through Energy Credits Online (ECO). Each eligible project needs its own registration number, and that number must appear on the original tax return that makes the elective payment election. The IRS strongly recommends filing registration at least 120 days before the planned filing date[6][7][9][12]. In day-to-day work, the problems tend to be pretty predictable:

Missed registration timing

Mismatches between project records and tax filings

Wrong ownership or placed-in-service assumptions

Incomplete support for wage or apprenticeship rules where they apply

Transferability and Tax Credit Sales

For taxable entities that generate more credits than they can use, transferability under IRC §6418 allows certain eligible credits to be sold one time for cash to an unrelated buyer[10][13][14]. That can turn a future tax item into near-term liquidity, which is a big deal for sponsors trying to keep projects moving.

There is a firm limit here: credits can be transferred only once, and re-transfers are not allowed[13][14]. Partnerships may also qualify as eligible taxpayers for transfers, even if tax-exempt entities or other applicable entities own them in whole or in part[13].

Buyers usually want to see the full paper trail. That often includes project contracts, ownership and title records, placed-in-service support, wage and apprenticeship records when needed, basis calculations, energy-modeling or production assumptions when relevant, and legal opinions or tax diligence memos. On the seller side, it is common to see representations and warranties, escrow or reserve terms, and indemnity duties if the credit is later challenged[13][14].

Capital Planning for climate resilience and sustainability portfolios

Monetization should be built into project design from the start, not handled as a tax choice after the deal is done. The path you choose can shape debt sizing, debt service coverage ratios, grant stacking, covenant compliance, and project sequencing. A finance-and-tax model that compares after-tax returns, net present value, cash timing, deal costs, and risk allocation across all three paths is the right place to begin[10][13][14].

Ownership structure matters too. It determines who can claim the credit, who can elect direct pay if eligible, and whether the credit can be transferred. Some organizations also phase projects so that the simplest assets to qualify are placed in service first. That can bring in earlier cash flow or tax value, which may help fund later stages.

Create an IRA credit steering group early so ownership, procurement, and tax structuring are lined up before contracts are signed.

That choice should feed straight into the screening and modeling process that comes next.

Integrating IRA Credits into a Sustainability Roadmap

Once credits are modeled, the next move is portfolio design: which projects go first, and why.

IRA credits can help teams put the right projects at the front of the line - projects that cut emissions, improve resilience, and make the numbers work better. A practical place to start is a Scope 1 and 2 emissions baseline across facilities and fleets, then map Scope 3 hotspots to the projects most likely to address them.

Use the table to rank projects by emissions impact, resilience value, and readiness - not just by credit size.

Align Credits with Decarbonization and Resilience Priorities

Sustainability Initiative | Likely IRA Incentives | Key Planning Considerations |

|---|---|---|

Rooftop solar + storage | Section 48/48E, plus bonuses where applicable; direct pay for eligible entities | Confirm ownership structure and interconnection; meet prevailing wage and apprenticeship rules; integrate with resilience goals (backup power for critical loads) |

Commercial building retrofits (HVAC, envelope, electrification) | Section 179D commercial building deduction (up to $5.00/sq ft) [2][18][17] | Require pre- and post-project energy modeling to ASHRAE standards; align with science-based targets; track interactions with local building performance standards |

Fleet electrification (medium- and heavy-duty) | Use 45W and 30C together to time vehicle replacement, charging buildout, and utility upgrades | Build a fleet transition roadmap using telematics data; plan depot charging and grid capacity upgrades; coordinate with utility make-ready programs |

Hydrogen pilots | Reserve 45V for sites with a clear low-carbon hydrogen pathway and reliable emissions data | Determine production pathway and lifecycle emissions intensity; secure robust GHG accounting |

Resilient infrastructure (microgrids, backup power, critical loads) | Integrate climate risk modeling into site selection; structure projects to provide community benefits; assess long-term adaptive management |

Sequencing matters. Early waves - LED upgrades, rooftop solar, and basic controls - are often faster to permit, easier to document, and faster to turn into incentive value. That early value can help fund heavier lifts later, like industrial fuel switching or hydrogen pilots. When teams rank projects, resilience criteria should sit right beside cost of carbon abatement, including measures like critical load coverage during grid outages and storm hardening.

After projects are prioritized, the next job is protecting the credit value already on the table.

Governance, Compliance, and Reporting Controls

Getting bonus credit levels takes proof, not good intentions. A cross-functional IRA and Sustainability Steering Committee - with tax, finance, sustainability, legal, procurement, and internal audit at the table - is often the best way to keep the work moving in step. This group should set RACI roles for documentation, define investment criteria that weigh emissions cuts alongside NPV, and bring recapture, compliance, and delivery risk into enterprise risk management.

The paper trail matters more than many teams expect. Certified payroll records, apprenticeship program documentation, manufacturer certificates of origin, and component cost breakdowns should all live in one central system, with retention policies tied to IRS statute of limitations.

On the reporting side, harmonizing tax and sustainability data helps avoid a common mess: claiming emissions reductions in an ESG report that don't line up with the assumptions in a project's financial model. Standardized baselines, recognized GHG accounting frameworks like the GHG Protocol, and interval metering data help IRA-credited projects connect cleanly to Scope 1 and 2 inventories while supporting audit-ready disclosures for CDP, SBTi, or SEC climate reporting.

Execution then comes down to turning those controls into a pipeline that can actually be built and financed.

How Council Fire Can Support Implementation

Turning eligible credits into a working, multi-year decarbonization roadmap is where many organizations stall. Council Fire helps close that gap by screening facilities, fleets, and industrial processes to identify the most promising IRA-supported interventions, then building phased pipelines that fit an organization's capital budget and risk appetite.

That work includes stakeholder planning so projects deliver shared value, pairing IRA-supported solar and storage with resilience goals, and using credits as portfolio levers that shape timing, capital allocation, and project order.

Planning Framework and Next Steps

A Step-by-Step Screening and Modeling Process

Once credit types and monetization paths are set, the next move is portfolio screening. Begin with a full asset inventory. That means buildings, fleet vehicles, charging stations, renewable systems, batteries, and industrial equipment. For each asset, log the location, technology, capacity, placed-in-service timing, construction start date, procurement specs, and labor data. Then map each asset to a single credit and estimate both the base value and any bonus value.

After eligibility is mapped, turn each project into a net-cost model. The goal here is simple: show what the project will cost under the most likely monetization path, whether that is a retained credit, direct pay, or a transfer sale. Include timing, tax capacity, and transaction costs in the model. One clear example: a 1.1 MW rooftop solar project in New Jersey dropped from $1.87 million to $1.31 million after the 30% ITC [15].

This process is about more than claiming credits. It helps teams pick better projects. Once the modeling is done, rank projects based on emissions reduction, resilience value, credit value, implementation complexity, and payback period. That makes it easier to direct capital to the highest-value opportunities first.

Key Takeaways for Executives and Decision-Makers

For executives, the main job is turning eligibility into a ranked, financeable project pipeline. The difference between organizations that capture full credit value and those that leave money on the table often comes down to documentation and internal controls set up at the procurement stage, not at the end. Put those controls in place early, and assign clear owners across tax, finance, legal, sustainability, procurement, and project management. Compliance should be checked before payment milestones and before tax filing.

The groups in the strongest position are the ones treating IRA incentives as a long-term lever in capital planning and decarbonization strategy. A practical next step is to approve a cross-functional screening process, assign ownership for tax, finance, procurement, and sustainability inputs, and build a shortlist of eligible projects with early credit estimates.

FAQs

Which IRA credit fits my project best?

Match each project to the IRA credit that fits it best. For tax-exempt entities, Direct Pay can make clean energy projects far more workable because it lets them access the credit value even without tax liability.

For generation and energy system upgrades, the ITC applies to projects such as solar, wind, battery storage, and geothermal heat pumps. On the building side, efficiency work may fit 179D or residential energy credits, depending on the property type and the scope of the upgrade.

Production-led projects follow a different path. Clean hydrogen, carbon capture, and domestic manufacturing may qualify for 45V, 45Q, or 45X. In some cases, these credits also come with bonus adders in the 10% to 20% range, which can change the math in a big way.

Can my organization get cash instead of using tax credits?

Yes. Under the Inflation Reduction Act’s Direct Pay program, tax-exempt organizations, including nonprofits, can get cash reimbursements for clean energy projects that cover 30% to 70% of total project costs.

There’s an important timing step, though. To use the program, you must pre-register with the IRS at least 120 days before filing Forms 990-T and 3800.

For-profit companies have a different path. They can monetize these credits by transferring them to third parties.

What records do I need to protect the credit?

Maintain clear compliance records and steady performance tracking from start to finish.

If you’re using Direct Pay, pre-register with the IRS using Forms 990-T and 3800 at least 120 days before filing. You’ll also want records that verify:

domestic content

wage compliance

any supply chain compliance requirements

This isn’t busywork. Good documentation can save a lot of stress later, especially if questions come up during filing or review.

Related Blog Posts

FAQ

What does it really mean to “redefine profit”?

What makes Council Fire different?

Who does Council Fire work with?

What does working with Council Fire actually look like?

How does Council Fire help organizations turn big goals into action?

How does Council Fire define and measure success?