Dec 29, 2025

Global ESG Standards: Climate Risk Alignment

ESG Strategy

In This Article

How TCFD, ISSB and CSRD turn climate risk into governance, disclosure and Paris-aligned transition plans for companies.

Global ESG Standards: Climate Risk Alignment

Climate risk is reshaping the corporate world, demanding action and transparency. With 2024 recorded as the hottest year in history, businesses face mounting challenges from extreme weather events, rising costs, and regulatory changes. This article outlines how global ESG standards like TCFD, ISSB, and CSRD are transforming climate risk into actionable strategies for companies.

Key Takeaways:

Climate Risk Types: Physical risks (e.g., hurricanes, wildfires) and transition risks (e.g., carbon pricing, regulations).

Major ESG Frameworks:

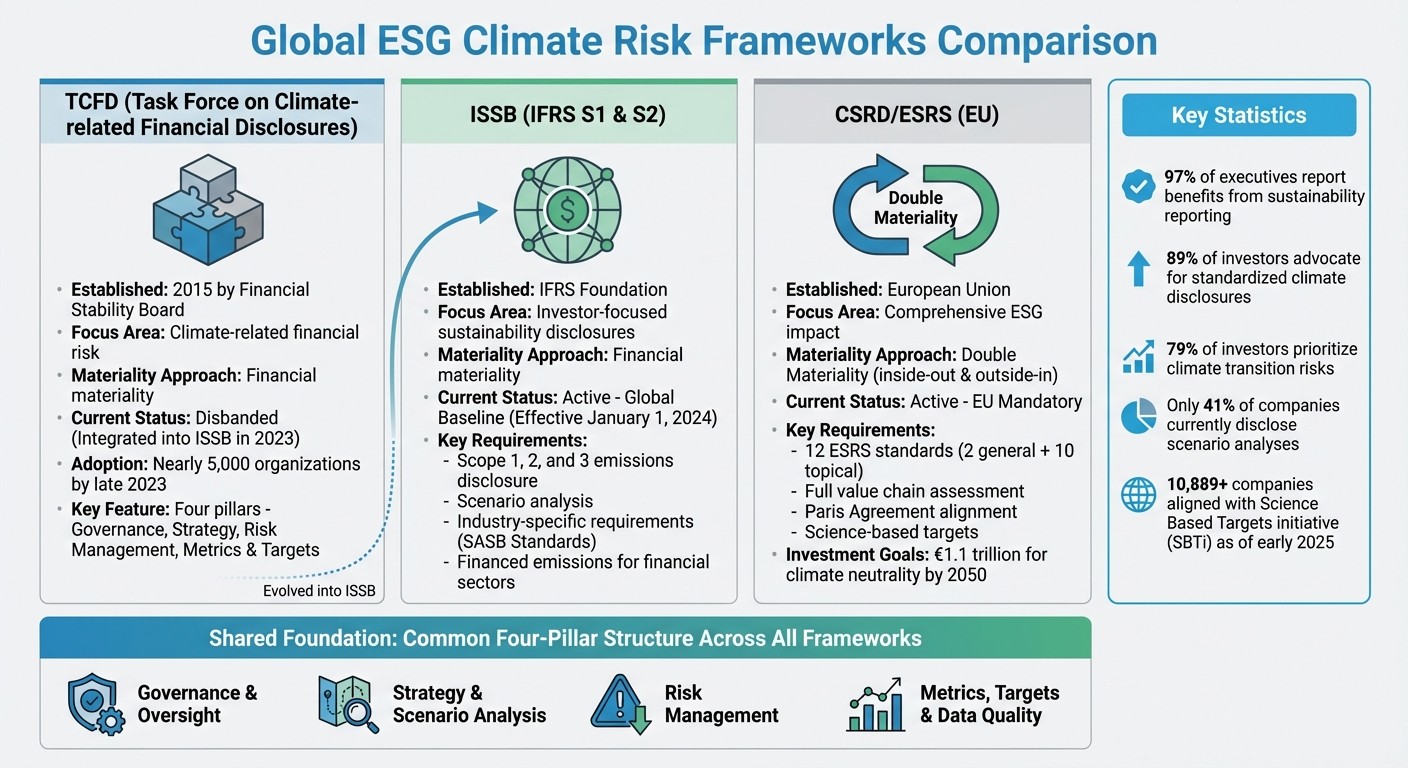

TCFD: Focused on financial materiality, now integrated into ISSB.

ISSB (IFRS S1/S2): Global baseline for sustainability reporting, emphasizing financial impacts and Scope 1, 2, and 3 emissions.

CSRD (EU): Double materiality approach, examining climate impact on companies and vice versa.

Regulatory Updates:SEC finalized climate disclosure rules in March 2024, and California laws (SB 253, SB 261) enforce stricter reporting.

Business Impact: ESG compliance influences investor trust, operational planning, and stakeholder relationships. 97% of executives report benefits from sustainability consulting and reporting.

Comparison of ESG Frameworks:

| Framework | Focus Area | Materiality Approach | Status |

| --- | --- | --- | --- |

| TCFD | Financial climate risk | Financial | Integrated into ISSB |

| ISSB | Investor-focused disclosures | Financial | Active (Global Baseline) |

| CSRD | Broader ESG impact | Double Materiality | Active (EU Mandatory)

| Framework | Focus Area | Materiality Approach | Status |

| --- | --- | --- | --- |

| TCFD | Financial climate risk | Financial | Integrated into ISSB |

| ISSB | Investor-focused disclosures | Financial | Active (Global Baseline) |

| CSRD | Broader ESG impact | Double Materiality | Active (EU Mandatory)

This guide explores how these frameworks help businesses manage climate risks, align with global goals, and prepare for a low-carbon future.

Comparison of Global ESG Climate Risk Frameworks: TCFD, ISSB, and CSRD

Beyond compliance: Leveraging climate risk for a competitive edge

Key Global ESG Standards for Climate Risk

Three major frameworks shape how companies worldwide address climate risk disclosure. While they share a common four-pillar structure, each framework introduces distinct requirements and regional nuances. Together, they guide organizations through shifting regulations and help align their climate strategies with broader global expectations.

Task Force on Climate-related Financial Disclosures (TCFD)

The TCFD laid the groundwork for modern climate disclosure frameworks, elevating climate risk from a purely environmental issue to a financial priority. Established by the Financial Stability Board in 2015, it structured climate reporting around four key pillars: Governance, Strategy, Risk Management, and Metrics and Targets [3].

By late 2023, nearly 5,000 organizations had adopted TCFD recommendations [6]. Stuart Gulliver, Chief Executive of HSBC, emphasized the framework's value:

"These recommendations are a practical and pragmatic response to the need for consistent and comparable climate-related financial disclosure" [6].

Before TCFD's widespread adoption, research by HSBC found that fewer than 25% of companies disclosed their environmental impact [6]. Following its 2023 status report, the TCFD concluded its mission and disbanded, passing its legacy to the IFRS Foundation. The foundation, through the International Sustainability Standards Board (ISSB), now oversees and refines climate-related disclosure standards [3][6].

IFRS Sustainability Disclosure Standards (ISSB: IFRS S1 and S2)

Building on TCFD's foundation, the ISSB establishes a mandatory global baseline for sustainability reporting. IFRS S2, effective for annual reporting periods starting January 1, 2024, introduces greater detail and precision to climate risk disclosures [9][12].

A key focus of IFRS S2 is financial materiality, requiring companies to report information that could influence cash flows, financing, or capital costs [7][11]. Companies must disclose absolute gross Scope 1, Scope 2, and Scope 3 greenhouse gas emissions, using the Greenhouse Gas Protocol: A Corporate Accounting and Reporting Standard [8][5]. They are also tasked with conducting scenario analyses and providing detailed transition plans [7][5].

In December 2025, the ISSB implemented amendments to simplify greenhouse gas emissions disclosures [9]. The framework also incorporates industry-specific requirements based on SASB Standards, adding sector-specific depth [9][10]. According to the IFRS Foundation:

"IFRS S2 integrates and builds on the recommendations of the Task Force on Climate-related Financial Disclosures (TCFD) and incorporates industry-based disclosure requirements derived from SASB Standards" [9].

For industries like asset management, commercial banking, and insurance, IFRS S2 mandates disclosures on financed emissions tied to investments [8][5]. While ISSB focuses on investor needs, the EU's CSRD takes a broader approach by incorporating double materiality.

EU Corporate Sustainability Reporting Directive (CSRD) and ESRS

The CSRD applies a double materiality perspective, requiring companies to report both on how climate change impacts their financial performance (outside-in) and how their operations affect the environment and society (inside-out) [13].

The European Sustainability Reporting Standards (ESRS) include 12 requirements: two overarching standards for general principles and disclosures, and ten topical standards addressing areas like climate, biodiversity, and supply chain impacts [13]. This makes CSRD and ESRS among the most detailed frameworks currently in use.

The EU Green Finance Strategy aims to drive over $1.1 trillion in sustainable investments to reach climate neutrality by 2050. Meanwhile, the European Green Deal calls for approximately $510 billion annually in climate-related investments [13]. Companies subject to CSRD must assess climate risks across their full value chain and align their targets with the Paris Agreement, often referencing the Science Based Targets initiative (SBTi), which, as of early 2025, includes over 10,889 companies globally [13].

| Standard | Primary Focus | Materiality Approach | Current Status |

| --- | --- | --- | --- |

| <strong>TCFD</strong> | Climate-related financial risk | Financial | Disbanded (Integrated into ISSB) |

| <strong>ISSB (IFRS S1/S2)</strong> | Investor-focused sustainability | Financial | Active (Global Baseline) |

| <strong>CSRD / ESRS</strong> | Comprehensive ESG impact | Double Materiality | Active (EU Mandatory)

| Standard | Primary Focus | Materiality Approach | Current Status |

| --- | --- | --- | --- |

| <strong>TCFD</strong> | Climate-related financial risk | Financial | Disbanded (Integrated into ISSB) |

| <strong>ISSB (IFRS S1/S2)</strong> | Investor-focused sustainability | Financial | Active (Global Baseline) |

| <strong>CSRD / ESRS</strong> | Comprehensive ESG impact | Double Materiality | Active (EU Mandatory)

Despite differences in scope, these frameworks are becoming increasingly interconnected. Preparing for one often equips companies to meet the requirements of others. Organizations like Council Fire assist businesses in navigating these overlaps, ensuring their climate risk strategies align with multiple frameworks without redundant efforts.

Principles of Climate Risk Alignment Across Frameworks

While regional differences exist, global ESG frameworks share a foundational structure that guides organizations in addressing climate risks effectively [3].

Governance and Oversight

A cornerstone of all major frameworks is ensuring robust board-level oversight of climate risks. Companies are expected to disclose how their boards monitor and incorporate these risks into overall business strategies. Audit committees are pivotal in evaluating how climate risks influence financial statements, such as asset valuations and impairment tests. To strengthen this oversight, many organizations are forming specialized board committees with expertise in climate issues. Publishing a board skills matrix that highlights climate-related competencies further underscores a company's commitment to accountability. This level of governance lays the groundwork for thorough scenario analysis and transparent data reporting across different frameworks.

Scenario Analysis and Paris Alignment

Frameworks increasingly emphasize the importance of climate scenario analysis to evaluate the resilience of business strategies. This involves modeling performance under various climate conditions, including scenarios aligned with the Paris Agreement's 1.5°C or 2°C targets. Despite its importance, only 41% of companies currently disclose scenario analyses, even though 79% of investors are prioritizing climate transition risks [15]. These analyses are not merely theoretical exercises - they directly inform decisions about capital allocation, such as investing in sustainable infrastructure or retiring high-emission assets.

Gary Gensler [4] has highlighted the importance of such disclosures for fostering transparency and comparability. By aligning with Paris Agreement goals, organizations demonstrate proactive planning for a net-zero future rather than reacting to immediate regulatory demands. These practices collectively enhance ESG compliance and strategic foresight.

Metrics, Targets, and Data Quality

Effective climate risk management also hinges on reliable metrics and clearly defined targets. Companies are now expected to approach sustainability disclosures with the same precision as financial reporting [14]. This entails reporting absolute gross Scope 1 and Scope 2 greenhouse gas emissions using standardized methods, and, when relevant, including Scope 3 emissions. Setting science-based targets is essential for showing measurable progress toward decarbonization goals.

To ensure the integrity of climate data, many organizations are appointing ESG Controllers who implement rigorous data controls similar to those used in financial reporting. Mock audits are becoming a common practice, helping companies identify weaknesses in data collection and control systems ahead of regulatory deadlines. The finance function plays a critical role in this process. As Janine Guillot, CEO of the Value Reporting Foundation, explains:

"What the Finance function brings to the table is incredible amounts of experience aggregating data and building internal controls and governance around data" [16].

Aligning ESG reporting timelines with the financial close process further ensures timely and accurate disclosures. Together, these practices reinforce comprehensive ESG compliance and organizational resilience.

Council Fire incorporates these principles into its climate risk strategies, helping organizations build a foundation for long-term stability and success.

Practical Roadmap for Climate Risk and ESG Alignment

Establish Climate Risk Governance

Effective climate risk governance begins with establishing clear oversight at the board level. Organizations need to identify which board, committee, or individuals are responsible for managing climate-related risks and opportunities. These responsibilities should be formally documented in terms of reference and mandates, ensuring clarity and accountability [7][5]. Public documents, such as board committee charters, should also reflect this oversight [17].

To manage financial risks objectively, board committees must operate independently [17]. Conducting a skills gap analysis can help determine whether the board possesses the necessary expertise in climate issues. This analysis should be reflected in board matrices and director biographies, showcasing the board's preparedness [17][7]. Regular education sessions can further ensure that board members stay informed about evolving climate risks [17].

Clear management responsibilities are equally important. Appointing dedicated roles, such as a Chief Sustainability Officer, or forming cross-functional committees with representatives from finance, legal, risk management, and supply chain teams can foster company-wide coordination on climate initiatives [17]. Reporting frequencies should also be defined, with many boards opting for quarterly updates on climate risks to support timely decision-making [7][5].

Incentivizing climate performance through executive compensation is another critical step. Tying greenhouse gas reduction targets and other climate-related goals to bonus structures can drive accountability [7][17]. Audit committees should also play a role by overseeing climate disclosure processes and ensuring that both internal and external auditors address climate risks in their work [17].

With governance established, organizations can then focus on identifying key risks.

Conduct Materiality Assessments

Materiality assessments are essential for identifying and prioritizing climate risks that require attention and disclosure. These assessments should differentiate between financial materiality - risks that directly affect cash flows, financing, or the cost of capital - and double materiality, which considers both the impact of climate on the company and the company’s impact on the climate [7][1].

Key risks include physical risks, such as extreme weather, and transition risks related to regulatory and market changes. Industry-specific frameworks, like the IFRS S2 Industry-based Guidance, can help organizations identify risks relevant to their sectors [7][5]. Each risk should be evaluated based on its nature, likelihood, and potential impact across various time horizons. Additionally, organizations should pinpoint where these risks are concentrated, whether by geography, facilities, or asset types [7][5].

Integrating materiality assessments into existing enterprise risk management (ERM) processes is vital [18][3]. This requires collaboration across departments, including audit, finance, legal, operations, and supply chain teams [17]. Organizations should use all available information - historical data, current conditions, and future forecasts - to inform their assessments [7][5]. Scenario analyses, such as testing strategies under a 2°C or lower scenario, can provide insights into future conditions [3][5]. Revisiting these assessments annually ensures they remain relevant as risks and regulations evolve [18].

Once risks are clearly identified, organizations can move on to crafting transition plans.

Develop Paris-Aligned Transition Plans

Paris-aligned transition plans turn governance and risk insights into actionable strategies. The IFRS S2 baseline offers a global standard that incorporates recommendations from the Task Force on Climate-related Financial Disclosures (TCFD) [2][20]. These plans should address four key areas: governance, strategy, risk management, and metrics and targets [3][5].

A good starting point is conducting a gap analysis to compare current practices against the 11 TCFD recommendations. This helps assess readiness and identify areas for improvement [19]. Scenario analysis should continue to test the resilience of strategies under Paris Agreement targets [3][5]. Transition plans must outline how climate risks and opportunities could affect financial performance, position, and cash flows over specific time frames [5].

Resource allocation is a critical component of transition planning. Organizations should detail any anticipated changes to their business models, capital expenditures, funding sources, and the financial impacts of these changes [5]. For example, this might include phasing out carbon-intensive operations and investing in low-carbon alternatives. Where exact financial impacts are unclear, qualitative descriptions that identify affected financial statement line items can still provide valuable context [5].

For instance, in 2023, Bayer AG collaborated with BSR’s "Value Chain Risk to Resilience" working group. Nicolas Schweigert and his team enhanced Bayer’s climate scenario planning and supply chain resilience strategies. This collaborative effort helped Bayer identify key regulatory and physical climate risks while focusing on reducing greenhouse gas emissions [18]. Repeating such processes annually allows organizations to adapt to new data and regulatory developments [18].

Council Fire applies these principles to help organizations build strong governance structures, conduct thorough materiality assessments, and create transition plans that align environmental and economic priorities effectively.

Sector-Specific Climate Risk Considerations

The effects of climate change vary widely across industries, with sectors like natural resource management, energy and water infrastructure, and urban systems facing distinct challenges. Addressing these requires tailored ESG strategies that align with their unique operational realities.

Natural Resource Management

Industries dependent on natural resources grapple with a dual challenge: climate change disrupts their operations, while their activities can exacerbate environmental harm. This dynamic increases risks such as water scarcity, biodiversity loss, and land degradation. The IPCC emphasizes that climate risks stem from the interaction of hazards, exposure, and vulnerability [21].

The financial implications are significant. Around 60% of companies in the S&P Index own physical assets exposed to at least one type of climate-related physical risk [23]. If no action is taken, global GDP could shrink by as much as 22% by the end of the century due to climate impacts [21]. Companies in this sector must evaluate both their reliance on natural resources and their impact on ecosystems. The Taskforce on Nature-related Financial Disclosures (TNFD) provides a framework similar to the TCFD's, enabling organizations to report on nature-related dependencies alongside climate risks [21][22].

Sector-specific standards, like those from the Sustainability Accounting Standards Board (SASB), help identify material ESG risks for sub-sectors within natural resource management [22]. Strengthening ESG assessments across supply chains is also vital to mitigate reputational risks tied to harmful practices like deforestation [22]. Practical solutions, such as reforestation, landfill methane capture, and wastewater treatment, can reduce emissions while improving resource resilience [23]. These approaches underline the need for precise ESG alignment within this sector.

Energy and Water Infrastructure

Critical energy and water systems face two main threats: physical damage from climate events and the transition risks tied to the shift toward a low-carbon economy [5]. These systems must adapt to reducing carbon intensity while ensuring reliable service delivery, especially as rising digital demands place additional strain on energy grids [25].

Climate risks must be integrated into financial planning, particularly in areas like capital expenditures, acquisitions, and adjustments to the valuation of long-term assets [5][24]. The IFRS S2 framework mandates organizations to disclose the percentage of assets or activities exposed to physical and transition risks [5]. Effective governance is also essential, ensuring climate-related goals and performance metrics are tied to executive compensation [5].

Scenario analysis plays a crucial role in testing the resilience of infrastructure strategies under varying climate conditions. This includes evaluating factors like local weather patterns and resource availability [5]. Internal carbon pricing can also help organizations assess the financial impact of greenhouse gas emissions during investment planning [5]. As the IFRS Foundation explains:

"The objective of IFRS S2 Climate-related Disclosures is to require an entity to disclose information about its climate-related risks and opportunities that is useful to primary users of general purpose financial reports" [5].

Such tailored strategies ensure that infrastructure remains resilient while aligning with broader climate risk disclosure frameworks.

Communities and Urban Systems

Urban areas face growing challenges from extreme weather events, such as heatwaves and flooding, which strain infrastructure and exacerbate social equity issues. Building urban resilience requires not just robust infrastructure but also strong community engagement and social responsibility. ESG frameworks address these social aspects by focusing on human rights, workplace safety, and community relations [28].

New regulations now mandate corporate accountability for community impacts [25]. By late 2020, 92% of S&P 500 companies were already reporting ESG metrics, reflecting a heightened awareness of their effects on local communities [24]. However, organizations must go beyond generic reporting to address the specific geographic realities of their operations and their influence on local resilience [27].

The TCFD's relevance principle highlights the importance of tailoring climate disclosures to reflect local contexts and meet the informational needs of affected communities [27]. Companies are encouraged to present data on community-related climate risks in clear, accessible terms, backed by location-specific insights [27]. The Fifth National Climate Assessment, released in 2023, provides a valuable resource for understanding climate impacts on urban systems, rural areas, and the built environment [26].

Council Fire adopts a systems-thinking approach to translate these sector-specific challenges into actionable and measurable outcomes.

Conclusion: Achieving Climate Risk Alignment for Long-Term Success

Climate risk is no longer a distant concern - it directly impacts financial performance, operational stability, and long-term growth. As Janine Guillot, CEO of the Value Reporting Foundation, aptly puts it:

"Climate risk is business risk, and climate risk is relevant to financial performance and financial risk" [16].

Businesses that weave climate risk management into their ESG frameworks are better equipped to handle both physical disruptions and the challenges of transitioning to a low-carbon economy.

The push for standardized climate disclosures has gained significant momentum, with 89% of investors and 74% of finance leaders advocating for it [16]. Regulatory developments have further cemented this shift. The SEC's climate rules, finalized in March 2024 after reviewing over 24,000 comment letters [4], and the IFRS S1 and S2 standards, effective as of January 1, 2024 [29], have made compliance a necessity rather than an option. Organizations must now view climate alignment as a strategic priority embedded within their broader risk management frameworks.

To navigate this evolving landscape, companies need strong board oversight, frequent materiality assessments, scenario planning to test resilience, and robust data controls led by finance teams. The finance function plays a pivotal role, with 95% of finance leaders acknowledging their teams' importance in ESG reporting [16]. Their expertise in data governance and aggregation ensures that disclosures are accurate and meet the expectations of investors and stakeholders.

Council Fire supports organizations in translating global ESG principles into actionable strategies. With a systems-thinking approach, they help establish climate governance frameworks, conduct double materiality assessments, craft Paris-aligned transition plans, and integrate climate considerations into areas like resource management, energy and water infrastructure, and community resilience. The goal is clear: to build the operational strength needed to succeed in a climate-constrained world while generating meaningful environmental, social, and economic outcomes.

FAQs

What are the key differences between the ISSB and CSRD frameworks for climate risk reporting?

The ISSB’s IFRS S2 framework is centered on single materiality, concentrating on how climate risks influence a company’s financial performance. Its disclosures are designed to be straightforward and focused on providing investors with clear, relevant information.

On the other hand, the EU’s CSRD adopts a double materiality perspective. This means organizations must disclose not only how climate risks impact their business but also their broader environmental and social effects.

The CSRD framework requires more detailed reporting, including Scope 1, 2, and 3 emissions, stricter thresholds for determining materiality, and comprehensive scenario analyses. As a result, it is more demanding than the ISSB framework, which emphasizes simplicity and accessibility for investors over exhaustive reporting.

How does scenario analysis help businesses align their strategies with climate goals?

Scenario analysis offers businesses a way to evaluate how different climate-related scenarios could influence their operations, financial health, and strategic direction. By simulating various potential outcomes - such as rapid shifts toward decarbonization, delayed policy responses, or escalating physical threats like severe weather - companies can uncover risks that conventional planning might miss. These risks generally fall into two categories: transition risks, which include policy or market changes, and physical risks, such as flooding or temperature increases.

This approach enables organizations to make smarter decisions by stress-testing strategies, identifying weak points, and spotting new opportunities to align with climate objectives like net-zero emissions. Tools recommended by the Task Force on Climate-related Financial Disclosures (TCFD) provide a framework for developing robust strategies, enhancing transparency for investors and regulators, and building trust among stakeholders.

Council Fire collaborates with businesses to create scenario analyses tailored to their specific challenges and objectives. By applying these insights to areas like capital planning, product innovation, and risk management, companies can maintain their competitive edge, meet U.S. climate requirements, and support broader environmental and social goals.

Why is board oversight essential for managing climate risks effectively?

Board oversight plays a crucial role in managing climate risks effectively, ensuring these challenges are woven into an organization’s strategic goals, financial planning, and decision-making processes. When boards address climate risks directly, they align their responsibilities with the organization's long-term resilience and ability to generate value.

Regulatory bodies like the U.S. Securities and Exchange Commission (SEC) and frameworks such as the Task Force on Climate-related Financial Disclosures (TCFD) stress the importance of board involvement in overseeing climate-related risks. This level of engagement not only boosts accountability and transparency but also strengthens investor confidence and helps companies meet emerging disclosure expectations.

Council Fire works with organizations to establish governance practices at the board level that treat climate risks with the same seriousness as financial risks. By doing so, companies can align with global ESG standards and transform climate resilience into a strategic advantage.

Related Blog Posts

Latest Articles

©2025

FAQ

01

What does it really mean to “redefine profit”?

02

What makes Council Fire different?

03

Who does Council Fire you work with?

04

What does working with Council Fire actually look like?

05

How does Council Fire help organizations turn big goals into action?

06

How does Council Fire define and measure success?

Dec 29, 2025

Global ESG Standards: Climate Risk Alignment

ESG Strategy

In This Article

How TCFD, ISSB and CSRD turn climate risk into governance, disclosure and Paris-aligned transition plans for companies.

Global ESG Standards: Climate Risk Alignment

Climate risk is reshaping the corporate world, demanding action and transparency. With 2024 recorded as the hottest year in history, businesses face mounting challenges from extreme weather events, rising costs, and regulatory changes. This article outlines how global ESG standards like TCFD, ISSB, and CSRD are transforming climate risk into actionable strategies for companies.

Key Takeaways:

Climate Risk Types: Physical risks (e.g., hurricanes, wildfires) and transition risks (e.g., carbon pricing, regulations).

Major ESG Frameworks:

TCFD: Focused on financial materiality, now integrated into ISSB.

ISSB (IFRS S1/S2): Global baseline for sustainability reporting, emphasizing financial impacts and Scope 1, 2, and 3 emissions.

CSRD (EU): Double materiality approach, examining climate impact on companies and vice versa.

Regulatory Updates:SEC finalized climate disclosure rules in March 2024, and California laws (SB 253, SB 261) enforce stricter reporting.

Business Impact: ESG compliance influences investor trust, operational planning, and stakeholder relationships. 97% of executives report benefits from sustainability consulting and reporting.

Comparison of ESG Frameworks:

| Framework | Focus Area | Materiality Approach | Status |

| --- | --- | --- | --- |

| TCFD | Financial climate risk | Financial | Integrated into ISSB |

| ISSB | Investor-focused disclosures | Financial | Active (Global Baseline) |

| CSRD | Broader ESG impact | Double Materiality | Active (EU Mandatory)

This guide explores how these frameworks help businesses manage climate risks, align with global goals, and prepare for a low-carbon future.

Comparison of Global ESG Climate Risk Frameworks: TCFD, ISSB, and CSRD

Beyond compliance: Leveraging climate risk for a competitive edge

Key Global ESG Standards for Climate Risk

Three major frameworks shape how companies worldwide address climate risk disclosure. While they share a common four-pillar structure, each framework introduces distinct requirements and regional nuances. Together, they guide organizations through shifting regulations and help align their climate strategies with broader global expectations.

Task Force on Climate-related Financial Disclosures (TCFD)

The TCFD laid the groundwork for modern climate disclosure frameworks, elevating climate risk from a purely environmental issue to a financial priority. Established by the Financial Stability Board in 2015, it structured climate reporting around four key pillars: Governance, Strategy, Risk Management, and Metrics and Targets [3].

By late 2023, nearly 5,000 organizations had adopted TCFD recommendations [6]. Stuart Gulliver, Chief Executive of HSBC, emphasized the framework's value:

"These recommendations are a practical and pragmatic response to the need for consistent and comparable climate-related financial disclosure" [6].

Before TCFD's widespread adoption, research by HSBC found that fewer than 25% of companies disclosed their environmental impact [6]. Following its 2023 status report, the TCFD concluded its mission and disbanded, passing its legacy to the IFRS Foundation. The foundation, through the International Sustainability Standards Board (ISSB), now oversees and refines climate-related disclosure standards [3][6].

IFRS Sustainability Disclosure Standards (ISSB: IFRS S1 and S2)

Building on TCFD's foundation, the ISSB establishes a mandatory global baseline for sustainability reporting. IFRS S2, effective for annual reporting periods starting January 1, 2024, introduces greater detail and precision to climate risk disclosures [9][12].

A key focus of IFRS S2 is financial materiality, requiring companies to report information that could influence cash flows, financing, or capital costs [7][11]. Companies must disclose absolute gross Scope 1, Scope 2, and Scope 3 greenhouse gas emissions, using the Greenhouse Gas Protocol: A Corporate Accounting and Reporting Standard [8][5]. They are also tasked with conducting scenario analyses and providing detailed transition plans [7][5].

In December 2025, the ISSB implemented amendments to simplify greenhouse gas emissions disclosures [9]. The framework also incorporates industry-specific requirements based on SASB Standards, adding sector-specific depth [9][10]. According to the IFRS Foundation:

"IFRS S2 integrates and builds on the recommendations of the Task Force on Climate-related Financial Disclosures (TCFD) and incorporates industry-based disclosure requirements derived from SASB Standards" [9].

For industries like asset management, commercial banking, and insurance, IFRS S2 mandates disclosures on financed emissions tied to investments [8][5]. While ISSB focuses on investor needs, the EU's CSRD takes a broader approach by incorporating double materiality.

EU Corporate Sustainability Reporting Directive (CSRD) and ESRS

The CSRD applies a double materiality perspective, requiring companies to report both on how climate change impacts their financial performance (outside-in) and how their operations affect the environment and society (inside-out) [13].

The European Sustainability Reporting Standards (ESRS) include 12 requirements: two overarching standards for general principles and disclosures, and ten topical standards addressing areas like climate, biodiversity, and supply chain impacts [13]. This makes CSRD and ESRS among the most detailed frameworks currently in use.

The EU Green Finance Strategy aims to drive over $1.1 trillion in sustainable investments to reach climate neutrality by 2050. Meanwhile, the European Green Deal calls for approximately $510 billion annually in climate-related investments [13]. Companies subject to CSRD must assess climate risks across their full value chain and align their targets with the Paris Agreement, often referencing the Science Based Targets initiative (SBTi), which, as of early 2025, includes over 10,889 companies globally [13].

| Standard | Primary Focus | Materiality Approach | Current Status |

| --- | --- | --- | --- |

| <strong>TCFD</strong> | Climate-related financial risk | Financial | Disbanded (Integrated into ISSB) |

| <strong>ISSB (IFRS S1/S2)</strong> | Investor-focused sustainability | Financial | Active (Global Baseline) |

| <strong>CSRD / ESRS</strong> | Comprehensive ESG impact | Double Materiality | Active (EU Mandatory)

Despite differences in scope, these frameworks are becoming increasingly interconnected. Preparing for one often equips companies to meet the requirements of others. Organizations like Council Fire assist businesses in navigating these overlaps, ensuring their climate risk strategies align with multiple frameworks without redundant efforts.

Principles of Climate Risk Alignment Across Frameworks

While regional differences exist, global ESG frameworks share a foundational structure that guides organizations in addressing climate risks effectively [3].

Governance and Oversight

A cornerstone of all major frameworks is ensuring robust board-level oversight of climate risks. Companies are expected to disclose how their boards monitor and incorporate these risks into overall business strategies. Audit committees are pivotal in evaluating how climate risks influence financial statements, such as asset valuations and impairment tests. To strengthen this oversight, many organizations are forming specialized board committees with expertise in climate issues. Publishing a board skills matrix that highlights climate-related competencies further underscores a company's commitment to accountability. This level of governance lays the groundwork for thorough scenario analysis and transparent data reporting across different frameworks.

Scenario Analysis and Paris Alignment

Frameworks increasingly emphasize the importance of climate scenario analysis to evaluate the resilience of business strategies. This involves modeling performance under various climate conditions, including scenarios aligned with the Paris Agreement's 1.5°C or 2°C targets. Despite its importance, only 41% of companies currently disclose scenario analyses, even though 79% of investors are prioritizing climate transition risks [15]. These analyses are not merely theoretical exercises - they directly inform decisions about capital allocation, such as investing in sustainable infrastructure or retiring high-emission assets.

Gary Gensler [4] has highlighted the importance of such disclosures for fostering transparency and comparability. By aligning with Paris Agreement goals, organizations demonstrate proactive planning for a net-zero future rather than reacting to immediate regulatory demands. These practices collectively enhance ESG compliance and strategic foresight.

Metrics, Targets, and Data Quality

Effective climate risk management also hinges on reliable metrics and clearly defined targets. Companies are now expected to approach sustainability disclosures with the same precision as financial reporting [14]. This entails reporting absolute gross Scope 1 and Scope 2 greenhouse gas emissions using standardized methods, and, when relevant, including Scope 3 emissions. Setting science-based targets is essential for showing measurable progress toward decarbonization goals.

To ensure the integrity of climate data, many organizations are appointing ESG Controllers who implement rigorous data controls similar to those used in financial reporting. Mock audits are becoming a common practice, helping companies identify weaknesses in data collection and control systems ahead of regulatory deadlines. The finance function plays a critical role in this process. As Janine Guillot, CEO of the Value Reporting Foundation, explains:

"What the Finance function brings to the table is incredible amounts of experience aggregating data and building internal controls and governance around data" [16].

Aligning ESG reporting timelines with the financial close process further ensures timely and accurate disclosures. Together, these practices reinforce comprehensive ESG compliance and organizational resilience.

Council Fire incorporates these principles into its climate risk strategies, helping organizations build a foundation for long-term stability and success.

Practical Roadmap for Climate Risk and ESG Alignment

Establish Climate Risk Governance

Effective climate risk governance begins with establishing clear oversight at the board level. Organizations need to identify which board, committee, or individuals are responsible for managing climate-related risks and opportunities. These responsibilities should be formally documented in terms of reference and mandates, ensuring clarity and accountability [7][5]. Public documents, such as board committee charters, should also reflect this oversight [17].

To manage financial risks objectively, board committees must operate independently [17]. Conducting a skills gap analysis can help determine whether the board possesses the necessary expertise in climate issues. This analysis should be reflected in board matrices and director biographies, showcasing the board's preparedness [17][7]. Regular education sessions can further ensure that board members stay informed about evolving climate risks [17].

Clear management responsibilities are equally important. Appointing dedicated roles, such as a Chief Sustainability Officer, or forming cross-functional committees with representatives from finance, legal, risk management, and supply chain teams can foster company-wide coordination on climate initiatives [17]. Reporting frequencies should also be defined, with many boards opting for quarterly updates on climate risks to support timely decision-making [7][5].

Incentivizing climate performance through executive compensation is another critical step. Tying greenhouse gas reduction targets and other climate-related goals to bonus structures can drive accountability [7][17]. Audit committees should also play a role by overseeing climate disclosure processes and ensuring that both internal and external auditors address climate risks in their work [17].

With governance established, organizations can then focus on identifying key risks.

Conduct Materiality Assessments

Materiality assessments are essential for identifying and prioritizing climate risks that require attention and disclosure. These assessments should differentiate between financial materiality - risks that directly affect cash flows, financing, or the cost of capital - and double materiality, which considers both the impact of climate on the company and the company’s impact on the climate [7][1].

Key risks include physical risks, such as extreme weather, and transition risks related to regulatory and market changes. Industry-specific frameworks, like the IFRS S2 Industry-based Guidance, can help organizations identify risks relevant to their sectors [7][5]. Each risk should be evaluated based on its nature, likelihood, and potential impact across various time horizons. Additionally, organizations should pinpoint where these risks are concentrated, whether by geography, facilities, or asset types [7][5].

Integrating materiality assessments into existing enterprise risk management (ERM) processes is vital [18][3]. This requires collaboration across departments, including audit, finance, legal, operations, and supply chain teams [17]. Organizations should use all available information - historical data, current conditions, and future forecasts - to inform their assessments [7][5]. Scenario analyses, such as testing strategies under a 2°C or lower scenario, can provide insights into future conditions [3][5]. Revisiting these assessments annually ensures they remain relevant as risks and regulations evolve [18].

Once risks are clearly identified, organizations can move on to crafting transition plans.

Develop Paris-Aligned Transition Plans

Paris-aligned transition plans turn governance and risk insights into actionable strategies. The IFRS S2 baseline offers a global standard that incorporates recommendations from the Task Force on Climate-related Financial Disclosures (TCFD) [2][20]. These plans should address four key areas: governance, strategy, risk management, and metrics and targets [3][5].

A good starting point is conducting a gap analysis to compare current practices against the 11 TCFD recommendations. This helps assess readiness and identify areas for improvement [19]. Scenario analysis should continue to test the resilience of strategies under Paris Agreement targets [3][5]. Transition plans must outline how climate risks and opportunities could affect financial performance, position, and cash flows over specific time frames [5].

Resource allocation is a critical component of transition planning. Organizations should detail any anticipated changes to their business models, capital expenditures, funding sources, and the financial impacts of these changes [5]. For example, this might include phasing out carbon-intensive operations and investing in low-carbon alternatives. Where exact financial impacts are unclear, qualitative descriptions that identify affected financial statement line items can still provide valuable context [5].

For instance, in 2023, Bayer AG collaborated with BSR’s "Value Chain Risk to Resilience" working group. Nicolas Schweigert and his team enhanced Bayer’s climate scenario planning and supply chain resilience strategies. This collaborative effort helped Bayer identify key regulatory and physical climate risks while focusing on reducing greenhouse gas emissions [18]. Repeating such processes annually allows organizations to adapt to new data and regulatory developments [18].

Council Fire applies these principles to help organizations build strong governance structures, conduct thorough materiality assessments, and create transition plans that align environmental and economic priorities effectively.

Sector-Specific Climate Risk Considerations

The effects of climate change vary widely across industries, with sectors like natural resource management, energy and water infrastructure, and urban systems facing distinct challenges. Addressing these requires tailored ESG strategies that align with their unique operational realities.

Natural Resource Management

Industries dependent on natural resources grapple with a dual challenge: climate change disrupts their operations, while their activities can exacerbate environmental harm. This dynamic increases risks such as water scarcity, biodiversity loss, and land degradation. The IPCC emphasizes that climate risks stem from the interaction of hazards, exposure, and vulnerability [21].

The financial implications are significant. Around 60% of companies in the S&P Index own physical assets exposed to at least one type of climate-related physical risk [23]. If no action is taken, global GDP could shrink by as much as 22% by the end of the century due to climate impacts [21]. Companies in this sector must evaluate both their reliance on natural resources and their impact on ecosystems. The Taskforce on Nature-related Financial Disclosures (TNFD) provides a framework similar to the TCFD's, enabling organizations to report on nature-related dependencies alongside climate risks [21][22].

Sector-specific standards, like those from the Sustainability Accounting Standards Board (SASB), help identify material ESG risks for sub-sectors within natural resource management [22]. Strengthening ESG assessments across supply chains is also vital to mitigate reputational risks tied to harmful practices like deforestation [22]. Practical solutions, such as reforestation, landfill methane capture, and wastewater treatment, can reduce emissions while improving resource resilience [23]. These approaches underline the need for precise ESG alignment within this sector.

Energy and Water Infrastructure

Critical energy and water systems face two main threats: physical damage from climate events and the transition risks tied to the shift toward a low-carbon economy [5]. These systems must adapt to reducing carbon intensity while ensuring reliable service delivery, especially as rising digital demands place additional strain on energy grids [25].

Climate risks must be integrated into financial planning, particularly in areas like capital expenditures, acquisitions, and adjustments to the valuation of long-term assets [5][24]. The IFRS S2 framework mandates organizations to disclose the percentage of assets or activities exposed to physical and transition risks [5]. Effective governance is also essential, ensuring climate-related goals and performance metrics are tied to executive compensation [5].

Scenario analysis plays a crucial role in testing the resilience of infrastructure strategies under varying climate conditions. This includes evaluating factors like local weather patterns and resource availability [5]. Internal carbon pricing can also help organizations assess the financial impact of greenhouse gas emissions during investment planning [5]. As the IFRS Foundation explains:

"The objective of IFRS S2 Climate-related Disclosures is to require an entity to disclose information about its climate-related risks and opportunities that is useful to primary users of general purpose financial reports" [5].

Such tailored strategies ensure that infrastructure remains resilient while aligning with broader climate risk disclosure frameworks.

Communities and Urban Systems

Urban areas face growing challenges from extreme weather events, such as heatwaves and flooding, which strain infrastructure and exacerbate social equity issues. Building urban resilience requires not just robust infrastructure but also strong community engagement and social responsibility. ESG frameworks address these social aspects by focusing on human rights, workplace safety, and community relations [28].

New regulations now mandate corporate accountability for community impacts [25]. By late 2020, 92% of S&P 500 companies were already reporting ESG metrics, reflecting a heightened awareness of their effects on local communities [24]. However, organizations must go beyond generic reporting to address the specific geographic realities of their operations and their influence on local resilience [27].

The TCFD's relevance principle highlights the importance of tailoring climate disclosures to reflect local contexts and meet the informational needs of affected communities [27]. Companies are encouraged to present data on community-related climate risks in clear, accessible terms, backed by location-specific insights [27]. The Fifth National Climate Assessment, released in 2023, provides a valuable resource for understanding climate impacts on urban systems, rural areas, and the built environment [26].

Council Fire adopts a systems-thinking approach to translate these sector-specific challenges into actionable and measurable outcomes.

Conclusion: Achieving Climate Risk Alignment for Long-Term Success

Climate risk is no longer a distant concern - it directly impacts financial performance, operational stability, and long-term growth. As Janine Guillot, CEO of the Value Reporting Foundation, aptly puts it:

"Climate risk is business risk, and climate risk is relevant to financial performance and financial risk" [16].

Businesses that weave climate risk management into their ESG frameworks are better equipped to handle both physical disruptions and the challenges of transitioning to a low-carbon economy.

The push for standardized climate disclosures has gained significant momentum, with 89% of investors and 74% of finance leaders advocating for it [16]. Regulatory developments have further cemented this shift. The SEC's climate rules, finalized in March 2024 after reviewing over 24,000 comment letters [4], and the IFRS S1 and S2 standards, effective as of January 1, 2024 [29], have made compliance a necessity rather than an option. Organizations must now view climate alignment as a strategic priority embedded within their broader risk management frameworks.

To navigate this evolving landscape, companies need strong board oversight, frequent materiality assessments, scenario planning to test resilience, and robust data controls led by finance teams. The finance function plays a pivotal role, with 95% of finance leaders acknowledging their teams' importance in ESG reporting [16]. Their expertise in data governance and aggregation ensures that disclosures are accurate and meet the expectations of investors and stakeholders.

Council Fire supports organizations in translating global ESG principles into actionable strategies. With a systems-thinking approach, they help establish climate governance frameworks, conduct double materiality assessments, craft Paris-aligned transition plans, and integrate climate considerations into areas like resource management, energy and water infrastructure, and community resilience. The goal is clear: to build the operational strength needed to succeed in a climate-constrained world while generating meaningful environmental, social, and economic outcomes.

FAQs

What are the key differences between the ISSB and CSRD frameworks for climate risk reporting?

The ISSB’s IFRS S2 framework is centered on single materiality, concentrating on how climate risks influence a company’s financial performance. Its disclosures are designed to be straightforward and focused on providing investors with clear, relevant information.

On the other hand, the EU’s CSRD adopts a double materiality perspective. This means organizations must disclose not only how climate risks impact their business but also their broader environmental and social effects.

The CSRD framework requires more detailed reporting, including Scope 1, 2, and 3 emissions, stricter thresholds for determining materiality, and comprehensive scenario analyses. As a result, it is more demanding than the ISSB framework, which emphasizes simplicity and accessibility for investors over exhaustive reporting.

How does scenario analysis help businesses align their strategies with climate goals?

Scenario analysis offers businesses a way to evaluate how different climate-related scenarios could influence their operations, financial health, and strategic direction. By simulating various potential outcomes - such as rapid shifts toward decarbonization, delayed policy responses, or escalating physical threats like severe weather - companies can uncover risks that conventional planning might miss. These risks generally fall into two categories: transition risks, which include policy or market changes, and physical risks, such as flooding or temperature increases.

This approach enables organizations to make smarter decisions by stress-testing strategies, identifying weak points, and spotting new opportunities to align with climate objectives like net-zero emissions. Tools recommended by the Task Force on Climate-related Financial Disclosures (TCFD) provide a framework for developing robust strategies, enhancing transparency for investors and regulators, and building trust among stakeholders.

Council Fire collaborates with businesses to create scenario analyses tailored to their specific challenges and objectives. By applying these insights to areas like capital planning, product innovation, and risk management, companies can maintain their competitive edge, meet U.S. climate requirements, and support broader environmental and social goals.

Why is board oversight essential for managing climate risks effectively?

Board oversight plays a crucial role in managing climate risks effectively, ensuring these challenges are woven into an organization’s strategic goals, financial planning, and decision-making processes. When boards address climate risks directly, they align their responsibilities with the organization's long-term resilience and ability to generate value.

Regulatory bodies like the U.S. Securities and Exchange Commission (SEC) and frameworks such as the Task Force on Climate-related Financial Disclosures (TCFD) stress the importance of board involvement in overseeing climate-related risks. This level of engagement not only boosts accountability and transparency but also strengthens investor confidence and helps companies meet emerging disclosure expectations.

Council Fire works with organizations to establish governance practices at the board level that treat climate risks with the same seriousness as financial risks. By doing so, companies can align with global ESG standards and transform climate resilience into a strategic advantage.

Related Blog Posts

FAQ

01

What does it really mean to “redefine profit”?

02

What makes Council Fire different?

03

Who does Council Fire you work with?

04

What does working with Council Fire actually look like?

05

How does Council Fire help organizations turn big goals into action?

06

How does Council Fire define and measure success?

Dec 29, 2025

Global ESG Standards: Climate Risk Alignment

ESG Strategy

In This Article

How TCFD, ISSB and CSRD turn climate risk into governance, disclosure and Paris-aligned transition plans for companies.

Global ESG Standards: Climate Risk Alignment

Climate risk is reshaping the corporate world, demanding action and transparency. With 2024 recorded as the hottest year in history, businesses face mounting challenges from extreme weather events, rising costs, and regulatory changes. This article outlines how global ESG standards like TCFD, ISSB, and CSRD are transforming climate risk into actionable strategies for companies.

Key Takeaways:

Climate Risk Types: Physical risks (e.g., hurricanes, wildfires) and transition risks (e.g., carbon pricing, regulations).

Major ESG Frameworks:

TCFD: Focused on financial materiality, now integrated into ISSB.

ISSB (IFRS S1/S2): Global baseline for sustainability reporting, emphasizing financial impacts and Scope 1, 2, and 3 emissions.

CSRD (EU): Double materiality approach, examining climate impact on companies and vice versa.

Regulatory Updates:SEC finalized climate disclosure rules in March 2024, and California laws (SB 253, SB 261) enforce stricter reporting.

Business Impact: ESG compliance influences investor trust, operational planning, and stakeholder relationships. 97% of executives report benefits from sustainability consulting and reporting.

Comparison of ESG Frameworks:

| Framework | Focus Area | Materiality Approach | Status |

| --- | --- | --- | --- |

| TCFD | Financial climate risk | Financial | Integrated into ISSB |

| ISSB | Investor-focused disclosures | Financial | Active (Global Baseline) |

| CSRD | Broader ESG impact | Double Materiality | Active (EU Mandatory)

This guide explores how these frameworks help businesses manage climate risks, align with global goals, and prepare for a low-carbon future.

Comparison of Global ESG Climate Risk Frameworks: TCFD, ISSB, and CSRD

Beyond compliance: Leveraging climate risk for a competitive edge

Key Global ESG Standards for Climate Risk

Three major frameworks shape how companies worldwide address climate risk disclosure. While they share a common four-pillar structure, each framework introduces distinct requirements and regional nuances. Together, they guide organizations through shifting regulations and help align their climate strategies with broader global expectations.

Task Force on Climate-related Financial Disclosures (TCFD)

The TCFD laid the groundwork for modern climate disclosure frameworks, elevating climate risk from a purely environmental issue to a financial priority. Established by the Financial Stability Board in 2015, it structured climate reporting around four key pillars: Governance, Strategy, Risk Management, and Metrics and Targets [3].

By late 2023, nearly 5,000 organizations had adopted TCFD recommendations [6]. Stuart Gulliver, Chief Executive of HSBC, emphasized the framework's value:

"These recommendations are a practical and pragmatic response to the need for consistent and comparable climate-related financial disclosure" [6].

Before TCFD's widespread adoption, research by HSBC found that fewer than 25% of companies disclosed their environmental impact [6]. Following its 2023 status report, the TCFD concluded its mission and disbanded, passing its legacy to the IFRS Foundation. The foundation, through the International Sustainability Standards Board (ISSB), now oversees and refines climate-related disclosure standards [3][6].

IFRS Sustainability Disclosure Standards (ISSB: IFRS S1 and S2)

Building on TCFD's foundation, the ISSB establishes a mandatory global baseline for sustainability reporting. IFRS S2, effective for annual reporting periods starting January 1, 2024, introduces greater detail and precision to climate risk disclosures [9][12].

A key focus of IFRS S2 is financial materiality, requiring companies to report information that could influence cash flows, financing, or capital costs [7][11]. Companies must disclose absolute gross Scope 1, Scope 2, and Scope 3 greenhouse gas emissions, using the Greenhouse Gas Protocol: A Corporate Accounting and Reporting Standard [8][5]. They are also tasked with conducting scenario analyses and providing detailed transition plans [7][5].

In December 2025, the ISSB implemented amendments to simplify greenhouse gas emissions disclosures [9]. The framework also incorporates industry-specific requirements based on SASB Standards, adding sector-specific depth [9][10]. According to the IFRS Foundation:

"IFRS S2 integrates and builds on the recommendations of the Task Force on Climate-related Financial Disclosures (TCFD) and incorporates industry-based disclosure requirements derived from SASB Standards" [9].

For industries like asset management, commercial banking, and insurance, IFRS S2 mandates disclosures on financed emissions tied to investments [8][5]. While ISSB focuses on investor needs, the EU's CSRD takes a broader approach by incorporating double materiality.

EU Corporate Sustainability Reporting Directive (CSRD) and ESRS

The CSRD applies a double materiality perspective, requiring companies to report both on how climate change impacts their financial performance (outside-in) and how their operations affect the environment and society (inside-out) [13].

The European Sustainability Reporting Standards (ESRS) include 12 requirements: two overarching standards for general principles and disclosures, and ten topical standards addressing areas like climate, biodiversity, and supply chain impacts [13]. This makes CSRD and ESRS among the most detailed frameworks currently in use.

The EU Green Finance Strategy aims to drive over $1.1 trillion in sustainable investments to reach climate neutrality by 2050. Meanwhile, the European Green Deal calls for approximately $510 billion annually in climate-related investments [13]. Companies subject to CSRD must assess climate risks across their full value chain and align their targets with the Paris Agreement, often referencing the Science Based Targets initiative (SBTi), which, as of early 2025, includes over 10,889 companies globally [13].

| Standard | Primary Focus | Materiality Approach | Current Status |

| --- | --- | --- | --- |

| <strong>TCFD</strong> | Climate-related financial risk | Financial | Disbanded (Integrated into ISSB) |

| <strong>ISSB (IFRS S1/S2)</strong> | Investor-focused sustainability | Financial | Active (Global Baseline) |

| <strong>CSRD / ESRS</strong> | Comprehensive ESG impact | Double Materiality | Active (EU Mandatory)

Despite differences in scope, these frameworks are becoming increasingly interconnected. Preparing for one often equips companies to meet the requirements of others. Organizations like Council Fire assist businesses in navigating these overlaps, ensuring their climate risk strategies align with multiple frameworks without redundant efforts.

Principles of Climate Risk Alignment Across Frameworks

While regional differences exist, global ESG frameworks share a foundational structure that guides organizations in addressing climate risks effectively [3].

Governance and Oversight

A cornerstone of all major frameworks is ensuring robust board-level oversight of climate risks. Companies are expected to disclose how their boards monitor and incorporate these risks into overall business strategies. Audit committees are pivotal in evaluating how climate risks influence financial statements, such as asset valuations and impairment tests. To strengthen this oversight, many organizations are forming specialized board committees with expertise in climate issues. Publishing a board skills matrix that highlights climate-related competencies further underscores a company's commitment to accountability. This level of governance lays the groundwork for thorough scenario analysis and transparent data reporting across different frameworks.

Scenario Analysis and Paris Alignment

Frameworks increasingly emphasize the importance of climate scenario analysis to evaluate the resilience of business strategies. This involves modeling performance under various climate conditions, including scenarios aligned with the Paris Agreement's 1.5°C or 2°C targets. Despite its importance, only 41% of companies currently disclose scenario analyses, even though 79% of investors are prioritizing climate transition risks [15]. These analyses are not merely theoretical exercises - they directly inform decisions about capital allocation, such as investing in sustainable infrastructure or retiring high-emission assets.

Gary Gensler [4] has highlighted the importance of such disclosures for fostering transparency and comparability. By aligning with Paris Agreement goals, organizations demonstrate proactive planning for a net-zero future rather than reacting to immediate regulatory demands. These practices collectively enhance ESG compliance and strategic foresight.

Metrics, Targets, and Data Quality

Effective climate risk management also hinges on reliable metrics and clearly defined targets. Companies are now expected to approach sustainability disclosures with the same precision as financial reporting [14]. This entails reporting absolute gross Scope 1 and Scope 2 greenhouse gas emissions using standardized methods, and, when relevant, including Scope 3 emissions. Setting science-based targets is essential for showing measurable progress toward decarbonization goals.

To ensure the integrity of climate data, many organizations are appointing ESG Controllers who implement rigorous data controls similar to those used in financial reporting. Mock audits are becoming a common practice, helping companies identify weaknesses in data collection and control systems ahead of regulatory deadlines. The finance function plays a critical role in this process. As Janine Guillot, CEO of the Value Reporting Foundation, explains:

"What the Finance function brings to the table is incredible amounts of experience aggregating data and building internal controls and governance around data" [16].

Aligning ESG reporting timelines with the financial close process further ensures timely and accurate disclosures. Together, these practices reinforce comprehensive ESG compliance and organizational resilience.

Council Fire incorporates these principles into its climate risk strategies, helping organizations build a foundation for long-term stability and success.

Practical Roadmap for Climate Risk and ESG Alignment

Establish Climate Risk Governance

Effective climate risk governance begins with establishing clear oversight at the board level. Organizations need to identify which board, committee, or individuals are responsible for managing climate-related risks and opportunities. These responsibilities should be formally documented in terms of reference and mandates, ensuring clarity and accountability [7][5]. Public documents, such as board committee charters, should also reflect this oversight [17].

To manage financial risks objectively, board committees must operate independently [17]. Conducting a skills gap analysis can help determine whether the board possesses the necessary expertise in climate issues. This analysis should be reflected in board matrices and director biographies, showcasing the board's preparedness [17][7]. Regular education sessions can further ensure that board members stay informed about evolving climate risks [17].

Clear management responsibilities are equally important. Appointing dedicated roles, such as a Chief Sustainability Officer, or forming cross-functional committees with representatives from finance, legal, risk management, and supply chain teams can foster company-wide coordination on climate initiatives [17]. Reporting frequencies should also be defined, with many boards opting for quarterly updates on climate risks to support timely decision-making [7][5].

Incentivizing climate performance through executive compensation is another critical step. Tying greenhouse gas reduction targets and other climate-related goals to bonus structures can drive accountability [7][17]. Audit committees should also play a role by overseeing climate disclosure processes and ensuring that both internal and external auditors address climate risks in their work [17].

With governance established, organizations can then focus on identifying key risks.

Conduct Materiality Assessments

Materiality assessments are essential for identifying and prioritizing climate risks that require attention and disclosure. These assessments should differentiate between financial materiality - risks that directly affect cash flows, financing, or the cost of capital - and double materiality, which considers both the impact of climate on the company and the company’s impact on the climate [7][1].

Key risks include physical risks, such as extreme weather, and transition risks related to regulatory and market changes. Industry-specific frameworks, like the IFRS S2 Industry-based Guidance, can help organizations identify risks relevant to their sectors [7][5]. Each risk should be evaluated based on its nature, likelihood, and potential impact across various time horizons. Additionally, organizations should pinpoint where these risks are concentrated, whether by geography, facilities, or asset types [7][5].

Integrating materiality assessments into existing enterprise risk management (ERM) processes is vital [18][3]. This requires collaboration across departments, including audit, finance, legal, operations, and supply chain teams [17]. Organizations should use all available information - historical data, current conditions, and future forecasts - to inform their assessments [7][5]. Scenario analyses, such as testing strategies under a 2°C or lower scenario, can provide insights into future conditions [3][5]. Revisiting these assessments annually ensures they remain relevant as risks and regulations evolve [18].

Once risks are clearly identified, organizations can move on to crafting transition plans.

Develop Paris-Aligned Transition Plans

Paris-aligned transition plans turn governance and risk insights into actionable strategies. The IFRS S2 baseline offers a global standard that incorporates recommendations from the Task Force on Climate-related Financial Disclosures (TCFD) [2][20]. These plans should address four key areas: governance, strategy, risk management, and metrics and targets [3][5].

A good starting point is conducting a gap analysis to compare current practices against the 11 TCFD recommendations. This helps assess readiness and identify areas for improvement [19]. Scenario analysis should continue to test the resilience of strategies under Paris Agreement targets [3][5]. Transition plans must outline how climate risks and opportunities could affect financial performance, position, and cash flows over specific time frames [5].

Resource allocation is a critical component of transition planning. Organizations should detail any anticipated changes to their business models, capital expenditures, funding sources, and the financial impacts of these changes [5]. For example, this might include phasing out carbon-intensive operations and investing in low-carbon alternatives. Where exact financial impacts are unclear, qualitative descriptions that identify affected financial statement line items can still provide valuable context [5].

For instance, in 2023, Bayer AG collaborated with BSR’s "Value Chain Risk to Resilience" working group. Nicolas Schweigert and his team enhanced Bayer’s climate scenario planning and supply chain resilience strategies. This collaborative effort helped Bayer identify key regulatory and physical climate risks while focusing on reducing greenhouse gas emissions [18]. Repeating such processes annually allows organizations to adapt to new data and regulatory developments [18].

Council Fire applies these principles to help organizations build strong governance structures, conduct thorough materiality assessments, and create transition plans that align environmental and economic priorities effectively.

Sector-Specific Climate Risk Considerations

The effects of climate change vary widely across industries, with sectors like natural resource management, energy and water infrastructure, and urban systems facing distinct challenges. Addressing these requires tailored ESG strategies that align with their unique operational realities.

Natural Resource Management

Industries dependent on natural resources grapple with a dual challenge: climate change disrupts their operations, while their activities can exacerbate environmental harm. This dynamic increases risks such as water scarcity, biodiversity loss, and land degradation. The IPCC emphasizes that climate risks stem from the interaction of hazards, exposure, and vulnerability [21].

The financial implications are significant. Around 60% of companies in the S&P Index own physical assets exposed to at least one type of climate-related physical risk [23]. If no action is taken, global GDP could shrink by as much as 22% by the end of the century due to climate impacts [21]. Companies in this sector must evaluate both their reliance on natural resources and their impact on ecosystems. The Taskforce on Nature-related Financial Disclosures (TNFD) provides a framework similar to the TCFD's, enabling organizations to report on nature-related dependencies alongside climate risks [21][22].

Sector-specific standards, like those from the Sustainability Accounting Standards Board (SASB), help identify material ESG risks for sub-sectors within natural resource management [22]. Strengthening ESG assessments across supply chains is also vital to mitigate reputational risks tied to harmful practices like deforestation [22]. Practical solutions, such as reforestation, landfill methane capture, and wastewater treatment, can reduce emissions while improving resource resilience [23]. These approaches underline the need for precise ESG alignment within this sector.

Energy and Water Infrastructure

Critical energy and water systems face two main threats: physical damage from climate events and the transition risks tied to the shift toward a low-carbon economy [5]. These systems must adapt to reducing carbon intensity while ensuring reliable service delivery, especially as rising digital demands place additional strain on energy grids [25].

Climate risks must be integrated into financial planning, particularly in areas like capital expenditures, acquisitions, and adjustments to the valuation of long-term assets [5][24]. The IFRS S2 framework mandates organizations to disclose the percentage of assets or activities exposed to physical and transition risks [5]. Effective governance is also essential, ensuring climate-related goals and performance metrics are tied to executive compensation [5].

Scenario analysis plays a crucial role in testing the resilience of infrastructure strategies under varying climate conditions. This includes evaluating factors like local weather patterns and resource availability [5]. Internal carbon pricing can also help organizations assess the financial impact of greenhouse gas emissions during investment planning [5]. As the IFRS Foundation explains:

"The objective of IFRS S2 Climate-related Disclosures is to require an entity to disclose information about its climate-related risks and opportunities that is useful to primary users of general purpose financial reports" [5].

Such tailored strategies ensure that infrastructure remains resilient while aligning with broader climate risk disclosure frameworks.

Communities and Urban Systems

Urban areas face growing challenges from extreme weather events, such as heatwaves and flooding, which strain infrastructure and exacerbate social equity issues. Building urban resilience requires not just robust infrastructure but also strong community engagement and social responsibility. ESG frameworks address these social aspects by focusing on human rights, workplace safety, and community relations [28].

New regulations now mandate corporate accountability for community impacts [25]. By late 2020, 92% of S&P 500 companies were already reporting ESG metrics, reflecting a heightened awareness of their effects on local communities [24]. However, organizations must go beyond generic reporting to address the specific geographic realities of their operations and their influence on local resilience [27].

The TCFD's relevance principle highlights the importance of tailoring climate disclosures to reflect local contexts and meet the informational needs of affected communities [27]. Companies are encouraged to present data on community-related climate risks in clear, accessible terms, backed by location-specific insights [27]. The Fifth National Climate Assessment, released in 2023, provides a valuable resource for understanding climate impacts on urban systems, rural areas, and the built environment [26].

Council Fire adopts a systems-thinking approach to translate these sector-specific challenges into actionable and measurable outcomes.

Conclusion: Achieving Climate Risk Alignment for Long-Term Success

Climate risk is no longer a distant concern - it directly impacts financial performance, operational stability, and long-term growth. As Janine Guillot, CEO of the Value Reporting Foundation, aptly puts it:

"Climate risk is business risk, and climate risk is relevant to financial performance and financial risk" [16].

Businesses that weave climate risk management into their ESG frameworks are better equipped to handle both physical disruptions and the challenges of transitioning to a low-carbon economy.

The push for standardized climate disclosures has gained significant momentum, with 89% of investors and 74% of finance leaders advocating for it [16]. Regulatory developments have further cemented this shift. The SEC's climate rules, finalized in March 2024 after reviewing over 24,000 comment letters [4], and the IFRS S1 and S2 standards, effective as of January 1, 2024 [29], have made compliance a necessity rather than an option. Organizations must now view climate alignment as a strategic priority embedded within their broader risk management frameworks.

To navigate this evolving landscape, companies need strong board oversight, frequent materiality assessments, scenario planning to test resilience, and robust data controls led by finance teams. The finance function plays a pivotal role, with 95% of finance leaders acknowledging their teams' importance in ESG reporting [16]. Their expertise in data governance and aggregation ensures that disclosures are accurate and meet the expectations of investors and stakeholders.