Jul 7, 2026

Hydrogen in Steelmaking: Opportunities and Barriers

Sustainability Strategy

In This Article

Hydrogen can cut U.S. steel emissions to near zero, but high H₂ costs, massive power needs, ore limits, and policy risk block scale-up.

Hydrogen in Steelmaking: Opportunities and Barriers

Hydrogen can cut steel emissions to near zero, but in the U.S. the main block is cost. From what I see in this article, hydrogen-based steelmaking has a clear upside on emissions, yet it still runs into four hard limits at once: high hydrogen prices, huge power demand, heavy upfront spending, and policy swings.

If I boil it down, the article says:

Steel matters for emissions:U.S. steel made up about 87 million metric tons of output in 2023, and the sector accounts for about 2% of U.S. greenhouse gas emissions.

Hydrogen changes the core step: In hydrogen DRI, H₂ removes oxygen from iron ore and makes water vapor instead of CO₂.

The cost gap is still large: Green hydrogen needs to fall to about $1.63 to $1.70 per kilogram to compete, but today it is about $3 to $6 per kilogram.

Power needs are huge: A plant making 1 million tons per year may need about 500 MW of constant power, which can mean roughly 1 to 2 GW of wind and solar capacity.

Capital timing matters: A blast furnace reline can cost about $350 million, but a move to DRI-EAF with hydrogen needs much more site-wide spending.

Raw materials matter too: Hydrogen DRI needs high-quality DR-grade pellets, and much of the U.S. ore base needs more processing first.

Policy can speed up or slow down projects: Federal funding cuts and tighter tax credit deadlines have made planning harder.

The near-term path is mixed: Many mills may start with natural gas DRI-EAF or hydrogen blending first, then shift later if fuel, power, and policy line up.

My short take: hydrogen steelmaking is not blocked by chemistry. It is blocked by project economics and system buildout. For U.S. steelmakers, the biggest decision point is often not whether hydrogen can work, but when it makes sense to commit before the next major furnace reline.

Decarbonization 102-Hydrogen Ironmaking-Managing Expectations of H2 Transformation & Its Many Colors

Quick Comparison

Route | Emissions | Main Input | Cost Risk | Market Status |

|---|---|---|---|---|

BF-BOF | Highest | Coal/coke | Lower if asset already exists | Full-scale use |

NG-DRI-EAF | Lower | Natural gas | Mid-range | Full-scale use |

H2-DRI-EAF | Lowest | Green hydrogen | Highest | Early-stage rollout |

In short: the article points to hydrogen as the lowest-emissions route, but not yet the easiest one to build at scale in the United States.

The Core Problem: Why Hydrogen Steelmaking Is Hard to Scale

Hydrogen vs. Traditional Steelmaking: Emissions, Cost & Maturity Compared

Hydrogen steelmaking is hard to scale in the U.S. because several barriers land at the same time: fuel cost, power demand, capital spend, and policy risk. The chemistry works. The hard part is building the full system around it at industrial scale. A few early project wins don't change that bigger reality.

Cost, Power, and Capital Constraints

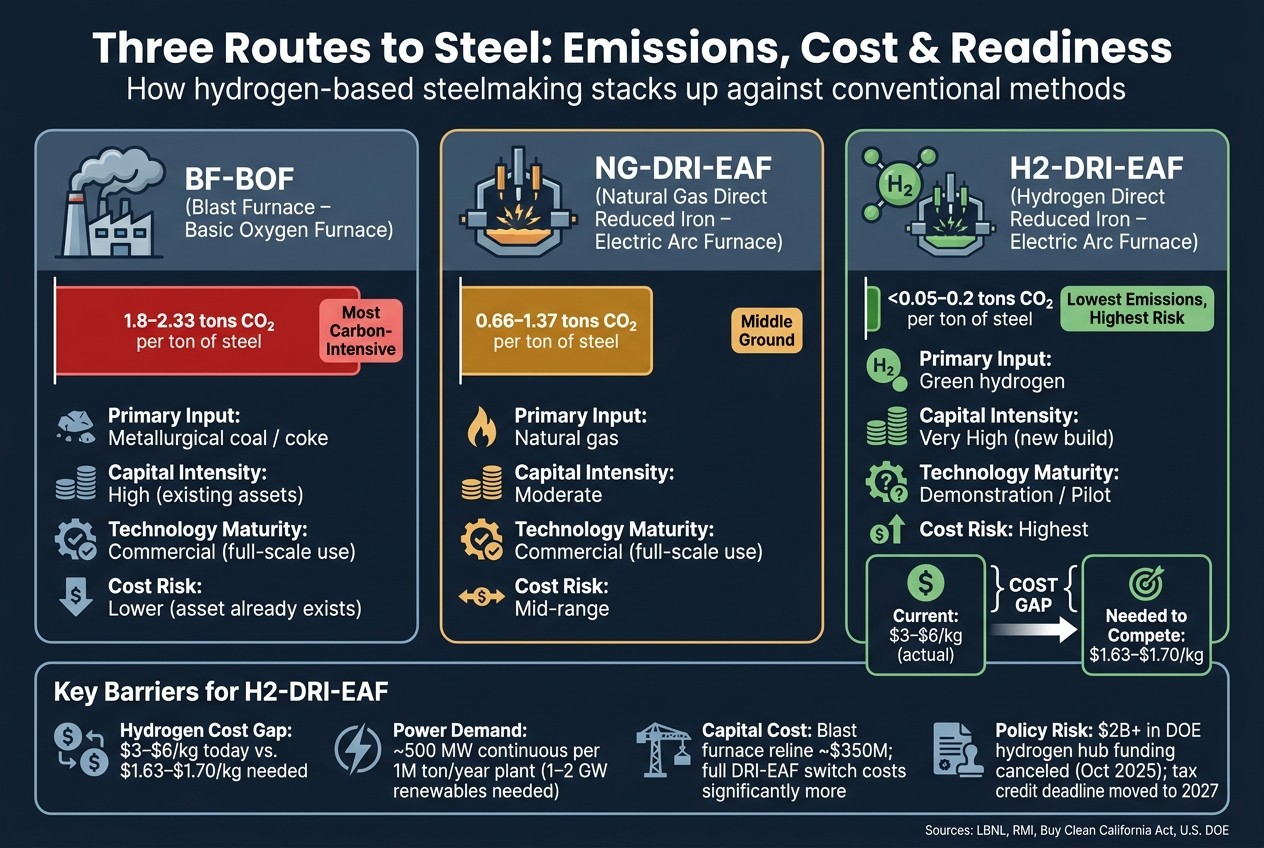

The biggest hurdle is still the price of green hydrogen. For H2-DRI to compete with today's natural-gas DRI, hydrogen procurement costs need to drop to about $1.63 to $1.70 per kilogram[6]. At the moment, green hydrogen sits around $3 to $6 per kilogram[3]. That's a big gap, and steelmakers feel every dollar of it.

Power needs make the math even tougher. A single steel plant producing 1 million tons per year needs about 500 MW of continuous electricity. Since wind and solar don't run at full output all day, that usually means roughly 1 to 2 GW of renewable capacity[6]. LBNL notes that one integrated steel mill can demand gigawatts of renewable generation and electrolysis capacity[6]. In plain terms, one mill can soak up a huge share of a region's clean power build-out.

Then there's the capital bill. Relining one large blast furnace costs about $350 million[4]. Moving to a full DRI-EAF route costs far more, with new spending needed for electrolyzers, shaft furnaces, hydrogen storage, and plant changes across the site. U.S. Steel, for instance, said it would reline the Gary Works No. 14 blast furnace in Indiana, a $350 million project that keeps the coal-based asset running for another 20 years[4]. That kind of choice shows the bind steelmakers are in: pay a large sum to extend what already exists, or spend much more to switch to a new route with less operating history.

Policy risk makes lenders and executives even more cautious. In October 2025, the U.S. Department of Energy canceled more than $2 billion in funding for West Coast hydrogen hubs[4]. The "One Big Beautiful Bill Act" also moved the construction start deadline for clean hydrogen tax credits from 2032 to 2027, and about 75% of projects in the pipeline are not expected to hit that date[5]. As RMI noted:

"Capital decisions made before 2030 will lock in US steelmaking pathways for decades, as blast furnaces approach costly reline deadlines." - RMI [4]

Supply Chain and Operational Limits

Even if the money showed up tomorrow, the supply chain would still be tight. H2-DRI works best with DR-grade iron ore pellets that are low in silica and highly porous. Much of the U.S. iron ore base is taconite, or magnetite, which is less porous, reduces more slowly, and needs extra processing before it fits a hydrogen shaft furnace[3][6]. So this isn't just a fuel switch. For many U.S. mills, it's also a raw-material and plant-design problem.

Electrolyzers are another choke point. A 2-million-ton-per-year iron plant would need about 1 GW of electrolyzer capacity[3]. Storage adds another layer of cost. Compressed hydrogen storage is expensive and energy intensive, while liquid carriers like methanol are still being studied[6].

There is also a process issue inside the mill. H2-DRI makes sponge iron without carbon, unlike natural gas DRI, which keeps some carbon in the product. That means mills have to add carbon later in the EAF to meet certain grade needs[6]. It's one more step, and one more design choice that has to work cleanly at scale.

Steelmaking Routes Compared

The table below puts the three main steelmaking routes next to each other. H2-DRI has the lowest emissions by far, but it also comes with the biggest capital burden and the least operating track record.

Route | CO₂ Emissions (tons/ton of steel) | Primary Fuel/Reductant | Capital Intensity | Technology Maturity |

|---|---|---|---|---|

BF-BOF | 1.8–2.33 [7] | Metallurgical coal/coke | High (existing assets) | Commercial |

NG-DRI-EAF | 0.66–1.37 [7] | Natural gas | Moderate | Commercial |

H2-DRI-EAF | <0.05–0.2 [7] | Green hydrogen | Very high (new build) | Demonstration/Pilot |

The pattern is pretty stark. BF-BOF is proven but carbon-heavy. NG-DRI-EAF cuts emissions and already runs at scale. H2-DRI-EAF offers the deepest emissions drop, yet it asks companies to take on the most risk upfront with the fewest full-scale examples to lean on. That helps explain why pilot projects are moving ahead faster than full commercial conversion.

Opportunities: Where Hydrogen Creates Value for Steel Producers

Emissions Reduction and Market Competitiveness

The clearest source of value in hydrogen steelmaking is lower emissions. That edge starts to matter a lot more when buyers and policymakers put a price on carbon. Natural gas DRI already cuts emissions by about 35% to 40% compared with blast furnace steel, which makes it a practical step between today's system and hydrogen-based production. [2][3]

Policy is already starting to shape demand. The Buy Clean California Act sets carbon-intensity limits for steel used in state construction projects. For hot-rolled steel, the limit is below 1.38 metric tons of CO₂ per metric ton. [3] Similar green procurement rules are spreading across the U.S., Japan, South Korea, and South Africa. [3] At that point, this is no longer just about public image. It becomes a question of who can still sell into key markets.

For steelmakers that still rely on blast furnaces, the pressure is building from both carbon pricing and tighter rules. As SSAB's Chief Technology Officer Martin Pei put it:

"We believe that in the long run, this will become even more competitive, since we know that emission costs will go up. Society is really pushing in that direction, and we believe there is a good business case." [3]

What Early Projects Show

Early projects are now testing whether this value holds up once companies face plant economics, fuel costs, and policy swings. HYBRIT stands out as the clearest proof point. It shows that hydrogen DRI is technically feasible and has already moved beyond the pilot stage into early commercial planning. [3]

That said, the picture in the U.S. is uneven. Hyundai moved ahead with a green steel mill in Louisiana, while Cleveland-Cliffs canceled a hydrogen project in Ohio after federal policy uncertainty. [5] That split tells its own story: the technology may be moving forward, but investment still depends on whether companies trust the rules of the game.

RMI's Kaitlyn Ramirez, Manager of Iron and Steel, put the logic plainly:

"When you first make the investment, it enables a pathway to leverage hydrogen as we build up the infrastructure, as the costs decline, and as the technology is de-risked to shift from gas-based production to hydrogen." [4]

Benefits vs. Risks of Hydrogen-Based Steel

Hydrogen-based steel brings two big upsides: deep emissions cuts and less reliance on imported coal and coke, which helps with energy security. But the costs are hard to ignore. Early production can carry a 20% to 30% cost premium over conventional steel. [3]

The setup is a bit of a mixed bag:

DRI shaft furnace technology is already proven, and hydrogen-ready plant designs are available. [2][3]

Hydrogen-only operations are still in the demonstration stage. [2][3]

U.S. federal funding and tax credit timelines remain volatile, which makes planning harder for long-lived industrial assets. [5]

That is why the biggest near-term opening may come at blast furnace reline deadlines. When a producer has to make a major capital decision anyway, building around DRI-EAF can keep the door open for hydrogen later, even if the plant starts on natural gas. [4]

Those tradeoffs lead straight to the next issue: what has to change for hydrogen steelmaking to scale?

Solutions: How to Address the Main Barriers to Hydrogen Steelmaking

Technology, Infrastructure, and Policy Actions

These barriers call for three things at the same time: lower-cost hydrogen, more clean power, and less project risk. No single group can push hydrogen steelmaking ahead on its own. Steel producers, energy suppliers, equipment makers, investors, and public agencies all have to line up their moves with care.

On the technology side, the most practical near-term step is to blend hydrogen into existing natural gas DRI plants before jumping to 100% hydrogen systems. That gives producers a lower-risk way to learn by doing. Thermal efficiency matters here as well. In hot charging setups, sponge iron moves straight into the EAF at about 1,300°F (700°C), which cuts energy losses in a meaningful way. Using EAF off-gas to preheat hydrogen can lift the break-even hydrogen price by up to $0.07/kg, which helps project economics. [2]

Grid upgrades and regional hydrogen hubs also need to move in step with plant investment. If one side gets ahead of the other, projects can stall. Methanol-based LOHCs may also cost less than compressed-gas storage for on-site storage and heat integration. [2]

Policy needs to do three jobs: build demand, cut first-of-a-kind (FOAK) project risk, and protect low-carbon steel from higher-emission imports. A Carbon Border Adjustment Mechanism (CBAM) would help shield domestic low-carbon producers from cheaper, higher-emission competition. Green procurement rules can also support the first wave of demand. One example is the Buy Clean California Act, which sets a limit of 1.38 metric tons of CO₂ per metric ton of hot-rolled steel. [3] Public-private risk-sharing for FOAK facilities matters just as much, since private investors alone are unlikely to take on the full cost of proving new plant designs at commercial scale.

Planning Steps for U.S. Decision-Makers

For mills facing big reinvestment calls, the next step is not commitment. It is comparison. Many U.S. steel facilities will hit reinvestment deadlines by 2030, so scenario analysis should test hydrogen prices, carbon costs, and policy timing before any capital is locked in.

For producers, scenario analysis is the right place to start. Investors should also watch feedstock quality closely. Hydrogen DRI processes need iron ore pellets with at least 67% iron content, and projects built around lower-grade ore face plain cost and performance risks. [1] Public agencies, meanwhile, need to put grid upgrades first in the Great Lakes and Southern regions, where steel production is clustered and where hydrogen hub development makes the most regional sense. [1]

Barrier-to-Solution Mapping

The main obstacles tie back to a short list of actions.

Barrier | Solution Type | Responsible Actors | Likely Timeline |

|---|---|---|---|

Hydrogen cost | Electrolyzer efficiency gains; hydrogen hubs | Electrolyzer makers, DOE, energy suppliers | 2026–2030 |

Clean power supply gaps | Grid upgrades; GW-scale renewables buildout | Utilities, energy suppliers, regulators | 2025–2035 |

High capital risk (FOAK) | Public-private risk-sharing; subsidies | Government, investors, steel producers | 2025–2030 |

Market competitiveness | CBAM; green public procurement | Policymakers, public agencies | 2024–2027 |

Feedstock quality (ore grade) | More DR-grade pellet supply and ore beneficiation | Mining companies, steel producers | 2025–2030 |

Conclusion: Hydrogen's Role in the Future of U.S. Steel

Hydrogen can help decarbonize U.S. steel, but scaling it is still the hard part. H2-DRI remains the lowest-carbon route now on the table, yet high costs, power demand, and iron ore feedstock limits still slow adoption at full industrial scale. [2]

Timing is just as important as the tech itself. That pressure shows up most clearly when mills face major reline decisions, because capital choices made before 2030 will shape steelmaking paths for decades. [4] For producers and policymakers, the job now is simple in theory and tough in practice: line up power, ore, and sustainable business capital plans before those decision windows shut. With federal hydrogen support looking less certain after the cancellation of over $2 billion in DOE hydrogen hub funding in October 2025 [4], state-level action is now doing more of the heavy lifting.

The path forward is clear: align power, ore, and capital plans before the next reline cycle.

FAQs

Why is green hydrogen still too expensive for steelmaking?

Green hydrogen is still too expensive for steelmaking. For most producers, the math just doesn’t work yet.

To compete with established natural gas-based processes, green hydrogen usually needs to land below $1.70–$2.00 per kilogram. Today, it often sits closer to $4–$8 per kilogram. That gap is the main problem.

A big reason comes down to electricity. Power accounts for 60–70% of green hydrogen production costs, which means high electricity prices can quickly wreck project economics. Limited access to low-cost renewable energy makes that challenge even tougher.

There’s also a policy issue. Without strong enough carbon pricing or government incentives, H2-DRI has a hard time competing with coal-based steelmaking. Put simply, cleaner production is available, but in many cases the market still rewards the cheaper, older route.

Can U.S. power grids support hydrogen-based steel plants?

It comes down to both technical limits and cost. Hydrogen-based steelmaking needs a large, steady flow of electricity to run electrolyzers. In many cases, tying a plant into the existing grid isn’t simple. Interconnection can take years, and the price tag can be high.

That’s why many experts look to off-grid hydrogen production powered by renewables. Putting hydrogen production next to wind or solar projects can ease grid and transmission bottlenecks. On top of that, hydrogen storage can help smooth out the ups and downs of renewable power, giving steel mills a more stable energy supply even though their demand stays constant.

Is natural gas DRI the most practical bridge to hydrogen steel?

Yes. Natural gas direct reduced iron (DRI) is widely seen as a practical bridge to hydrogen-based steelmaking.

Existing DRI shaft furnaces already run on hydrogen and carbon monoxide made from natural gas. That means steel producers don't have to rip everything out and start from scratch. In many cases, they can retrofit these systems to use a higher share of hydrogen over time.

That step-by-step path matters. It gives producers room to shift as green hydrogen supply expands and costs come down, without taking on a full facility overhaul all at once.

Related Blog Posts

Latest Articles

©2025

FAQ

01

What does it really mean to “redefine profit”?

02

What makes Council Fire different?

03

Who does Council Fire you work with?

04

What does working with Council Fire actually look like?

05

How does Council Fire help organizations turn big goals into action?

06

How does Council Fire define and measure success?

Jul 7, 2026

Hydrogen in Steelmaking: Opportunities and Barriers

Sustainability Strategy

In This Article

Hydrogen can cut U.S. steel emissions to near zero, but high H₂ costs, massive power needs, ore limits, and policy risk block scale-up.

Hydrogen in Steelmaking: Opportunities and Barriers

Hydrogen can cut steel emissions to near zero, but in the U.S. the main block is cost. From what I see in this article, hydrogen-based steelmaking has a clear upside on emissions, yet it still runs into four hard limits at once: high hydrogen prices, huge power demand, heavy upfront spending, and policy swings.

If I boil it down, the article says:

Steel matters for emissions:U.S. steel made up about 87 million metric tons of output in 2023, and the sector accounts for about 2% of U.S. greenhouse gas emissions.

Hydrogen changes the core step: In hydrogen DRI, H₂ removes oxygen from iron ore and makes water vapor instead of CO₂.

The cost gap is still large: Green hydrogen needs to fall to about $1.63 to $1.70 per kilogram to compete, but today it is about $3 to $6 per kilogram.

Power needs are huge: A plant making 1 million tons per year may need about 500 MW of constant power, which can mean roughly 1 to 2 GW of wind and solar capacity.

Capital timing matters: A blast furnace reline can cost about $350 million, but a move to DRI-EAF with hydrogen needs much more site-wide spending.

Raw materials matter too: Hydrogen DRI needs high-quality DR-grade pellets, and much of the U.S. ore base needs more processing first.

Policy can speed up or slow down projects: Federal funding cuts and tighter tax credit deadlines have made planning harder.

The near-term path is mixed: Many mills may start with natural gas DRI-EAF or hydrogen blending first, then shift later if fuel, power, and policy line up.

My short take: hydrogen steelmaking is not blocked by chemistry. It is blocked by project economics and system buildout. For U.S. steelmakers, the biggest decision point is often not whether hydrogen can work, but when it makes sense to commit before the next major furnace reline.

Decarbonization 102-Hydrogen Ironmaking-Managing Expectations of H2 Transformation & Its Many Colors

Quick Comparison

Route | Emissions | Main Input | Cost Risk | Market Status |

|---|---|---|---|---|

BF-BOF | Highest | Coal/coke | Lower if asset already exists | Full-scale use |

NG-DRI-EAF | Lower | Natural gas | Mid-range | Full-scale use |

H2-DRI-EAF | Lowest | Green hydrogen | Highest | Early-stage rollout |

In short: the article points to hydrogen as the lowest-emissions route, but not yet the easiest one to build at scale in the United States.

The Core Problem: Why Hydrogen Steelmaking Is Hard to Scale

Hydrogen vs. Traditional Steelmaking: Emissions, Cost & Maturity Compared

Hydrogen steelmaking is hard to scale in the U.S. because several barriers land at the same time: fuel cost, power demand, capital spend, and policy risk. The chemistry works. The hard part is building the full system around it at industrial scale. A few early project wins don't change that bigger reality.

Cost, Power, and Capital Constraints

The biggest hurdle is still the price of green hydrogen. For H2-DRI to compete with today's natural-gas DRI, hydrogen procurement costs need to drop to about $1.63 to $1.70 per kilogram[6]. At the moment, green hydrogen sits around $3 to $6 per kilogram[3]. That's a big gap, and steelmakers feel every dollar of it.

Power needs make the math even tougher. A single steel plant producing 1 million tons per year needs about 500 MW of continuous electricity. Since wind and solar don't run at full output all day, that usually means roughly 1 to 2 GW of renewable capacity[6]. LBNL notes that one integrated steel mill can demand gigawatts of renewable generation and electrolysis capacity[6]. In plain terms, one mill can soak up a huge share of a region's clean power build-out.

Then there's the capital bill. Relining one large blast furnace costs about $350 million[4]. Moving to a full DRI-EAF route costs far more, with new spending needed for electrolyzers, shaft furnaces, hydrogen storage, and plant changes across the site. U.S. Steel, for instance, said it would reline the Gary Works No. 14 blast furnace in Indiana, a $350 million project that keeps the coal-based asset running for another 20 years[4]. That kind of choice shows the bind steelmakers are in: pay a large sum to extend what already exists, or spend much more to switch to a new route with less operating history.

Policy risk makes lenders and executives even more cautious. In October 2025, the U.S. Department of Energy canceled more than $2 billion in funding for West Coast hydrogen hubs[4]. The "One Big Beautiful Bill Act" also moved the construction start deadline for clean hydrogen tax credits from 2032 to 2027, and about 75% of projects in the pipeline are not expected to hit that date[5]. As RMI noted:

"Capital decisions made before 2030 will lock in US steelmaking pathways for decades, as blast furnaces approach costly reline deadlines." - RMI [4]

Supply Chain and Operational Limits

Even if the money showed up tomorrow, the supply chain would still be tight. H2-DRI works best with DR-grade iron ore pellets that are low in silica and highly porous. Much of the U.S. iron ore base is taconite, or magnetite, which is less porous, reduces more slowly, and needs extra processing before it fits a hydrogen shaft furnace[3][6]. So this isn't just a fuel switch. For many U.S. mills, it's also a raw-material and plant-design problem.

Electrolyzers are another choke point. A 2-million-ton-per-year iron plant would need about 1 GW of electrolyzer capacity[3]. Storage adds another layer of cost. Compressed hydrogen storage is expensive and energy intensive, while liquid carriers like methanol are still being studied[6].

There is also a process issue inside the mill. H2-DRI makes sponge iron without carbon, unlike natural gas DRI, which keeps some carbon in the product. That means mills have to add carbon later in the EAF to meet certain grade needs[6]. It's one more step, and one more design choice that has to work cleanly at scale.

Steelmaking Routes Compared

The table below puts the three main steelmaking routes next to each other. H2-DRI has the lowest emissions by far, but it also comes with the biggest capital burden and the least operating track record.

Route | CO₂ Emissions (tons/ton of steel) | Primary Fuel/Reductant | Capital Intensity | Technology Maturity |

|---|---|---|---|---|

BF-BOF | 1.8–2.33 [7] | Metallurgical coal/coke | High (existing assets) | Commercial |

NG-DRI-EAF | 0.66–1.37 [7] | Natural gas | Moderate | Commercial |

H2-DRI-EAF | <0.05–0.2 [7] | Green hydrogen | Very high (new build) | Demonstration/Pilot |

The pattern is pretty stark. BF-BOF is proven but carbon-heavy. NG-DRI-EAF cuts emissions and already runs at scale. H2-DRI-EAF offers the deepest emissions drop, yet it asks companies to take on the most risk upfront with the fewest full-scale examples to lean on. That helps explain why pilot projects are moving ahead faster than full commercial conversion.

Opportunities: Where Hydrogen Creates Value for Steel Producers

Emissions Reduction and Market Competitiveness

The clearest source of value in hydrogen steelmaking is lower emissions. That edge starts to matter a lot more when buyers and policymakers put a price on carbon. Natural gas DRI already cuts emissions by about 35% to 40% compared with blast furnace steel, which makes it a practical step between today's system and hydrogen-based production. [2][3]

Policy is already starting to shape demand. The Buy Clean California Act sets carbon-intensity limits for steel used in state construction projects. For hot-rolled steel, the limit is below 1.38 metric tons of CO₂ per metric ton. [3] Similar green procurement rules are spreading across the U.S., Japan, South Korea, and South Africa. [3] At that point, this is no longer just about public image. It becomes a question of who can still sell into key markets.

For steelmakers that still rely on blast furnaces, the pressure is building from both carbon pricing and tighter rules. As SSAB's Chief Technology Officer Martin Pei put it:

"We believe that in the long run, this will become even more competitive, since we know that emission costs will go up. Society is really pushing in that direction, and we believe there is a good business case." [3]

What Early Projects Show

Early projects are now testing whether this value holds up once companies face plant economics, fuel costs, and policy swings. HYBRIT stands out as the clearest proof point. It shows that hydrogen DRI is technically feasible and has already moved beyond the pilot stage into early commercial planning. [3]

That said, the picture in the U.S. is uneven. Hyundai moved ahead with a green steel mill in Louisiana, while Cleveland-Cliffs canceled a hydrogen project in Ohio after federal policy uncertainty. [5] That split tells its own story: the technology may be moving forward, but investment still depends on whether companies trust the rules of the game.

RMI's Kaitlyn Ramirez, Manager of Iron and Steel, put the logic plainly:

"When you first make the investment, it enables a pathway to leverage hydrogen as we build up the infrastructure, as the costs decline, and as the technology is de-risked to shift from gas-based production to hydrogen." [4]

Benefits vs. Risks of Hydrogen-Based Steel

Hydrogen-based steel brings two big upsides: deep emissions cuts and less reliance on imported coal and coke, which helps with energy security. But the costs are hard to ignore. Early production can carry a 20% to 30% cost premium over conventional steel. [3]

The setup is a bit of a mixed bag:

DRI shaft furnace technology is already proven, and hydrogen-ready plant designs are available. [2][3]

Hydrogen-only operations are still in the demonstration stage. [2][3]

U.S. federal funding and tax credit timelines remain volatile, which makes planning harder for long-lived industrial assets. [5]

That is why the biggest near-term opening may come at blast furnace reline deadlines. When a producer has to make a major capital decision anyway, building around DRI-EAF can keep the door open for hydrogen later, even if the plant starts on natural gas. [4]

Those tradeoffs lead straight to the next issue: what has to change for hydrogen steelmaking to scale?

Solutions: How to Address the Main Barriers to Hydrogen Steelmaking

Technology, Infrastructure, and Policy Actions

These barriers call for three things at the same time: lower-cost hydrogen, more clean power, and less project risk. No single group can push hydrogen steelmaking ahead on its own. Steel producers, energy suppliers, equipment makers, investors, and public agencies all have to line up their moves with care.

On the technology side, the most practical near-term step is to blend hydrogen into existing natural gas DRI plants before jumping to 100% hydrogen systems. That gives producers a lower-risk way to learn by doing. Thermal efficiency matters here as well. In hot charging setups, sponge iron moves straight into the EAF at about 1,300°F (700°C), which cuts energy losses in a meaningful way. Using EAF off-gas to preheat hydrogen can lift the break-even hydrogen price by up to $0.07/kg, which helps project economics. [2]

Grid upgrades and regional hydrogen hubs also need to move in step with plant investment. If one side gets ahead of the other, projects can stall. Methanol-based LOHCs may also cost less than compressed-gas storage for on-site storage and heat integration. [2]

Policy needs to do three jobs: build demand, cut first-of-a-kind (FOAK) project risk, and protect low-carbon steel from higher-emission imports. A Carbon Border Adjustment Mechanism (CBAM) would help shield domestic low-carbon producers from cheaper, higher-emission competition. Green procurement rules can also support the first wave of demand. One example is the Buy Clean California Act, which sets a limit of 1.38 metric tons of CO₂ per metric ton of hot-rolled steel. [3] Public-private risk-sharing for FOAK facilities matters just as much, since private investors alone are unlikely to take on the full cost of proving new plant designs at commercial scale.

Planning Steps for U.S. Decision-Makers

For mills facing big reinvestment calls, the next step is not commitment. It is comparison. Many U.S. steel facilities will hit reinvestment deadlines by 2030, so scenario analysis should test hydrogen prices, carbon costs, and policy timing before any capital is locked in.

For producers, scenario analysis is the right place to start. Investors should also watch feedstock quality closely. Hydrogen DRI processes need iron ore pellets with at least 67% iron content, and projects built around lower-grade ore face plain cost and performance risks. [1] Public agencies, meanwhile, need to put grid upgrades first in the Great Lakes and Southern regions, where steel production is clustered and where hydrogen hub development makes the most regional sense. [1]

Barrier-to-Solution Mapping

The main obstacles tie back to a short list of actions.

Barrier | Solution Type | Responsible Actors | Likely Timeline |

|---|---|---|---|

Hydrogen cost | Electrolyzer efficiency gains; hydrogen hubs | Electrolyzer makers, DOE, energy suppliers | 2026–2030 |

Clean power supply gaps | Grid upgrades; GW-scale renewables buildout | Utilities, energy suppliers, regulators | 2025–2035 |

High capital risk (FOAK) | Public-private risk-sharing; subsidies | Government, investors, steel producers | 2025–2030 |

Market competitiveness | CBAM; green public procurement | Policymakers, public agencies | 2024–2027 |

Feedstock quality (ore grade) | More DR-grade pellet supply and ore beneficiation | Mining companies, steel producers | 2025–2030 |

Conclusion: Hydrogen's Role in the Future of U.S. Steel

Hydrogen can help decarbonize U.S. steel, but scaling it is still the hard part. H2-DRI remains the lowest-carbon route now on the table, yet high costs, power demand, and iron ore feedstock limits still slow adoption at full industrial scale. [2]

Timing is just as important as the tech itself. That pressure shows up most clearly when mills face major reline decisions, because capital choices made before 2030 will shape steelmaking paths for decades. [4] For producers and policymakers, the job now is simple in theory and tough in practice: line up power, ore, and sustainable business capital plans before those decision windows shut. With federal hydrogen support looking less certain after the cancellation of over $2 billion in DOE hydrogen hub funding in October 2025 [4], state-level action is now doing more of the heavy lifting.

The path forward is clear: align power, ore, and capital plans before the next reline cycle.

FAQs

Why is green hydrogen still too expensive for steelmaking?

Green hydrogen is still too expensive for steelmaking. For most producers, the math just doesn’t work yet.

To compete with established natural gas-based processes, green hydrogen usually needs to land below $1.70–$2.00 per kilogram. Today, it often sits closer to $4–$8 per kilogram. That gap is the main problem.

A big reason comes down to electricity. Power accounts for 60–70% of green hydrogen production costs, which means high electricity prices can quickly wreck project economics. Limited access to low-cost renewable energy makes that challenge even tougher.

There’s also a policy issue. Without strong enough carbon pricing or government incentives, H2-DRI has a hard time competing with coal-based steelmaking. Put simply, cleaner production is available, but in many cases the market still rewards the cheaper, older route.

Can U.S. power grids support hydrogen-based steel plants?

It comes down to both technical limits and cost. Hydrogen-based steelmaking needs a large, steady flow of electricity to run electrolyzers. In many cases, tying a plant into the existing grid isn’t simple. Interconnection can take years, and the price tag can be high.

That’s why many experts look to off-grid hydrogen production powered by renewables. Putting hydrogen production next to wind or solar projects can ease grid and transmission bottlenecks. On top of that, hydrogen storage can help smooth out the ups and downs of renewable power, giving steel mills a more stable energy supply even though their demand stays constant.

Is natural gas DRI the most practical bridge to hydrogen steel?

Yes. Natural gas direct reduced iron (DRI) is widely seen as a practical bridge to hydrogen-based steelmaking.

Existing DRI shaft furnaces already run on hydrogen and carbon monoxide made from natural gas. That means steel producers don't have to rip everything out and start from scratch. In many cases, they can retrofit these systems to use a higher share of hydrogen over time.

That step-by-step path matters. It gives producers room to shift as green hydrogen supply expands and costs come down, without taking on a full facility overhaul all at once.

Related Blog Posts

FAQ

01

What does it really mean to “redefine profit”?

02

What makes Council Fire different?

03

Who does Council Fire you work with?

04

What does working with Council Fire actually look like?

05

How does Council Fire help organizations turn big goals into action?

06

How does Council Fire define and measure success?

Jul 7, 2026

Hydrogen in Steelmaking: Opportunities and Barriers

Sustainability Strategy

In This Article

Hydrogen can cut U.S. steel emissions to near zero, but high H₂ costs, massive power needs, ore limits, and policy risk block scale-up.

Hydrogen in Steelmaking: Opportunities and Barriers

Hydrogen can cut steel emissions to near zero, but in the U.S. the main block is cost. From what I see in this article, hydrogen-based steelmaking has a clear upside on emissions, yet it still runs into four hard limits at once: high hydrogen prices, huge power demand, heavy upfront spending, and policy swings.

If I boil it down, the article says:

Steel matters for emissions:U.S. steel made up about 87 million metric tons of output in 2023, and the sector accounts for about 2% of U.S. greenhouse gas emissions.

Hydrogen changes the core step: In hydrogen DRI, H₂ removes oxygen from iron ore and makes water vapor instead of CO₂.

The cost gap is still large: Green hydrogen needs to fall to about $1.63 to $1.70 per kilogram to compete, but today it is about $3 to $6 per kilogram.

Power needs are huge: A plant making 1 million tons per year may need about 500 MW of constant power, which can mean roughly 1 to 2 GW of wind and solar capacity.

Capital timing matters: A blast furnace reline can cost about $350 million, but a move to DRI-EAF with hydrogen needs much more site-wide spending.

Raw materials matter too: Hydrogen DRI needs high-quality DR-grade pellets, and much of the U.S. ore base needs more processing first.

Policy can speed up or slow down projects: Federal funding cuts and tighter tax credit deadlines have made planning harder.

The near-term path is mixed: Many mills may start with natural gas DRI-EAF or hydrogen blending first, then shift later if fuel, power, and policy line up.

My short take: hydrogen steelmaking is not blocked by chemistry. It is blocked by project economics and system buildout. For U.S. steelmakers, the biggest decision point is often not whether hydrogen can work, but when it makes sense to commit before the next major furnace reline.

Decarbonization 102-Hydrogen Ironmaking-Managing Expectations of H2 Transformation & Its Many Colors

Quick Comparison

Route | Emissions | Main Input | Cost Risk | Market Status |

|---|---|---|---|---|

BF-BOF | Highest | Coal/coke | Lower if asset already exists | Full-scale use |

NG-DRI-EAF | Lower | Natural gas | Mid-range | Full-scale use |

H2-DRI-EAF | Lowest | Green hydrogen | Highest | Early-stage rollout |

In short: the article points to hydrogen as the lowest-emissions route, but not yet the easiest one to build at scale in the United States.

The Core Problem: Why Hydrogen Steelmaking Is Hard to Scale

Hydrogen vs. Traditional Steelmaking: Emissions, Cost & Maturity Compared

Hydrogen steelmaking is hard to scale in the U.S. because several barriers land at the same time: fuel cost, power demand, capital spend, and policy risk. The chemistry works. The hard part is building the full system around it at industrial scale. A few early project wins don't change that bigger reality.

Cost, Power, and Capital Constraints

The biggest hurdle is still the price of green hydrogen. For H2-DRI to compete with today's natural-gas DRI, hydrogen procurement costs need to drop to about $1.63 to $1.70 per kilogram[6]. At the moment, green hydrogen sits around $3 to $6 per kilogram[3]. That's a big gap, and steelmakers feel every dollar of it.

Power needs make the math even tougher. A single steel plant producing 1 million tons per year needs about 500 MW of continuous electricity. Since wind and solar don't run at full output all day, that usually means roughly 1 to 2 GW of renewable capacity[6]. LBNL notes that one integrated steel mill can demand gigawatts of renewable generation and electrolysis capacity[6]. In plain terms, one mill can soak up a huge share of a region's clean power build-out.

Then there's the capital bill. Relining one large blast furnace costs about $350 million[4]. Moving to a full DRI-EAF route costs far more, with new spending needed for electrolyzers, shaft furnaces, hydrogen storage, and plant changes across the site. U.S. Steel, for instance, said it would reline the Gary Works No. 14 blast furnace in Indiana, a $350 million project that keeps the coal-based asset running for another 20 years[4]. That kind of choice shows the bind steelmakers are in: pay a large sum to extend what already exists, or spend much more to switch to a new route with less operating history.

Policy risk makes lenders and executives even more cautious. In October 2025, the U.S. Department of Energy canceled more than $2 billion in funding for West Coast hydrogen hubs[4]. The "One Big Beautiful Bill Act" also moved the construction start deadline for clean hydrogen tax credits from 2032 to 2027, and about 75% of projects in the pipeline are not expected to hit that date[5]. As RMI noted:

"Capital decisions made before 2030 will lock in US steelmaking pathways for decades, as blast furnaces approach costly reline deadlines." - RMI [4]

Supply Chain and Operational Limits

Even if the money showed up tomorrow, the supply chain would still be tight. H2-DRI works best with DR-grade iron ore pellets that are low in silica and highly porous. Much of the U.S. iron ore base is taconite, or magnetite, which is less porous, reduces more slowly, and needs extra processing before it fits a hydrogen shaft furnace[3][6]. So this isn't just a fuel switch. For many U.S. mills, it's also a raw-material and plant-design problem.

Electrolyzers are another choke point. A 2-million-ton-per-year iron plant would need about 1 GW of electrolyzer capacity[3]. Storage adds another layer of cost. Compressed hydrogen storage is expensive and energy intensive, while liquid carriers like methanol are still being studied[6].

There is also a process issue inside the mill. H2-DRI makes sponge iron without carbon, unlike natural gas DRI, which keeps some carbon in the product. That means mills have to add carbon later in the EAF to meet certain grade needs[6]. It's one more step, and one more design choice that has to work cleanly at scale.

Steelmaking Routes Compared

The table below puts the three main steelmaking routes next to each other. H2-DRI has the lowest emissions by far, but it also comes with the biggest capital burden and the least operating track record.

Route | CO₂ Emissions (tons/ton of steel) | Primary Fuel/Reductant | Capital Intensity | Technology Maturity |

|---|---|---|---|---|

BF-BOF | 1.8–2.33 [7] | Metallurgical coal/coke | High (existing assets) | Commercial |

NG-DRI-EAF | 0.66–1.37 [7] | Natural gas | Moderate | Commercial |

H2-DRI-EAF | <0.05–0.2 [7] | Green hydrogen | Very high (new build) | Demonstration/Pilot |

The pattern is pretty stark. BF-BOF is proven but carbon-heavy. NG-DRI-EAF cuts emissions and already runs at scale. H2-DRI-EAF offers the deepest emissions drop, yet it asks companies to take on the most risk upfront with the fewest full-scale examples to lean on. That helps explain why pilot projects are moving ahead faster than full commercial conversion.

Opportunities: Where Hydrogen Creates Value for Steel Producers

Emissions Reduction and Market Competitiveness

The clearest source of value in hydrogen steelmaking is lower emissions. That edge starts to matter a lot more when buyers and policymakers put a price on carbon. Natural gas DRI already cuts emissions by about 35% to 40% compared with blast furnace steel, which makes it a practical step between today's system and hydrogen-based production. [2][3]

Policy is already starting to shape demand. The Buy Clean California Act sets carbon-intensity limits for steel used in state construction projects. For hot-rolled steel, the limit is below 1.38 metric tons of CO₂ per metric ton. [3] Similar green procurement rules are spreading across the U.S., Japan, South Korea, and South Africa. [3] At that point, this is no longer just about public image. It becomes a question of who can still sell into key markets.

For steelmakers that still rely on blast furnaces, the pressure is building from both carbon pricing and tighter rules. As SSAB's Chief Technology Officer Martin Pei put it:

"We believe that in the long run, this will become even more competitive, since we know that emission costs will go up. Society is really pushing in that direction, and we believe there is a good business case." [3]

What Early Projects Show

Early projects are now testing whether this value holds up once companies face plant economics, fuel costs, and policy swings. HYBRIT stands out as the clearest proof point. It shows that hydrogen DRI is technically feasible and has already moved beyond the pilot stage into early commercial planning. [3]

That said, the picture in the U.S. is uneven. Hyundai moved ahead with a green steel mill in Louisiana, while Cleveland-Cliffs canceled a hydrogen project in Ohio after federal policy uncertainty. [5] That split tells its own story: the technology may be moving forward, but investment still depends on whether companies trust the rules of the game.

RMI's Kaitlyn Ramirez, Manager of Iron and Steel, put the logic plainly:

"When you first make the investment, it enables a pathway to leverage hydrogen as we build up the infrastructure, as the costs decline, and as the technology is de-risked to shift from gas-based production to hydrogen." [4]

Benefits vs. Risks of Hydrogen-Based Steel

Hydrogen-based steel brings two big upsides: deep emissions cuts and less reliance on imported coal and coke, which helps with energy security. But the costs are hard to ignore. Early production can carry a 20% to 30% cost premium over conventional steel. [3]

The setup is a bit of a mixed bag:

DRI shaft furnace technology is already proven, and hydrogen-ready plant designs are available. [2][3]

Hydrogen-only operations are still in the demonstration stage. [2][3]

U.S. federal funding and tax credit timelines remain volatile, which makes planning harder for long-lived industrial assets. [5]

That is why the biggest near-term opening may come at blast furnace reline deadlines. When a producer has to make a major capital decision anyway, building around DRI-EAF can keep the door open for hydrogen later, even if the plant starts on natural gas. [4]

Those tradeoffs lead straight to the next issue: what has to change for hydrogen steelmaking to scale?

Solutions: How to Address the Main Barriers to Hydrogen Steelmaking

Technology, Infrastructure, and Policy Actions

These barriers call for three things at the same time: lower-cost hydrogen, more clean power, and less project risk. No single group can push hydrogen steelmaking ahead on its own. Steel producers, energy suppliers, equipment makers, investors, and public agencies all have to line up their moves with care.

On the technology side, the most practical near-term step is to blend hydrogen into existing natural gas DRI plants before jumping to 100% hydrogen systems. That gives producers a lower-risk way to learn by doing. Thermal efficiency matters here as well. In hot charging setups, sponge iron moves straight into the EAF at about 1,300°F (700°C), which cuts energy losses in a meaningful way. Using EAF off-gas to preheat hydrogen can lift the break-even hydrogen price by up to $0.07/kg, which helps project economics. [2]

Grid upgrades and regional hydrogen hubs also need to move in step with plant investment. If one side gets ahead of the other, projects can stall. Methanol-based LOHCs may also cost less than compressed-gas storage for on-site storage and heat integration. [2]

Policy needs to do three jobs: build demand, cut first-of-a-kind (FOAK) project risk, and protect low-carbon steel from higher-emission imports. A Carbon Border Adjustment Mechanism (CBAM) would help shield domestic low-carbon producers from cheaper, higher-emission competition. Green procurement rules can also support the first wave of demand. One example is the Buy Clean California Act, which sets a limit of 1.38 metric tons of CO₂ per metric ton of hot-rolled steel. [3] Public-private risk-sharing for FOAK facilities matters just as much, since private investors alone are unlikely to take on the full cost of proving new plant designs at commercial scale.

Planning Steps for U.S. Decision-Makers

For mills facing big reinvestment calls, the next step is not commitment. It is comparison. Many U.S. steel facilities will hit reinvestment deadlines by 2030, so scenario analysis should test hydrogen prices, carbon costs, and policy timing before any capital is locked in.

For producers, scenario analysis is the right place to start. Investors should also watch feedstock quality closely. Hydrogen DRI processes need iron ore pellets with at least 67% iron content, and projects built around lower-grade ore face plain cost and performance risks. [1] Public agencies, meanwhile, need to put grid upgrades first in the Great Lakes and Southern regions, where steel production is clustered and where hydrogen hub development makes the most regional sense. [1]

Barrier-to-Solution Mapping

The main obstacles tie back to a short list of actions.

Barrier | Solution Type | Responsible Actors | Likely Timeline |

|---|---|---|---|

Hydrogen cost | Electrolyzer efficiency gains; hydrogen hubs | Electrolyzer makers, DOE, energy suppliers | 2026–2030 |

Clean power supply gaps | Grid upgrades; GW-scale renewables buildout | Utilities, energy suppliers, regulators | 2025–2035 |

High capital risk (FOAK) | Public-private risk-sharing; subsidies | Government, investors, steel producers | 2025–2030 |

Market competitiveness | CBAM; green public procurement | Policymakers, public agencies | 2024–2027 |

Feedstock quality (ore grade) | More DR-grade pellet supply and ore beneficiation | Mining companies, steel producers | 2025–2030 |

Conclusion: Hydrogen's Role in the Future of U.S. Steel

Hydrogen can help decarbonize U.S. steel, but scaling it is still the hard part. H2-DRI remains the lowest-carbon route now on the table, yet high costs, power demand, and iron ore feedstock limits still slow adoption at full industrial scale. [2]

Timing is just as important as the tech itself. That pressure shows up most clearly when mills face major reline decisions, because capital choices made before 2030 will shape steelmaking paths for decades. [4] For producers and policymakers, the job now is simple in theory and tough in practice: line up power, ore, and sustainable business capital plans before those decision windows shut. With federal hydrogen support looking less certain after the cancellation of over $2 billion in DOE hydrogen hub funding in October 2025 [4], state-level action is now doing more of the heavy lifting.

The path forward is clear: align power, ore, and capital plans before the next reline cycle.

FAQs

Why is green hydrogen still too expensive for steelmaking?

Green hydrogen is still too expensive for steelmaking. For most producers, the math just doesn’t work yet.

To compete with established natural gas-based processes, green hydrogen usually needs to land below $1.70–$2.00 per kilogram. Today, it often sits closer to $4–$8 per kilogram. That gap is the main problem.

A big reason comes down to electricity. Power accounts for 60–70% of green hydrogen production costs, which means high electricity prices can quickly wreck project economics. Limited access to low-cost renewable energy makes that challenge even tougher.

There’s also a policy issue. Without strong enough carbon pricing or government incentives, H2-DRI has a hard time competing with coal-based steelmaking. Put simply, cleaner production is available, but in many cases the market still rewards the cheaper, older route.

Can U.S. power grids support hydrogen-based steel plants?

It comes down to both technical limits and cost. Hydrogen-based steelmaking needs a large, steady flow of electricity to run electrolyzers. In many cases, tying a plant into the existing grid isn’t simple. Interconnection can take years, and the price tag can be high.

That’s why many experts look to off-grid hydrogen production powered by renewables. Putting hydrogen production next to wind or solar projects can ease grid and transmission bottlenecks. On top of that, hydrogen storage can help smooth out the ups and downs of renewable power, giving steel mills a more stable energy supply even though their demand stays constant.

Is natural gas DRI the most practical bridge to hydrogen steel?

Yes. Natural gas direct reduced iron (DRI) is widely seen as a practical bridge to hydrogen-based steelmaking.

Existing DRI shaft furnaces already run on hydrogen and carbon monoxide made from natural gas. That means steel producers don't have to rip everything out and start from scratch. In many cases, they can retrofit these systems to use a higher share of hydrogen over time.

That step-by-step path matters. It gives producers room to shift as green hydrogen supply expands and costs come down, without taking on a full facility overhaul all at once.

Related Blog Posts

FAQ

What does it really mean to “redefine profit”?

What makes Council Fire different?

Who does Council Fire you work with?

What does working with Council Fire actually look like?

How does Council Fire help organizations turn big goals into action?

How does Council Fire define and measure success?