Feb 23, 2026

How to Measure and Report ESG Impact Effectively for Corporations

ESG Strategy

In This Article

Clear, step-by-step guide to identify material ESG issues, choose frameworks, collect audit-ready data, verify metrics, and link ESG reporting to business value.

How to Measure and Report ESG Impact Effectively for Corporations

Measuring and reporting ESG (Environmental, Social, and Governance) impact is now a critical business requirement. Investors demand transparency, regulators enforce stricter standards, and consumers prioritize sustainability. This guide outlines a clear, step-by-step approach to help corporations navigate ESG reporting challenges, select the right frameworks, and improve data accuracy.

Key Takeaways:

Identify Material ESG Issues: Focus on what matters most to your business and stakeholders using materiality assessments, including double materiality for broader insights.

Choose the Right Framework: Options include GRI, SASB, ISSB, ESRS, and CDP, each tailored to specific audiences and goals.

Collect Accurate Data: Build systems for traceable, audit-ready ESG data, leveraging existing platforms like SAP or Oracle.

Verify and Structure Reports: Ensure data accuracy through internal controls and independent validation. Organize reports around governance, strategy, risk management, and metrics.

Align ESG with Business Goals: Use ESG reporting to identify cost savings, reduce risks, and strengthen stakeholder trust.

Why It Matters:

90% of S&P 500 companies now publish sustainability reports, up from 20% in 2011.

76% of investors trust independently verified ESG data, and 72% of Gen Z consumers are willing to pay more for sustainable products.

By following these principles, corporations can meet regulatory demands, build trust, and turn ESG efforts into measurable business value.

Step 1: Identify Material ESG Issues Through Assessments

How to Determine Material ESG Issues

Pinpointing material ESG (Environmental, Social, and Governance) issues is essential for credible and effective reporting. Materiality refers to identifying the topics that have the greatest impact on your organization’s economic, environmental, and social performance [6]. The process involves narrowing down a wide range of ESG concerns to focus only on those that are most relevant to your business and stakeholders.

Here’s how you can approach this:

Understand your organizational context: Map out your business activities, geographical footprint, and the stakeholders you interact with - both internally and externally [6].

Identify impacts: Look across your value chain to uncover both negative effects that need addressing and positive contributions you can amplify [6][8].

Assess significance: Use both quantitative and qualitative methods to evaluate the severity, likelihood, scale, and scope of these impacts [6].

Prioritize key issues: Focus on the most significant impacts for reporting purposes and integrate them into your overall strategy [6][8].

Engaging with stakeholders is a critical part of this process. Collaboration with internal teams, investors, suppliers, customers, and local communities can provide valuable insights [8]. Surveys are particularly useful, enabling stakeholders to rank ESG issues based on their perceived impact on business performance [8]. Where direct consultation isn’t feasible, input from independent experts, such as NGOs or academics, can help fill the gap [6].

"As in financial reporting, you need to provide your stakeholders with information about the topics that matter and ensure less-relevant information doesn't get in the way." – KPMG [8]

Organizations that embed sustainability into their operations often see tangible benefits. Companies with strong sustainability practices report 16% higher revenue growth and are 52% more likely to excel in profitability [8]. For private firms, sustainability can boost EBITDA by 4% to 7%, while also increasing exit multiples by up to 7% [8]. Additionally, companies that disclose materiality assessments experience a 36% rate of shareholder proposal withdrawals, compared to 29% for those that don’t - indicating better stakeholder engagement [7].

This groundwork sets the stage for applying a double-lens approach to refine and deepen the understanding of ESG impacts.

Understanding Double Materiality

Double materiality builds on traditional materiality assessments by introducing a dual perspective. It considers two lenses:

Impact Materiality: Focuses on how your company’s activities affect society and the environment - an "inside-out" view [9].

Financial Materiality: Examines how ESG factors influence your company’s financial performance, cash flow, and access to capital - an "outside-in" perspective [9].

This concept plays a central role in the EU's Corporate Sustainability Reporting Directive (CSRD) and European Sustainability Reporting Standards (ESRS) [9].

An issue may be material from one perspective but not the other. For example, Telefónica, a Spanish telecommunications company, identified greenhouse gas emissions as material from both perspectives in its 2021 assessment. However, water and wastewater management was deemed material only from an impact perspective, while risk and critical incidents management was viewed as material only from a financial standpoint [9]. This dual approach ensures that critical environmental and social issues are not overlooked, even if they don’t directly affect financial outcomes under traditional frameworks.

The adoption of double materiality is gaining momentum worldwide. In 2023, 16 out of 47 European companies explicitly used this framework in their reports [9]. Meanwhile, in the Asia-Pacific region, about 51% of companies have incorporated double materiality as part of their net-zero strategies [9].

To implement this approach, start by mapping your value chain, covering all entities you control or influence, including suppliers and partners [9][6]. Then, identify specific Impacts, Risks, and Opportunities (IROs) to evaluate over short-, medium-, and long-term horizons [9]. Finally, present your findings in a double materiality matrix, which plots issues along two axes: "Impact on People/Environment" and "Financial Influence on the Company" [9].

This structured approach ensures a comprehensive view of ESG priorities, aligning both societal and financial considerations.

How to build a modern ESG reporting framework | Understanding standards, metrics and challenges

Step 2: Select the Right ESG Reporting Framework

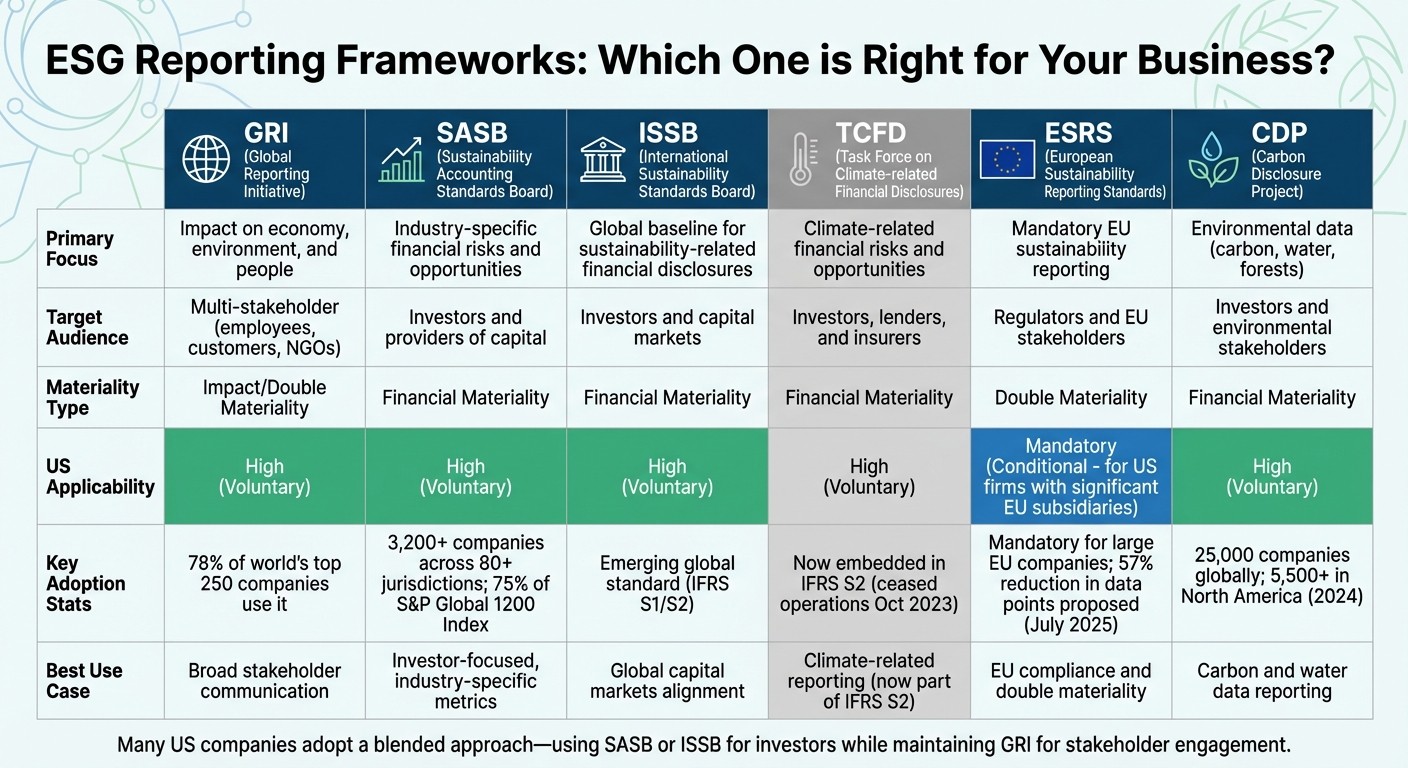

ESG Reporting Frameworks Comparison Guide for US Corporations

Main ESG Reporting Frameworks Explained

Once material ESG issues are identified, the next step is choosing the right reporting framework. This decision is essential for creating transparent and effective ESG reports. With various frameworks available, each designed for specific purposes and audiences, understanding their focus can help align your reporting strategy with both your business goals and stakeholder needs.

GRI (Global Reporting Initiative) emphasizes a broad stakeholder approach, addressing how a company impacts the economy, environment, and people. It’s widely adopted, with 78% of the world’s top 250 companies using it [12]. GRI is particularly effective for communicating with diverse groups, including employees, customers, NGOs, and local communities. Its modular structure combines universal standards with sector-specific guidance tailored to different industries [1][12].

SASB (Sustainability Accounting Standards Board) zeroes in on financial materiality, offering industry-specific metrics across 77 sectors. Over 3,200 companies across more than 80 jurisdictions, including 75% of the S&P Global 1200 Index, use SASB Standards [10]. This framework highlights ESG topics most likely to influence financial performance and shareholder value. Now overseen by the IFRS Foundation, SASB Standards are designed for investor disclosures and are freely accessible.

ISSB (International Sustainability Standards Board) is emerging as a global baseline for sustainability reporting. It integrates SASB and TCFD into two unified standards: IFRS S1 (General Requirements for Disclosure of Sustainability-related Financial Information) and IFRS S2 (Climate-related Disclosures) [10][11]. Targeting investors, ISSB provides consistent and comparable disclosures.

"As the regulatory agenda intensifies, companies that can pivot quickly and approach ESG reporting strategically will be able to move from simple compliance to creating a clear competitive advantage for their organizations" [11].

Stephanie Jamison, Jens Laue, and Michela Coppola, Accenture

TCFD (Task Force on Climate-related Financial Disclosures), which ceased operations in October 2023, has its recommendations embedded within IFRS S2 [11][13]. TCFD focused on climate-related financial risks and opportunities through four pillars: Governance, Strategy, Risk Management, and Metrics and Targets. Today, its principles are foundational to climate reporting under IFRS S2.

ESRS (European Sustainability Reporting Standards), developed under the EU’s Corporate Sustainability Reporting Directive (CSRD), is mandatory for large companies operating in the European Union, including U.S. corporations with significant EU subsidiaries [11][3]. ESRS requires "double materiality" reporting, assessing both how sustainability issues affect the business and how the business impacts society and the environment. Proposed amendments in July 2025 aim to reduce reporting burdens by cutting mandatory data points by 57% [11].

CDP (formerly Carbon Disclosure Project) focuses on environmental data, including carbon emissions, water, and forests. In 2024, nearly 25,000 companies globally, including over 5,500 in North America, utilized the CDP system [11]. CDP works well as a complementary tool for investors and customers seeking detailed environmental performance data.

Choosing the right framework hinges on three key factors: your primary audience (investors versus a broader group of stakeholders), your industry's specific risks and opportunities, and regulatory requirements. Many U.S. companies adopt a blended approach - using SASB or ISSB for investor-focused reporting while maintaining GRI disclosures for broad stakeholder engagement. This dual strategy aligns with trends like the 59% of individual investors in early 2025 who planned to increase sustainable investments within 12 months [11].

Framework Comparison Table

Here’s a quick comparison of major frameworks to guide U.S.-based corporations in their selection:

| Framework | Primary Focus | Target Audience | Materiality Type | Applicability for U.S. Corps | Key Reason for Use |

| --- | --- | --- | --- | --- | --- |

| <strong>GRI</strong> | Impact on economy, environment, and people | Multi-stakeholder (employees, customers, NGOs) | Impact/Double Materiality | High (Voluntary) | Widely used for broad stakeholder communication |

| <strong>SASB</strong> | Industry-specific financial risks and opportunities | Investors and providers of capital | Financial Materiality | High (Voluntary) | Preferred by U.S. investors for industry-specific metrics |

| <strong>ISSB (IFRS S1/S2)</strong> | Global baseline for sustainability-related financial disclosures | Investors and capital markets | Financial Materiality | High (Voluntary) | Emerging standard for global capital markets |

| <strong>TCFD</strong> | Climate-related financial risks and opportunities | Investors, lenders, and insurers | Financial Materiality | High (Voluntary) | Now part of IFRS S2; essential for climate-related reporting |

| <strong>ESRS (EU)</strong> | Mandatory EU sustainability reporting | Regulators and EU stakeholders | Double Materiality | Mandatory (Conditional) | Required for U.S. firms with significant EU subsidiaries |

| <strong>CDP</strong> | Environmental data (carbon, water, forests) | Investors and environmental stakeholders | Financial Materiality | High (Voluntary) | Standard for carbon and water data reporting

| Framework | Primary Focus | Target Audience | Materiality Type | Applicability for U.S. Corps | Key Reason for Use |

| --- | --- | --- | --- | --- | --- |

| <strong>GRI</strong> | Impact on economy, environment, and people | Multi-stakeholder (employees, customers, NGOs) | Impact/Double Materiality | High (Voluntary) | Widely used for broad stakeholder communication |

| <strong>SASB</strong> | Industry-specific financial risks and opportunities | Investors and providers of capital | Financial Materiality | High (Voluntary) | Preferred by U.S. investors for industry-specific metrics |

| <strong>ISSB (IFRS S1/S2)</strong> | Global baseline for sustainability-related financial disclosures | Investors and capital markets | Financial Materiality | High (Voluntary) | Emerging standard for global capital markets |

| <strong>TCFD</strong> | Climate-related financial risks and opportunities | Investors, lenders, and insurers | Financial Materiality | High (Voluntary) | Now part of IFRS S2; essential for climate-related reporting |

| <strong>ESRS (EU)</strong> | Mandatory EU sustainability reporting | Regulators and EU stakeholders | Double Materiality | Mandatory (Conditional) | Required for U.S. firms with significant EU subsidiaries |

| <strong>CDP</strong> | Environmental data (carbon, water, forests) | Investors and environmental stakeholders | Financial Materiality | High (Voluntary) | Standard for carbon and water data reporting

Starting with a materiality assessment helps map stakeholder needs and determine the best framework. For investor-focused goals, SASB or ISSB offer industry-specific, globally comparable insights. Companies with diverse stakeholder groups or EU operations may find GRI or ESRS more suitable. Many organizations also leverage tools like CDP and GRI to identify overlapping data points, streamlining their reporting process. This interoperability reduces duplication, allowing data to serve multiple frameworks efficiently.

Step 3: Collect and Measure ESG Data

Set Up Data Collection Systems

Creating an effective ESG data system starts with building a detailed inventory of all data sources. This inventory should outline the specific data needed, where it currently resides, how it will be utilized, and its long-term storage plan [5]. Without this step, you risk overlooking important information or duplicating efforts across teams.

Assign clear accountability roles to maintain data quality throughout the process. Designate an ESG Controller to lead operations, supported by three key roles: Information Owners, who ensure accuracy at the source; Disclosure Owners, who certify data before it enters reports; and independent Validators, who provide an objective review [5]. This structured approach ensures that every stage of data collection is managed responsibly.

Rather than creating a standalone ESG reporting system, integrate these processes into your existing enterprise platforms. Systems like Oracle, SAP, or Workday, commonly used for financial reporting, can also handle ESG data [5][15]. For frequently updated metrics - like energy usage or business travel - establish API connections to automatically pull data from utility providers or travel management systems [15]. Automation not only reduces manual tracking but also minimizes errors.

To ensure accuracy, trace every metric from its original source through all transformations to its final report format. This process helps pinpoint where controls are needed and uncovers any data gaps. Conduct a data gap analysis early in the reporting cycle to address issues before deadlines become a concern. This proactive approach allows time for data cleansing and remediation.

With a solid framework for data collection in place, the next critical step is to verify the accuracy of your ESG data.

Verify Data Accuracy

Verification is essential for ensuring the integrity of your ESG disclosures. Start by conducting quality assessments (QA) to check for accuracy, completeness, and reliable calculations before data is transferred to the final reporting system [5]. These assessments help catch errors early, reducing risks to your report’s credibility and preparing the data for independent attestation - a level of assurance that 85% of investors now expect, akin to financial audits [5].

Ensure internal controls are in place by aligning the data and assumptions used for ESG disclosures with those in your financial statements [14]. This consistency is crucial, as both regulators and auditors will compare your sustainability metrics with your financial filings. As noted in the IFRS S1 standard:

"For sustainability-related financial information to be useful, it must be relevant and faithfully represent what it purports to represent" [14].

Independent reviewers should be able to confirm that your data accurately supports your claims.

To meet regulatory and investor expectations, maintain ESG data in compliance with company policies and ensure it is "investor-grade" [5]. This involves documenting data sources, using transparent calculation methods, and maintaining traceable audit trails. With 76% of investors expressing greater confidence in sustainability information that has been independently assured [4], third-party verification is becoming a crucial step. Organize and store all supporting documentation systematically to facilitate efficient audits.

The table below outlines the key steps for verifying ESG data:

| Verification Step | Description | Key Objective |

| --- | --- | --- |

| Data Source Inventory | Catalog all origins of ESG-related data | Ensure completeness and identify gaps |

| Metric Walkthrough | Trace data from source to final report | Verify accuracy and internal controls |

| Quality Assessment (QA) | Test calculations and cleanse data | Ensure reliability of metrics |

| Independent Validation | Review by an external, unbiased party | Enhance credibility and prepare for audit |

| External Attestation | Third-party audit (limited or reasonable assurance) | Build stakeholder trust

| Verification Step | Description | Key Objective |

| --- | --- | --- |

| Data Source Inventory | Catalog all origins of ESG-related data | Ensure completeness and identify gaps |

| Metric Walkthrough | Trace data from source to final report | Verify accuracy and internal controls |

| Quality Assessment (QA) | Test calculations and cleanse data | Ensure reliability of metrics |

| Independent Validation | Review by an external, unbiased party | Enhance credibility and prepare for audit |

| External Attestation | Third-party audit (limited or reasonable assurance) | Build stakeholder trust

Step 4: Structure Your ESG Report

Core Sections of an ESG Report

Once you've gathered comprehensive ESG data, the next step is organizing your report effectively. A well-structured ESG report typically revolves around four key pillars - Governance, Strategy, Risk Management, and Metrics and Targets - aligned with TCFD and ISSB guidelines [14].

Governance: This section highlights the individuals or committees responsible for overseeing ESG efforts. Detail their roles, responsibilities, and how they stay informed on sustainability matters. Additionally, outline how ESG performance metrics are tied to executive compensation.

Strategy: Explain how ESG-related risks and opportunities influence your business model, value chain, and financial planning. Include an analysis of your organization's ability to adapt to these challenges.

Risk Management: Describe the processes for identifying, monitoring, and mitigating ESG risks. This should also include scenario analyses to demonstrate preparedness for potential challenges.

Metrics and Targets: Share the performance indicators you track and provide updates on progress toward your ESG goals. Ensure that ESG disclosures align with the same reporting entity and currency as your financial statements to maintain consistency and comparability [14].

For businesses operating within or serving the European Union, it’s essential to address double materiality. This means reporting on both the financial risks arising from ESG issues and the organization's broader impact on the environment and society [4].

Once your report framework is established, incorporate stakeholder feedback to refine and enhance your disclosures.

Include Stakeholder Input

Identifying and engaging with key stakeholders - such as investors, employees, customers, suppliers, regulators, and civil society - is critical [16][2]. Conduct double materiality assessments to ensure the report addresses topics that are both significant for business performance and important to stakeholders. Aligning these insights with your strategic objectives enhances the report's relevance and effectiveness.

Engage internal experts and leadership to validate technical data and ensure ESG priorities align with your broader business strategy [16]. As Paul Gassett, CEO of OBATA, notes:

"Effective ESG reporting requires a deliberate blend of analytical rigor and strategic communication. High-quality sustainability reports strengthen stakeholder confidence, reduce information asymmetry, and support more effective engagement with investors and regulators." [16]

Keep stakeholders informed on a regular basis - quarterly or semiannually - using accessible formats like landing pages, infographics, or short videos to maintain engagement and transparency [16].

Step 5: Use ESG Reporting to Create Business Value

Connect ESG Reporting to Business Goals

Tying ESG reporting to business objectives can unlock measurable financial gains and position companies for long-term success. Companies that integrate ESG into their core strategies and continuously adapt - referred to as "Reinventors" - have shown remarkable financial performance. Between 2019 and 2022, these companies achieved a 15-percentage-point revenue increase over their competitors, with projections suggesting this gap could grow to 37 percentage points by 2026 [17].

The financial benefits go beyond revenue. Reinvention strategies have been linked to a 2.9-percentage-point boost in profit margins [17]. Real-world examples highlight the potential of such approaches. Walmart’s LED retrofitting initiative across its facilities has resulted in up to $200 million in annual savings by cutting electricity costs and reducing maintenance expenses [19]. Similarly, UPS optimized its delivery routes, saving 10 million gallons of fuel, cutting 20,000 tons of CO₂ emissions, and enabling the delivery of 350,000 more packages annually - all while using 1,100 fewer trucks [19].

The decision to treat ESG as a tool for compliance or as a driver of transformation is critical and shapes how companies allocate resources and develop talent strategies [17]. Léon Wijnands, Head of Sustainability at ING Netherlands, emphasizes this point:

"To truly incorporate sustainability into your business, it must be integrated throughout. We have an integrated strategy that includes both financial and concrete ESG KPIs..." [17]

Making ESG a central part of corporate strategy rather than a compliance checkbox can yield substantial operational advantages. Research shows ESG strategies can influence corporate operating profits by as much as 60% [18]. Consumer and investor expectations also support this approach: 72% of Gen Z consumers are willing to pay extra for sustainable products, and 76% of investors trust sustainability data more when independently verified [4]. Additionally, 33% of CEOs globally report that climate-conscious investments over the past five years have directly boosted revenue [3].

By embedding ESG into strategic priorities and collaborating with experts, companies can turn insights into actionable results.

Work with Consulting Experts for Better Results

Expert consultants can help businesses extract maximum value from ESG reporting by turning sustainability goals into operational improvements. These professionals specialize in transforming ESG data into actionable strategies, leveraging tools like automated systems, real-time dashboards, and robust controls. Council Fire, for instance, works with organizations to move beyond compliance, delivering system-level results that enhance operations, supply chains, and infrastructure. Their services include climate resilience planning, stakeholder engagement, and data-driven solutions.

This expertise is especially critical when navigating complex regulatory requirements, such as California’s SB-253 and SB-261 emissions disclosure laws or the EU’s CSRD compliance standards [4].

Investing in expert guidance often leads to measurable returns. For example, StandardAero’s GreenERmro initiative used digitized environmental metrics to save $1.3 million annually, conserve 4 million gallons of water, and cut landfill waste by 75% in 2024 [19]. Similarly, Boeing’s Ergo Challenge resulted in 68 ergonomic improvement projects, reducing ergonomic risks by 93% and saving $2.6 million through avoided costs [19].

In addition to operational savings, expert validation of ESG strategies can enhance investor confidence. By combining strategic planning with precise execution, consultants help companies realize the full potential of ESG reporting - whether through cost reductions, improved market positioning, or stronger relationships with investors.

Conclusion

Successful ESG reporting hinges on a structured, repeatable process that combines meticulous data management with strategic storytelling. The first step is identifying key ESG issues through double materiality assessments, followed by choosing the right frameworks to meet stakeholder expectations - whether it's ISSB for investor-focused disclosures, GRI for broader impact reporting, or CSRD for compliance within the EU [16][2]. Establishing audit-ready data systems from the outset ensures traceability and prepares organizations for mandatory assurance requirements set to take effect in 2026 [16].

The corporate landscape is already shifting from mere compliance to leveraging ESG as a strategic advantage. For instance, the percentage of corporate boards with dedicated ESG committees surged from 41% in 2018 to nearly 75% by 2022 [20]. This trend underscores the growing recognition that effective ESG reporting requires balancing technical precision with compelling narrative.

Paul Gassett, Chief Executive Officer at OBATA, captures this dual approach perfectly:

"Effective ESG reporting requires a deliberate blend of analytical rigor and strategic communication... the science - frameworks, data, and assurance - must integrate seamlessly with the art - narrative, structure, and visual experience." [16]

Starting with audit-ready data systems not only reduces the need for rework but also builds trust with investors and regulators [16]. Early Scope 3 measurement is another critical step, allowing companies to align supply chain data and refine estimates ahead of regulatory deadlines [16].

Expert guidance can significantly streamline this process, helping organizations navigate complex regulations, select the right frameworks, and transform raw data into actionable strategies. With a structured approach, ESG reporting becomes more than a compliance task - it evolves into a valuable business asset that supports long-term profitability [16][20]. By embedding these practices, companies can meet rising ESG standards while positioning themselves for sustainable growth.

FAQs

How do we decide which ESG topics are truly material?

Determining material ESG topics requires a twofold evaluation: understanding how a company impacts society and the environment and examining how ESG factors influence the company's own performance. This "double materiality" approach looks at issues from two angles - an "inside-out" view (the company's effect on the world) and an "outside-in" view (how external ESG factors shape the company's success). Tools like the GRI Standards and IFRS Practice Statement 2 provide structured methods to identify, assess, and prioritize the issues that carry the greatest weight in decision-making and stakeholder engagement.

Which ESG framework should we report under for our stakeholders?

The right ESG framework for your organization hinges on your objectives and the needs of your stakeholders. SASB standards are tailored for industry-specific and financially relevant disclosures, making them a solid choice for businesses aiming to align with financial reporting priorities. On the other hand, GRI standards emphasize broader sustainability issues and transparency, catering to a wider range of stakeholder interests. Many organizations opt to use both frameworks together to meet diverse expectations and provide well-rounded reporting.

SASB, recognized globally and managed by the IFRS Foundation, focuses on delivering cost-effective and industry-relevant reporting. Meanwhile, GRI excels in fostering deeper engagement with stakeholders through its emphasis on transparency and sustainability.

How can we make our ESG data audit-ready and verifiable?

To make sure your ESG data holds up to audits and remains verifiable, it’s essential to build a solid internal framework. Start by implementing clear controls and assigning specific ownership for data management. Keep evidence files well-organized and traceable to back up your claims. Standardize how data is collected to ensure consistency and reliability across the board. Additionally, document your processes thoroughly so you can demonstrate their dependability when needed. Regularly revisit and update these controls to safeguard data accuracy and support external verification efforts over time.

Related Blog Posts

Latest Articles

©2025

FAQ

01

What does it really mean to “redefine profit”?

02

What makes Council Fire different?

03

Who does Council Fire you work with?

04

What does working with Council Fire actually look like?

05

How does Council Fire help organizations turn big goals into action?

06

How does Council Fire define and measure success?

Feb 23, 2026

How to Measure and Report ESG Impact Effectively for Corporations

ESG Strategy

In This Article

Clear, step-by-step guide to identify material ESG issues, choose frameworks, collect audit-ready data, verify metrics, and link ESG reporting to business value.

How to Measure and Report ESG Impact Effectively for Corporations

Measuring and reporting ESG (Environmental, Social, and Governance) impact is now a critical business requirement. Investors demand transparency, regulators enforce stricter standards, and consumers prioritize sustainability. This guide outlines a clear, step-by-step approach to help corporations navigate ESG reporting challenges, select the right frameworks, and improve data accuracy.

Key Takeaways:

Identify Material ESG Issues: Focus on what matters most to your business and stakeholders using materiality assessments, including double materiality for broader insights.

Choose the Right Framework: Options include GRI, SASB, ISSB, ESRS, and CDP, each tailored to specific audiences and goals.

Collect Accurate Data: Build systems for traceable, audit-ready ESG data, leveraging existing platforms like SAP or Oracle.

Verify and Structure Reports: Ensure data accuracy through internal controls and independent validation. Organize reports around governance, strategy, risk management, and metrics.

Align ESG with Business Goals: Use ESG reporting to identify cost savings, reduce risks, and strengthen stakeholder trust.

Why It Matters:

90% of S&P 500 companies now publish sustainability reports, up from 20% in 2011.

76% of investors trust independently verified ESG data, and 72% of Gen Z consumers are willing to pay more for sustainable products.

By following these principles, corporations can meet regulatory demands, build trust, and turn ESG efforts into measurable business value.

Step 1: Identify Material ESG Issues Through Assessments

How to Determine Material ESG Issues

Pinpointing material ESG (Environmental, Social, and Governance) issues is essential for credible and effective reporting. Materiality refers to identifying the topics that have the greatest impact on your organization’s economic, environmental, and social performance [6]. The process involves narrowing down a wide range of ESG concerns to focus only on those that are most relevant to your business and stakeholders.

Here’s how you can approach this:

Understand your organizational context: Map out your business activities, geographical footprint, and the stakeholders you interact with - both internally and externally [6].

Identify impacts: Look across your value chain to uncover both negative effects that need addressing and positive contributions you can amplify [6][8].

Assess significance: Use both quantitative and qualitative methods to evaluate the severity, likelihood, scale, and scope of these impacts [6].

Prioritize key issues: Focus on the most significant impacts for reporting purposes and integrate them into your overall strategy [6][8].

Engaging with stakeholders is a critical part of this process. Collaboration with internal teams, investors, suppliers, customers, and local communities can provide valuable insights [8]. Surveys are particularly useful, enabling stakeholders to rank ESG issues based on their perceived impact on business performance [8]. Where direct consultation isn’t feasible, input from independent experts, such as NGOs or academics, can help fill the gap [6].

"As in financial reporting, you need to provide your stakeholders with information about the topics that matter and ensure less-relevant information doesn't get in the way." – KPMG [8]

Organizations that embed sustainability into their operations often see tangible benefits. Companies with strong sustainability practices report 16% higher revenue growth and are 52% more likely to excel in profitability [8]. For private firms, sustainability can boost EBITDA by 4% to 7%, while also increasing exit multiples by up to 7% [8]. Additionally, companies that disclose materiality assessments experience a 36% rate of shareholder proposal withdrawals, compared to 29% for those that don’t - indicating better stakeholder engagement [7].

This groundwork sets the stage for applying a double-lens approach to refine and deepen the understanding of ESG impacts.

Understanding Double Materiality

Double materiality builds on traditional materiality assessments by introducing a dual perspective. It considers two lenses:

Impact Materiality: Focuses on how your company’s activities affect society and the environment - an "inside-out" view [9].

Financial Materiality: Examines how ESG factors influence your company’s financial performance, cash flow, and access to capital - an "outside-in" perspective [9].

This concept plays a central role in the EU's Corporate Sustainability Reporting Directive (CSRD) and European Sustainability Reporting Standards (ESRS) [9].

An issue may be material from one perspective but not the other. For example, Telefónica, a Spanish telecommunications company, identified greenhouse gas emissions as material from both perspectives in its 2021 assessment. However, water and wastewater management was deemed material only from an impact perspective, while risk and critical incidents management was viewed as material only from a financial standpoint [9]. This dual approach ensures that critical environmental and social issues are not overlooked, even if they don’t directly affect financial outcomes under traditional frameworks.

The adoption of double materiality is gaining momentum worldwide. In 2023, 16 out of 47 European companies explicitly used this framework in their reports [9]. Meanwhile, in the Asia-Pacific region, about 51% of companies have incorporated double materiality as part of their net-zero strategies [9].

To implement this approach, start by mapping your value chain, covering all entities you control or influence, including suppliers and partners [9][6]. Then, identify specific Impacts, Risks, and Opportunities (IROs) to evaluate over short-, medium-, and long-term horizons [9]. Finally, present your findings in a double materiality matrix, which plots issues along two axes: "Impact on People/Environment" and "Financial Influence on the Company" [9].

This structured approach ensures a comprehensive view of ESG priorities, aligning both societal and financial considerations.

How to build a modern ESG reporting framework | Understanding standards, metrics and challenges

Step 2: Select the Right ESG Reporting Framework

ESG Reporting Frameworks Comparison Guide for US Corporations

Main ESG Reporting Frameworks Explained

Once material ESG issues are identified, the next step is choosing the right reporting framework. This decision is essential for creating transparent and effective ESG reports. With various frameworks available, each designed for specific purposes and audiences, understanding their focus can help align your reporting strategy with both your business goals and stakeholder needs.

GRI (Global Reporting Initiative) emphasizes a broad stakeholder approach, addressing how a company impacts the economy, environment, and people. It’s widely adopted, with 78% of the world’s top 250 companies using it [12]. GRI is particularly effective for communicating with diverse groups, including employees, customers, NGOs, and local communities. Its modular structure combines universal standards with sector-specific guidance tailored to different industries [1][12].

SASB (Sustainability Accounting Standards Board) zeroes in on financial materiality, offering industry-specific metrics across 77 sectors. Over 3,200 companies across more than 80 jurisdictions, including 75% of the S&P Global 1200 Index, use SASB Standards [10]. This framework highlights ESG topics most likely to influence financial performance and shareholder value. Now overseen by the IFRS Foundation, SASB Standards are designed for investor disclosures and are freely accessible.

ISSB (International Sustainability Standards Board) is emerging as a global baseline for sustainability reporting. It integrates SASB and TCFD into two unified standards: IFRS S1 (General Requirements for Disclosure of Sustainability-related Financial Information) and IFRS S2 (Climate-related Disclosures) [10][11]. Targeting investors, ISSB provides consistent and comparable disclosures.

"As the regulatory agenda intensifies, companies that can pivot quickly and approach ESG reporting strategically will be able to move from simple compliance to creating a clear competitive advantage for their organizations" [11].

Stephanie Jamison, Jens Laue, and Michela Coppola, Accenture

TCFD (Task Force on Climate-related Financial Disclosures), which ceased operations in October 2023, has its recommendations embedded within IFRS S2 [11][13]. TCFD focused on climate-related financial risks and opportunities through four pillars: Governance, Strategy, Risk Management, and Metrics and Targets. Today, its principles are foundational to climate reporting under IFRS S2.

ESRS (European Sustainability Reporting Standards), developed under the EU’s Corporate Sustainability Reporting Directive (CSRD), is mandatory for large companies operating in the European Union, including U.S. corporations with significant EU subsidiaries [11][3]. ESRS requires "double materiality" reporting, assessing both how sustainability issues affect the business and how the business impacts society and the environment. Proposed amendments in July 2025 aim to reduce reporting burdens by cutting mandatory data points by 57% [11].

CDP (formerly Carbon Disclosure Project) focuses on environmental data, including carbon emissions, water, and forests. In 2024, nearly 25,000 companies globally, including over 5,500 in North America, utilized the CDP system [11]. CDP works well as a complementary tool for investors and customers seeking detailed environmental performance data.

Choosing the right framework hinges on three key factors: your primary audience (investors versus a broader group of stakeholders), your industry's specific risks and opportunities, and regulatory requirements. Many U.S. companies adopt a blended approach - using SASB or ISSB for investor-focused reporting while maintaining GRI disclosures for broad stakeholder engagement. This dual strategy aligns with trends like the 59% of individual investors in early 2025 who planned to increase sustainable investments within 12 months [11].

Framework Comparison Table

Here’s a quick comparison of major frameworks to guide U.S.-based corporations in their selection:

| Framework | Primary Focus | Target Audience | Materiality Type | Applicability for U.S. Corps | Key Reason for Use |

| --- | --- | --- | --- | --- | --- |

| <strong>GRI</strong> | Impact on economy, environment, and people | Multi-stakeholder (employees, customers, NGOs) | Impact/Double Materiality | High (Voluntary) | Widely used for broad stakeholder communication |

| <strong>SASB</strong> | Industry-specific financial risks and opportunities | Investors and providers of capital | Financial Materiality | High (Voluntary) | Preferred by U.S. investors for industry-specific metrics |

| <strong>ISSB (IFRS S1/S2)</strong> | Global baseline for sustainability-related financial disclosures | Investors and capital markets | Financial Materiality | High (Voluntary) | Emerging standard for global capital markets |

| <strong>TCFD</strong> | Climate-related financial risks and opportunities | Investors, lenders, and insurers | Financial Materiality | High (Voluntary) | Now part of IFRS S2; essential for climate-related reporting |

| <strong>ESRS (EU)</strong> | Mandatory EU sustainability reporting | Regulators and EU stakeholders | Double Materiality | Mandatory (Conditional) | Required for U.S. firms with significant EU subsidiaries |

| <strong>CDP</strong> | Environmental data (carbon, water, forests) | Investors and environmental stakeholders | Financial Materiality | High (Voluntary) | Standard for carbon and water data reporting

Starting with a materiality assessment helps map stakeholder needs and determine the best framework. For investor-focused goals, SASB or ISSB offer industry-specific, globally comparable insights. Companies with diverse stakeholder groups or EU operations may find GRI or ESRS more suitable. Many organizations also leverage tools like CDP and GRI to identify overlapping data points, streamlining their reporting process. This interoperability reduces duplication, allowing data to serve multiple frameworks efficiently.

Step 3: Collect and Measure ESG Data

Set Up Data Collection Systems

Creating an effective ESG data system starts with building a detailed inventory of all data sources. This inventory should outline the specific data needed, where it currently resides, how it will be utilized, and its long-term storage plan [5]. Without this step, you risk overlooking important information or duplicating efforts across teams.

Assign clear accountability roles to maintain data quality throughout the process. Designate an ESG Controller to lead operations, supported by three key roles: Information Owners, who ensure accuracy at the source; Disclosure Owners, who certify data before it enters reports; and independent Validators, who provide an objective review [5]. This structured approach ensures that every stage of data collection is managed responsibly.

Rather than creating a standalone ESG reporting system, integrate these processes into your existing enterprise platforms. Systems like Oracle, SAP, or Workday, commonly used for financial reporting, can also handle ESG data [5][15]. For frequently updated metrics - like energy usage or business travel - establish API connections to automatically pull data from utility providers or travel management systems [15]. Automation not only reduces manual tracking but also minimizes errors.

To ensure accuracy, trace every metric from its original source through all transformations to its final report format. This process helps pinpoint where controls are needed and uncovers any data gaps. Conduct a data gap analysis early in the reporting cycle to address issues before deadlines become a concern. This proactive approach allows time for data cleansing and remediation.

With a solid framework for data collection in place, the next critical step is to verify the accuracy of your ESG data.

Verify Data Accuracy

Verification is essential for ensuring the integrity of your ESG disclosures. Start by conducting quality assessments (QA) to check for accuracy, completeness, and reliable calculations before data is transferred to the final reporting system [5]. These assessments help catch errors early, reducing risks to your report’s credibility and preparing the data for independent attestation - a level of assurance that 85% of investors now expect, akin to financial audits [5].

Ensure internal controls are in place by aligning the data and assumptions used for ESG disclosures with those in your financial statements [14]. This consistency is crucial, as both regulators and auditors will compare your sustainability metrics with your financial filings. As noted in the IFRS S1 standard:

"For sustainability-related financial information to be useful, it must be relevant and faithfully represent what it purports to represent" [14].

Independent reviewers should be able to confirm that your data accurately supports your claims.

To meet regulatory and investor expectations, maintain ESG data in compliance with company policies and ensure it is "investor-grade" [5]. This involves documenting data sources, using transparent calculation methods, and maintaining traceable audit trails. With 76% of investors expressing greater confidence in sustainability information that has been independently assured [4], third-party verification is becoming a crucial step. Organize and store all supporting documentation systematically to facilitate efficient audits.

The table below outlines the key steps for verifying ESG data:

| Verification Step | Description | Key Objective |

| --- | --- | --- |

| Data Source Inventory | Catalog all origins of ESG-related data | Ensure completeness and identify gaps |

| Metric Walkthrough | Trace data from source to final report | Verify accuracy and internal controls |

| Quality Assessment (QA) | Test calculations and cleanse data | Ensure reliability of metrics |

| Independent Validation | Review by an external, unbiased party | Enhance credibility and prepare for audit |

| External Attestation | Third-party audit (limited or reasonable assurance) | Build stakeholder trust

Step 4: Structure Your ESG Report

Core Sections of an ESG Report

Once you've gathered comprehensive ESG data, the next step is organizing your report effectively. A well-structured ESG report typically revolves around four key pillars - Governance, Strategy, Risk Management, and Metrics and Targets - aligned with TCFD and ISSB guidelines [14].

Governance: This section highlights the individuals or committees responsible for overseeing ESG efforts. Detail their roles, responsibilities, and how they stay informed on sustainability matters. Additionally, outline how ESG performance metrics are tied to executive compensation.

Strategy: Explain how ESG-related risks and opportunities influence your business model, value chain, and financial planning. Include an analysis of your organization's ability to adapt to these challenges.

Risk Management: Describe the processes for identifying, monitoring, and mitigating ESG risks. This should also include scenario analyses to demonstrate preparedness for potential challenges.

Metrics and Targets: Share the performance indicators you track and provide updates on progress toward your ESG goals. Ensure that ESG disclosures align with the same reporting entity and currency as your financial statements to maintain consistency and comparability [14].

For businesses operating within or serving the European Union, it’s essential to address double materiality. This means reporting on both the financial risks arising from ESG issues and the organization's broader impact on the environment and society [4].

Once your report framework is established, incorporate stakeholder feedback to refine and enhance your disclosures.

Include Stakeholder Input

Identifying and engaging with key stakeholders - such as investors, employees, customers, suppliers, regulators, and civil society - is critical [16][2]. Conduct double materiality assessments to ensure the report addresses topics that are both significant for business performance and important to stakeholders. Aligning these insights with your strategic objectives enhances the report's relevance and effectiveness.

Engage internal experts and leadership to validate technical data and ensure ESG priorities align with your broader business strategy [16]. As Paul Gassett, CEO of OBATA, notes:

"Effective ESG reporting requires a deliberate blend of analytical rigor and strategic communication. High-quality sustainability reports strengthen stakeholder confidence, reduce information asymmetry, and support more effective engagement with investors and regulators." [16]

Keep stakeholders informed on a regular basis - quarterly or semiannually - using accessible formats like landing pages, infographics, or short videos to maintain engagement and transparency [16].

Step 5: Use ESG Reporting to Create Business Value

Connect ESG Reporting to Business Goals

Tying ESG reporting to business objectives can unlock measurable financial gains and position companies for long-term success. Companies that integrate ESG into their core strategies and continuously adapt - referred to as "Reinventors" - have shown remarkable financial performance. Between 2019 and 2022, these companies achieved a 15-percentage-point revenue increase over their competitors, with projections suggesting this gap could grow to 37 percentage points by 2026 [17].

The financial benefits go beyond revenue. Reinvention strategies have been linked to a 2.9-percentage-point boost in profit margins [17]. Real-world examples highlight the potential of such approaches. Walmart’s LED retrofitting initiative across its facilities has resulted in up to $200 million in annual savings by cutting electricity costs and reducing maintenance expenses [19]. Similarly, UPS optimized its delivery routes, saving 10 million gallons of fuel, cutting 20,000 tons of CO₂ emissions, and enabling the delivery of 350,000 more packages annually - all while using 1,100 fewer trucks [19].

The decision to treat ESG as a tool for compliance or as a driver of transformation is critical and shapes how companies allocate resources and develop talent strategies [17]. Léon Wijnands, Head of Sustainability at ING Netherlands, emphasizes this point:

"To truly incorporate sustainability into your business, it must be integrated throughout. We have an integrated strategy that includes both financial and concrete ESG KPIs..." [17]

Making ESG a central part of corporate strategy rather than a compliance checkbox can yield substantial operational advantages. Research shows ESG strategies can influence corporate operating profits by as much as 60% [18]. Consumer and investor expectations also support this approach: 72% of Gen Z consumers are willing to pay extra for sustainable products, and 76% of investors trust sustainability data more when independently verified [4]. Additionally, 33% of CEOs globally report that climate-conscious investments over the past five years have directly boosted revenue [3].

By embedding ESG into strategic priorities and collaborating with experts, companies can turn insights into actionable results.

Work with Consulting Experts for Better Results

Expert consultants can help businesses extract maximum value from ESG reporting by turning sustainability goals into operational improvements. These professionals specialize in transforming ESG data into actionable strategies, leveraging tools like automated systems, real-time dashboards, and robust controls. Council Fire, for instance, works with organizations to move beyond compliance, delivering system-level results that enhance operations, supply chains, and infrastructure. Their services include climate resilience planning, stakeholder engagement, and data-driven solutions.

This expertise is especially critical when navigating complex regulatory requirements, such as California’s SB-253 and SB-261 emissions disclosure laws or the EU’s CSRD compliance standards [4].

Investing in expert guidance often leads to measurable returns. For example, StandardAero’s GreenERmro initiative used digitized environmental metrics to save $1.3 million annually, conserve 4 million gallons of water, and cut landfill waste by 75% in 2024 [19]. Similarly, Boeing’s Ergo Challenge resulted in 68 ergonomic improvement projects, reducing ergonomic risks by 93% and saving $2.6 million through avoided costs [19].

In addition to operational savings, expert validation of ESG strategies can enhance investor confidence. By combining strategic planning with precise execution, consultants help companies realize the full potential of ESG reporting - whether through cost reductions, improved market positioning, or stronger relationships with investors.

Conclusion

Successful ESG reporting hinges on a structured, repeatable process that combines meticulous data management with strategic storytelling. The first step is identifying key ESG issues through double materiality assessments, followed by choosing the right frameworks to meet stakeholder expectations - whether it's ISSB for investor-focused disclosures, GRI for broader impact reporting, or CSRD for compliance within the EU [16][2]. Establishing audit-ready data systems from the outset ensures traceability and prepares organizations for mandatory assurance requirements set to take effect in 2026 [16].

The corporate landscape is already shifting from mere compliance to leveraging ESG as a strategic advantage. For instance, the percentage of corporate boards with dedicated ESG committees surged from 41% in 2018 to nearly 75% by 2022 [20]. This trend underscores the growing recognition that effective ESG reporting requires balancing technical precision with compelling narrative.

Paul Gassett, Chief Executive Officer at OBATA, captures this dual approach perfectly:

"Effective ESG reporting requires a deliberate blend of analytical rigor and strategic communication... the science - frameworks, data, and assurance - must integrate seamlessly with the art - narrative, structure, and visual experience." [16]

Starting with audit-ready data systems not only reduces the need for rework but also builds trust with investors and regulators [16]. Early Scope 3 measurement is another critical step, allowing companies to align supply chain data and refine estimates ahead of regulatory deadlines [16].

Expert guidance can significantly streamline this process, helping organizations navigate complex regulations, select the right frameworks, and transform raw data into actionable strategies. With a structured approach, ESG reporting becomes more than a compliance task - it evolves into a valuable business asset that supports long-term profitability [16][20]. By embedding these practices, companies can meet rising ESG standards while positioning themselves for sustainable growth.

FAQs

How do we decide which ESG topics are truly material?

Determining material ESG topics requires a twofold evaluation: understanding how a company impacts society and the environment and examining how ESG factors influence the company's own performance. This "double materiality" approach looks at issues from two angles - an "inside-out" view (the company's effect on the world) and an "outside-in" view (how external ESG factors shape the company's success). Tools like the GRI Standards and IFRS Practice Statement 2 provide structured methods to identify, assess, and prioritize the issues that carry the greatest weight in decision-making and stakeholder engagement.

Which ESG framework should we report under for our stakeholders?

The right ESG framework for your organization hinges on your objectives and the needs of your stakeholders. SASB standards are tailored for industry-specific and financially relevant disclosures, making them a solid choice for businesses aiming to align with financial reporting priorities. On the other hand, GRI standards emphasize broader sustainability issues and transparency, catering to a wider range of stakeholder interests. Many organizations opt to use both frameworks together to meet diverse expectations and provide well-rounded reporting.

SASB, recognized globally and managed by the IFRS Foundation, focuses on delivering cost-effective and industry-relevant reporting. Meanwhile, GRI excels in fostering deeper engagement with stakeholders through its emphasis on transparency and sustainability.

How can we make our ESG data audit-ready and verifiable?

To make sure your ESG data holds up to audits and remains verifiable, it’s essential to build a solid internal framework. Start by implementing clear controls and assigning specific ownership for data management. Keep evidence files well-organized and traceable to back up your claims. Standardize how data is collected to ensure consistency and reliability across the board. Additionally, document your processes thoroughly so you can demonstrate their dependability when needed. Regularly revisit and update these controls to safeguard data accuracy and support external verification efforts over time.

Related Blog Posts

FAQ

01

What does it really mean to “redefine profit”?

02

What makes Council Fire different?

03

Who does Council Fire you work with?

04

What does working with Council Fire actually look like?

05

How does Council Fire help organizations turn big goals into action?

06

How does Council Fire define and measure success?

Feb 23, 2026

How to Measure and Report ESG Impact Effectively for Corporations

ESG Strategy

In This Article

Clear, step-by-step guide to identify material ESG issues, choose frameworks, collect audit-ready data, verify metrics, and link ESG reporting to business value.

How to Measure and Report ESG Impact Effectively for Corporations

Measuring and reporting ESG (Environmental, Social, and Governance) impact is now a critical business requirement. Investors demand transparency, regulators enforce stricter standards, and consumers prioritize sustainability. This guide outlines a clear, step-by-step approach to help corporations navigate ESG reporting challenges, select the right frameworks, and improve data accuracy.

Key Takeaways:

Identify Material ESG Issues: Focus on what matters most to your business and stakeholders using materiality assessments, including double materiality for broader insights.

Choose the Right Framework: Options include GRI, SASB, ISSB, ESRS, and CDP, each tailored to specific audiences and goals.

Collect Accurate Data: Build systems for traceable, audit-ready ESG data, leveraging existing platforms like SAP or Oracle.

Verify and Structure Reports: Ensure data accuracy through internal controls and independent validation. Organize reports around governance, strategy, risk management, and metrics.

Align ESG with Business Goals: Use ESG reporting to identify cost savings, reduce risks, and strengthen stakeholder trust.

Why It Matters:

90% of S&P 500 companies now publish sustainability reports, up from 20% in 2011.

76% of investors trust independently verified ESG data, and 72% of Gen Z consumers are willing to pay more for sustainable products.

By following these principles, corporations can meet regulatory demands, build trust, and turn ESG efforts into measurable business value.

Step 1: Identify Material ESG Issues Through Assessments

How to Determine Material ESG Issues

Pinpointing material ESG (Environmental, Social, and Governance) issues is essential for credible and effective reporting. Materiality refers to identifying the topics that have the greatest impact on your organization’s economic, environmental, and social performance [6]. The process involves narrowing down a wide range of ESG concerns to focus only on those that are most relevant to your business and stakeholders.

Here’s how you can approach this:

Understand your organizational context: Map out your business activities, geographical footprint, and the stakeholders you interact with - both internally and externally [6].

Identify impacts: Look across your value chain to uncover both negative effects that need addressing and positive contributions you can amplify [6][8].

Assess significance: Use both quantitative and qualitative methods to evaluate the severity, likelihood, scale, and scope of these impacts [6].

Prioritize key issues: Focus on the most significant impacts for reporting purposes and integrate them into your overall strategy [6][8].

Engaging with stakeholders is a critical part of this process. Collaboration with internal teams, investors, suppliers, customers, and local communities can provide valuable insights [8]. Surveys are particularly useful, enabling stakeholders to rank ESG issues based on their perceived impact on business performance [8]. Where direct consultation isn’t feasible, input from independent experts, such as NGOs or academics, can help fill the gap [6].

"As in financial reporting, you need to provide your stakeholders with information about the topics that matter and ensure less-relevant information doesn't get in the way." – KPMG [8]

Organizations that embed sustainability into their operations often see tangible benefits. Companies with strong sustainability practices report 16% higher revenue growth and are 52% more likely to excel in profitability [8]. For private firms, sustainability can boost EBITDA by 4% to 7%, while also increasing exit multiples by up to 7% [8]. Additionally, companies that disclose materiality assessments experience a 36% rate of shareholder proposal withdrawals, compared to 29% for those that don’t - indicating better stakeholder engagement [7].

This groundwork sets the stage for applying a double-lens approach to refine and deepen the understanding of ESG impacts.

Understanding Double Materiality

Double materiality builds on traditional materiality assessments by introducing a dual perspective. It considers two lenses:

Impact Materiality: Focuses on how your company’s activities affect society and the environment - an "inside-out" view [9].

Financial Materiality: Examines how ESG factors influence your company’s financial performance, cash flow, and access to capital - an "outside-in" perspective [9].

This concept plays a central role in the EU's Corporate Sustainability Reporting Directive (CSRD) and European Sustainability Reporting Standards (ESRS) [9].

An issue may be material from one perspective but not the other. For example, Telefónica, a Spanish telecommunications company, identified greenhouse gas emissions as material from both perspectives in its 2021 assessment. However, water and wastewater management was deemed material only from an impact perspective, while risk and critical incidents management was viewed as material only from a financial standpoint [9]. This dual approach ensures that critical environmental and social issues are not overlooked, even if they don’t directly affect financial outcomes under traditional frameworks.

The adoption of double materiality is gaining momentum worldwide. In 2023, 16 out of 47 European companies explicitly used this framework in their reports [9]. Meanwhile, in the Asia-Pacific region, about 51% of companies have incorporated double materiality as part of their net-zero strategies [9].

To implement this approach, start by mapping your value chain, covering all entities you control or influence, including suppliers and partners [9][6]. Then, identify specific Impacts, Risks, and Opportunities (IROs) to evaluate over short-, medium-, and long-term horizons [9]. Finally, present your findings in a double materiality matrix, which plots issues along two axes: "Impact on People/Environment" and "Financial Influence on the Company" [9].

This structured approach ensures a comprehensive view of ESG priorities, aligning both societal and financial considerations.

How to build a modern ESG reporting framework | Understanding standards, metrics and challenges

Step 2: Select the Right ESG Reporting Framework

ESG Reporting Frameworks Comparison Guide for US Corporations

Main ESG Reporting Frameworks Explained

Once material ESG issues are identified, the next step is choosing the right reporting framework. This decision is essential for creating transparent and effective ESG reports. With various frameworks available, each designed for specific purposes and audiences, understanding their focus can help align your reporting strategy with both your business goals and stakeholder needs.

GRI (Global Reporting Initiative) emphasizes a broad stakeholder approach, addressing how a company impacts the economy, environment, and people. It’s widely adopted, with 78% of the world’s top 250 companies using it [12]. GRI is particularly effective for communicating with diverse groups, including employees, customers, NGOs, and local communities. Its modular structure combines universal standards with sector-specific guidance tailored to different industries [1][12].

SASB (Sustainability Accounting Standards Board) zeroes in on financial materiality, offering industry-specific metrics across 77 sectors. Over 3,200 companies across more than 80 jurisdictions, including 75% of the S&P Global 1200 Index, use SASB Standards [10]. This framework highlights ESG topics most likely to influence financial performance and shareholder value. Now overseen by the IFRS Foundation, SASB Standards are designed for investor disclosures and are freely accessible.

ISSB (International Sustainability Standards Board) is emerging as a global baseline for sustainability reporting. It integrates SASB and TCFD into two unified standards: IFRS S1 (General Requirements for Disclosure of Sustainability-related Financial Information) and IFRS S2 (Climate-related Disclosures) [10][11]. Targeting investors, ISSB provides consistent and comparable disclosures.

"As the regulatory agenda intensifies, companies that can pivot quickly and approach ESG reporting strategically will be able to move from simple compliance to creating a clear competitive advantage for their organizations" [11].

Stephanie Jamison, Jens Laue, and Michela Coppola, Accenture

TCFD (Task Force on Climate-related Financial Disclosures), which ceased operations in October 2023, has its recommendations embedded within IFRS S2 [11][13]. TCFD focused on climate-related financial risks and opportunities through four pillars: Governance, Strategy, Risk Management, and Metrics and Targets. Today, its principles are foundational to climate reporting under IFRS S2.

ESRS (European Sustainability Reporting Standards), developed under the EU’s Corporate Sustainability Reporting Directive (CSRD), is mandatory for large companies operating in the European Union, including U.S. corporations with significant EU subsidiaries [11][3]. ESRS requires "double materiality" reporting, assessing both how sustainability issues affect the business and how the business impacts society and the environment. Proposed amendments in July 2025 aim to reduce reporting burdens by cutting mandatory data points by 57% [11].

CDP (formerly Carbon Disclosure Project) focuses on environmental data, including carbon emissions, water, and forests. In 2024, nearly 25,000 companies globally, including over 5,500 in North America, utilized the CDP system [11]. CDP works well as a complementary tool for investors and customers seeking detailed environmental performance data.

Choosing the right framework hinges on three key factors: your primary audience (investors versus a broader group of stakeholders), your industry's specific risks and opportunities, and regulatory requirements. Many U.S. companies adopt a blended approach - using SASB or ISSB for investor-focused reporting while maintaining GRI disclosures for broad stakeholder engagement. This dual strategy aligns with trends like the 59% of individual investors in early 2025 who planned to increase sustainable investments within 12 months [11].

Framework Comparison Table

Here’s a quick comparison of major frameworks to guide U.S.-based corporations in their selection:

| Framework | Primary Focus | Target Audience | Materiality Type | Applicability for U.S. Corps | Key Reason for Use |

| --- | --- | --- | --- | --- | --- |

| <strong>GRI</strong> | Impact on economy, environment, and people | Multi-stakeholder (employees, customers, NGOs) | Impact/Double Materiality | High (Voluntary) | Widely used for broad stakeholder communication |

| <strong>SASB</strong> | Industry-specific financial risks and opportunities | Investors and providers of capital | Financial Materiality | High (Voluntary) | Preferred by U.S. investors for industry-specific metrics |

| <strong>ISSB (IFRS S1/S2)</strong> | Global baseline for sustainability-related financial disclosures | Investors and capital markets | Financial Materiality | High (Voluntary) | Emerging standard for global capital markets |

| <strong>TCFD</strong> | Climate-related financial risks and opportunities | Investors, lenders, and insurers | Financial Materiality | High (Voluntary) | Now part of IFRS S2; essential for climate-related reporting |

| <strong>ESRS (EU)</strong> | Mandatory EU sustainability reporting | Regulators and EU stakeholders | Double Materiality | Mandatory (Conditional) | Required for U.S. firms with significant EU subsidiaries |

| <strong>CDP</strong> | Environmental data (carbon, water, forests) | Investors and environmental stakeholders | Financial Materiality | High (Voluntary) | Standard for carbon and water data reporting

Starting with a materiality assessment helps map stakeholder needs and determine the best framework. For investor-focused goals, SASB or ISSB offer industry-specific, globally comparable insights. Companies with diverse stakeholder groups or EU operations may find GRI or ESRS more suitable. Many organizations also leverage tools like CDP and GRI to identify overlapping data points, streamlining their reporting process. This interoperability reduces duplication, allowing data to serve multiple frameworks efficiently.

Step 3: Collect and Measure ESG Data

Set Up Data Collection Systems

Creating an effective ESG data system starts with building a detailed inventory of all data sources. This inventory should outline the specific data needed, where it currently resides, how it will be utilized, and its long-term storage plan [5]. Without this step, you risk overlooking important information or duplicating efforts across teams.

Assign clear accountability roles to maintain data quality throughout the process. Designate an ESG Controller to lead operations, supported by three key roles: Information Owners, who ensure accuracy at the source; Disclosure Owners, who certify data before it enters reports; and independent Validators, who provide an objective review [5]. This structured approach ensures that every stage of data collection is managed responsibly.

Rather than creating a standalone ESG reporting system, integrate these processes into your existing enterprise platforms. Systems like Oracle, SAP, or Workday, commonly used for financial reporting, can also handle ESG data [5][15]. For frequently updated metrics - like energy usage or business travel - establish API connections to automatically pull data from utility providers or travel management systems [15]. Automation not only reduces manual tracking but also minimizes errors.

To ensure accuracy, trace every metric from its original source through all transformations to its final report format. This process helps pinpoint where controls are needed and uncovers any data gaps. Conduct a data gap analysis early in the reporting cycle to address issues before deadlines become a concern. This proactive approach allows time for data cleansing and remediation.

With a solid framework for data collection in place, the next critical step is to verify the accuracy of your ESG data.

Verify Data Accuracy

Verification is essential for ensuring the integrity of your ESG disclosures. Start by conducting quality assessments (QA) to check for accuracy, completeness, and reliable calculations before data is transferred to the final reporting system [5]. These assessments help catch errors early, reducing risks to your report’s credibility and preparing the data for independent attestation - a level of assurance that 85% of investors now expect, akin to financial audits [5].

Ensure internal controls are in place by aligning the data and assumptions used for ESG disclosures with those in your financial statements [14]. This consistency is crucial, as both regulators and auditors will compare your sustainability metrics with your financial filings. As noted in the IFRS S1 standard:

"For sustainability-related financial information to be useful, it must be relevant and faithfully represent what it purports to represent" [14].

Independent reviewers should be able to confirm that your data accurately supports your claims.

To meet regulatory and investor expectations, maintain ESG data in compliance with company policies and ensure it is "investor-grade" [5]. This involves documenting data sources, using transparent calculation methods, and maintaining traceable audit trails. With 76% of investors expressing greater confidence in sustainability information that has been independently assured [4], third-party verification is becoming a crucial step. Organize and store all supporting documentation systematically to facilitate efficient audits.

The table below outlines the key steps for verifying ESG data:

| Verification Step | Description | Key Objective |

| --- | --- | --- |

| Data Source Inventory | Catalog all origins of ESG-related data | Ensure completeness and identify gaps |

| Metric Walkthrough | Trace data from source to final report | Verify accuracy and internal controls |

| Quality Assessment (QA) | Test calculations and cleanse data | Ensure reliability of metrics |

| Independent Validation | Review by an external, unbiased party | Enhance credibility and prepare for audit |

| External Attestation | Third-party audit (limited or reasonable assurance) | Build stakeholder trust

Step 4: Structure Your ESG Report

Core Sections of an ESG Report

Once you've gathered comprehensive ESG data, the next step is organizing your report effectively. A well-structured ESG report typically revolves around four key pillars - Governance, Strategy, Risk Management, and Metrics and Targets - aligned with TCFD and ISSB guidelines [14].

Governance: This section highlights the individuals or committees responsible for overseeing ESG efforts. Detail their roles, responsibilities, and how they stay informed on sustainability matters. Additionally, outline how ESG performance metrics are tied to executive compensation.

Strategy: Explain how ESG-related risks and opportunities influence your business model, value chain, and financial planning. Include an analysis of your organization's ability to adapt to these challenges.

Risk Management: Describe the processes for identifying, monitoring, and mitigating ESG risks. This should also include scenario analyses to demonstrate preparedness for potential challenges.

Metrics and Targets: Share the performance indicators you track and provide updates on progress toward your ESG goals. Ensure that ESG disclosures align with the same reporting entity and currency as your financial statements to maintain consistency and comparability [14].

For businesses operating within or serving the European Union, it’s essential to address double materiality. This means reporting on both the financial risks arising from ESG issues and the organization's broader impact on the environment and society [4].

Once your report framework is established, incorporate stakeholder feedback to refine and enhance your disclosures.

Include Stakeholder Input

Identifying and engaging with key stakeholders - such as investors, employees, customers, suppliers, regulators, and civil society - is critical [16][2]. Conduct double materiality assessments to ensure the report addresses topics that are both significant for business performance and important to stakeholders. Aligning these insights with your strategic objectives enhances the report's relevance and effectiveness.

Engage internal experts and leadership to validate technical data and ensure ESG priorities align with your broader business strategy [16]. As Paul Gassett, CEO of OBATA, notes:

"Effective ESG reporting requires a deliberate blend of analytical rigor and strategic communication. High-quality sustainability reports strengthen stakeholder confidence, reduce information asymmetry, and support more effective engagement with investors and regulators." [16]

Keep stakeholders informed on a regular basis - quarterly or semiannually - using accessible formats like landing pages, infographics, or short videos to maintain engagement and transparency [16].

Step 5: Use ESG Reporting to Create Business Value

Connect ESG Reporting to Business Goals