Dec 24, 2025

Energy Sector Challenges in Emerging Markets

Sustainability Strategy

In This Article

Why emerging markets lag in clean energy: gaps in access, aging grids, and high financing costs — and the policy, tech, and blended‑finance fixes.

Energy Sector Challenges in Emerging Markets

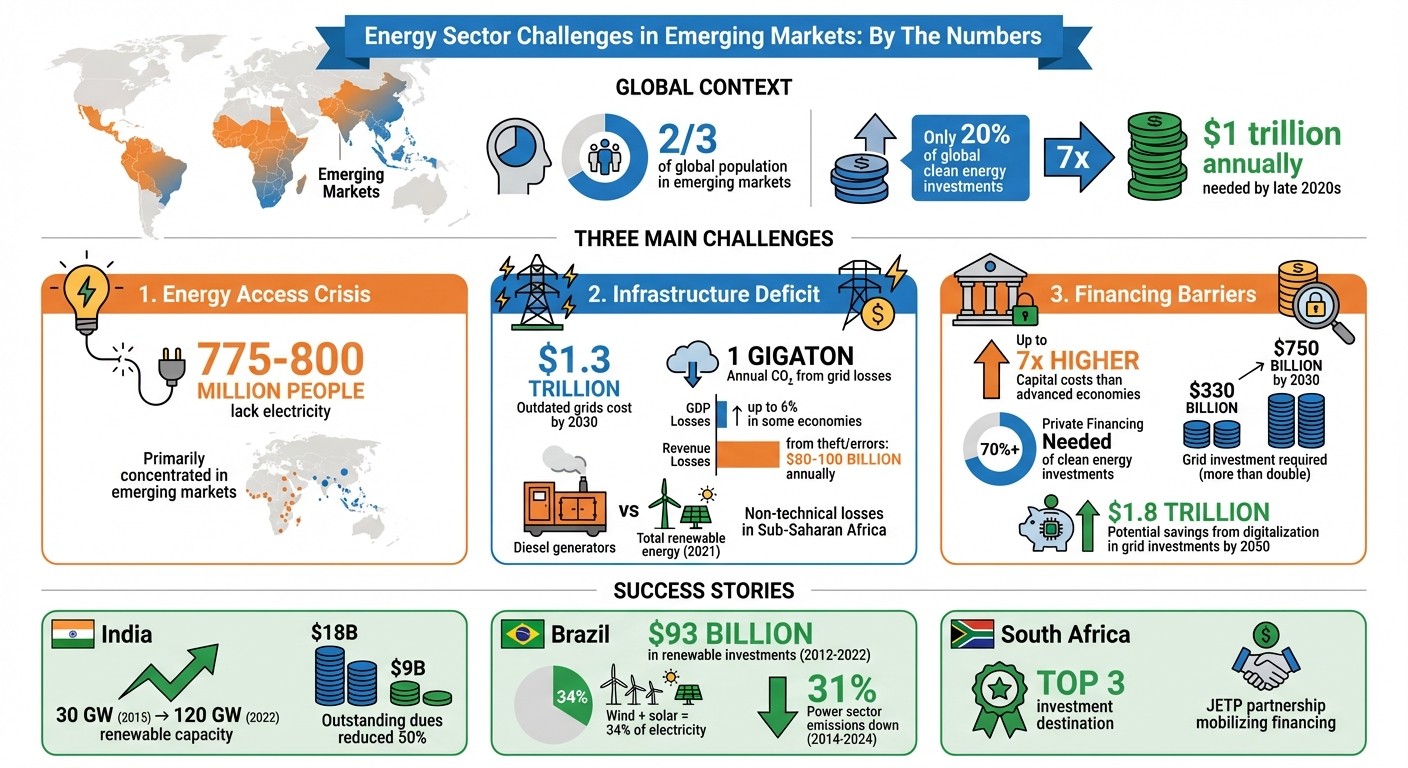

Emerging markets face a daunting energy challenge: balancing growing demand with clean energy transitions. These regions, home to two-thirds of the global population, receive only 20% of global clean energy investments, despite their critical role in combating climate change. Key issues include:

Energy Access: 775–800 million people lack electricity, mainly in these regions.

Outdated Grids: Power outages and inefficiencies cost up to $1.3 trillion by 2030.

High Financing Costs: Clean energy projects are up to 7x more expensive than in advanced economies.

Countries like India, Brazil, and South Africa demonstrate progress through tailored policies, grid upgrades, and financing models. However, achieving energy goals requires $1 trillion annually in investments by the late 2020s, alongside global collaboration and innovative solutions and sustainability consulting.

Key Takeaways:

Investments in infrastructure, grids, and renewables are critical.

Policies addressing financial risks and grid inefficiencies show promise.

International support and private financing are essential for success.

Energy Challenges in Emerging Markets: Key Statistics and Investment Gaps

Main Challenges in Energy Sustainability

Access to Renewable Energy

Emerging markets encounter steep obstacles when it comes to renewable energy development. High capital costs - sometimes up to seven times higher than in the U.S. and Europe - make it difficult to kickstart renewable energy projects that require substantial upfront investments [1].

The situation is further complicated by financially unstable state-owned utilities. Many distribution companies in these markets struggle with insolvency, making them unreliable as buyers for renewable power. To address this, India introduced creditworthy intermediaries in 2021 to bridge the gap between developers and financially weak distribution companies. This move helped reduce revenue risks for large-scale solar and wind projects [1]. Brazil, on the other hand, tackled the issue by implementing competitive procurement auctions and leveraging public financing to lower costs for utility-scale renewable projects. The government also set policies to encourage the growth of distributed solar [1].

Adding to these challenges are fluctuating local currencies and subsidies for fossil fuels, which further erode the competitiveness of renewable energy.

These financial barriers directly affect the readiness of power grids, which is the next hurdle.

Grid Infrastructure Problems

Emerging markets face what experts describe as a "vertical transition." Unlike advanced economies that can replace aging fossil fuel plants within stable grids, these nations must simultaneously build basic grid infrastructure and integrate renewable energy systems [2].

The integration of variable renewables and distributed solar requires advanced capabilities like automated voltage control and bidirectional energy flow - features that most legacy systems simply do not have [2].

The consequences of inadequate infrastructure are significant. Outdated electricity grids result in technical losses that account for roughly 1 gigaton of CO₂ emissions annually [3]. In some emerging economies, unreliable power infrastructure leads to GDP losses as high as 6% [3]. In Sub-Saharan Africa in 2021, diesel-powered backup generators produced more electricity for end-users than the total renewable energy generated in the region. Additionally, non-technical losses, including theft and billing errors, drain $80–$100 billion in annual revenue from utilities [3].

"Low-income countries must add large quantities of renewable energy while rapidly building out grid and distribution infrastructure, grid management capability, workable energy market regulations, and dispatchable capacity to back up intermittent sources like wind and solar." - Mark Thurber and Murefu Barasa [2]

Digitalization offers some hope. Technologies that can detect faults and restore power more quickly could extend the lifespan of grid assets, potentially saving $1.8 trillion in global grid investments [3]. Yet, to meet net-zero targets, annual investments in power grids need to more than double - from about $330 billion today to $750 billion by 2030 [3].

These technical and infrastructure challenges only exacerbate the financial barriers confronting emerging markets.

Investment Gaps and Financing Barriers

The financial challenges don’t stop with capital costs or outdated grids. Emerging markets, which account for two-thirds of the global population, receive just one-fifth of worldwide clean energy investments [1]. To meet net-zero targets, annual clean energy investments in these economies must increase more than sevenfold, surpassing $1 trillion by the late 2020s [1].

The Covid-19 pandemic worsened this situation, straining public finances and leaving many governments with heavy debt burdens. This limits their ability to directly fund or guarantee clean energy projects. As a result, over 70% of clean energy investments in these markets are expected to come from private financing [1]. However, private investors remain cautious without robust measures to mitigate risks.

Kenya provides an example of how targeted reforms can help. The government restructured its debt to fund energy access projects and improve the financial management of its utility sector [1]. Such efforts are critical, as financially stable utilities are essential for ensuring reliable renewable energy purchases.

"The affordability of clean energy transitions will depend on reducing the cost and improving the availability of capital." - IEA [1]

Emerging markets also face unique costs compared to advanced economies. While advanced economies focus on "horizontal transitions" like upgrading existing systems, emerging markets must invest in generation, grid infrastructure, and backup capacity all at once [1]. Despite the higher complexity, the cost of reducing emissions in these economies is roughly half that of advanced economies [1], making them attractive candidates for global climate financing. Yet, the necessary capital remains elusive.

Panel | Driving the Energy Transition in Emerging and Developing Countries

Country-Specific Case Studies

Case studies from India, Brazil, and South Africa showcase how tailored strategies are addressing energy transition challenges.

India: Renewable Energy Policies Driving Progress

India has positioned itself as a leader in renewable energy, setting an ambitious goal of achieving 500 GW of renewable power capacity by 2030, with 50% of its generation capacity coming from non-fossil fuel sources [4].

One of India’s key strategies has been the use of reverse auctions to secure competitive electricity prices. This approach has fueled remarkable growth, with renewable capacity expanding from 30 GW in 2015 to over 120 GW by the end of 2022 [4]. In 2022 alone, solar PV investments reached $15 billion, a significant 50% increase compared to the annual average between 2017 and 2021 [4].

To mitigate credit risks, India established the Solar Energy Corporation of India (SECI). Acting as an intermediary, SECI signs Power Purchase Agreements with developers and Power Sale Agreements with state distribution companies (DISCOMs), backed by a Payment Security Fund [4]. This structure safeguards developers from financial risks tied to utilities.

India has also addressed DISCOM financial struggles through policies like the Late Payment Surcharge (LPS) Rules, which penalize late payments to electricity generators. Between June 2022 and January 2024, this reduced outstanding dues by 50%, from $18 billion to $9 billion [4]. Additionally, the Revamped Distribution Sector Scheme (RDSS) modernized infrastructure, leading to improvements in aggregate technical and commercial (AT&C) losses, which dropped from 22% in 2020/21 to 16% in 2021/22, while payment delays shortened from 175 days to 163 days [4].

"Accelerating the deployment of renewable sources therefore necessitated addressing risks arising from off-taker risk." - IEA [4]

Despite these advancements, challenges persist. The cost of capital for utility-scale solar PV in India remains 80% higher than in advanced economies, influenced by regulatory, currency, and off-taker risks [4]. States like Karnataka and Rajasthan have made strides, with solar and wind contributing 29% and 20% of annual electricity generation, respectively, during fiscal year 2020/21 [5].

Brazil: Diversifying Energy Sources with Wind and Solar

Brazil’s energy strategy highlights the benefits of diversification, transitioning from a hydro-dominated system to one supported by hydro, solar, and wind power [9]. Wind energy alone grew significantly, increasing its share from 8.8% in 2019 to 15% by 2024 [7]. By August 2025, wind and solar together accounted for 34% of Brazil's electricity, with wind contributing 21% [7].

The Brazilian National Development Bank (BNDES) has played a pivotal role by offering low-cost financing for large-scale renewable projects [6][8]. Between 2012 and 2022, Brazil attracted over $93 billion in renewable energy investments, representing more than one-third of all renewable energy investments in emerging markets (excluding China) in 2022 [8].

This diversified energy mix has proven valuable during drought years, allowing hydroelectric reservoirs to conserve water while reducing reliance on costly, high-emission fossil fuels [7][9]. As a result, Brazil’s power sector emissions dropped by 31% between 2014 and 2024, even as electricity demand rose by 22% [7].

"Solar and wind are a perfect match for Brazil's hydropower resources, taking the pressure off in drought years. A diversified mix is a fundamental strategy for tackling risks related to climate change." - Raul Miranda, Global Programme Director, Ember [7]

However, Brazil’s renewable expansion has not been without criticism. Paulo Pedrosa, President of Abrace Energia, has pointed out that "the excess of renewable energy subsidy models has increased the cost of energy and, ironically, promoted the contracting of expensive thermal energy, which is necessary to keep the system balanced when there is no wind and no sun" [9]. To address these challenges, the government has focused on resolving infrastructure bottlenecks through new transmission line auctions and reforms to solar compensation rules [7].

South Africa: Balancing Ambition with Policy Challenges

South Africa’s renewable energy journey has been marked by both progress and setbacks. While the country has mature procurement practices and financing capacity, policy instability, regulatory hurdles, and political risks have created significant obstacles [8]. Retroactive policy changes and the cancellation of clean power procurement auctions have undermined investor confidence [8].

"Despite being a mature renewables market in terms of procurement experience and financing capacity, South Africa faces major energy transition stumbling blocks in its policy instability, regulatory tightness and political risk." - BloombergNEF [8]

Despite these challenges, South Africa was among the top three investment destinations for renewable energy in emerging markets (excluding China) in 2022, alongside Brazil and India [8]. Recent regulatory reforms have unlocked the potential of distributed solar PV, offering a solution to the country’s ongoing power shortages [8].

The Just Energy Transition Partnership (JETP) has emerged as a key initiative, bringing together governments, private sector stakeholders, and multilateral development banks to mobilize financing for a comprehensive energy transition plan [8]. As of December 2023, the program aims to meet ambitious climate goals, contingent on technical and financial support from global partners [8].

"Country platforms [like JETPs] are designed to bring stakeholders together around a comprehensive transition plan and mobilize financing against it, including from the private sector." - BloombergNEF [8]

The most complex issue for South Africa is managing the phase-out of coal-fired power plants, a process that requires transforming utilities and communities heavily reliant on these assets [8]. Experts emphasize that success will depend on extensive collaboration between domestic and international stakeholders to ensure public funds are used effectively to attract private investment [8].

Pathways Toward Sustainable Energy Futures

Energy Planning and Policy Reform

Integrated policy approaches consistently deliver better results than isolated regulations. A study by the IEA examining 11 emerging economies highlights that comprehensive "clean energy innovation ecosystems" are far more effective than simply mandating individual technologies [10]. According to the IEA:

"Government policies play an essential role in clean energy innovation, and it is the combination of a broad range of measures that makes them effective." [10]

Emerging economies are showcasing this principle in action by implementing tailored reforms. Examples include deploying ultra-high voltage (UHV) grids, expanding off-grid solar solutions, and prioritizing energy efficiency [10]. These examples highlight the importance of customizing policies to address unique infrastructure gaps and development goals. Such reforms not only pave the way for collaborative initiatives but also open doors for innovative financing strategies, as explored in later sections.

Stakeholder Collaboration and Systems Thinking

Achieving sustainable energy transitions requires a whole-systems perspective that integrates digital innovations into broader energy and economic frameworks. Governments must align energy, digital, and economic policies to strengthen national innovation systems while fostering collaboration among diverse stakeholders [3].

Council Fire adopts a stakeholder-focused approach, bringing together governments, utilities, private developers, and local communities to craft integrated energy solutions. By applying systems thinking and forming strong partnerships, Council Fire helps organizations move beyond basic compliance, turning ambitious sustainability goals into actionable plans for decarbonization and resilient infrastructure development. These collaborations not only harmonize policies but also drive digital advancements that enhance grid performance and lifespan.

Digital technologies, for instance, can significantly improve grid maintenance, potentially deferring up to $1.8 trillion in global grid investments by 2050 [3]. However, to meet net-zero targets, global grid investments must increase from approximately $330 billion annually to $750 billion by 2030 [3]. Collaborative demonstration projects play a crucial role here, validating business models and reducing risks for future investments, ultimately supporting sustainable energy transitions in emerging markets.

Risk Mitigation and Financing Solutions

Policy reforms and collaboration set the stage, but effective financing strategies are essential to accelerate the energy transition. In emerging and developing economies, annual clean energy investments need to increase more than sevenfold - reaching over $1 trillion by the late 2020s. This challenge is compounded by financing costs that are up to seven times higher than in developed markets [1].

Blended finance has proven to be a viable solution. By leveraging concessional capital, development finance institutions can attract private investment for high-risk projects, such as those targeting remote energy access [1][11]. Countries like India and South Africa have successfully deployed creditworthy intermediaries to lower revenue-related risks for large-scale projects. Similarly, Indonesia, Senegal, and South Africa have used blended finance models to draw in private capital.

The IEA emphasizes the importance of affordable financing:

"The affordability of clean energy transitions will depend on reducing the cost and improving the availability of capital." [1]

Competitive procurement, such as auctions, has also emerged as an effective tool for reducing costs and drawing international developers. Argentina and Brazil have successfully utilized this method, while regions like West Africa and Bangladesh have adopted pay-as-you-go (PAYG) models to finance solar energy and clean cooking technologies. Strengthening domestic banking systems and capital markets to improve access to local-currency debt is another critical step. This is particularly important as over 70% of clean energy investments in emerging markets are expected to come from private financing in climate-driven scenarios [1].

Conclusion

Emerging markets face a steep challenge often referred to as a "vertical transition." This involves building energy grids from scratch, incorporating renewable sources, and ensuring reliable backup systems - all starting from a minimal base of infrastructure [2]. Mark Thurber and Murefu Barasa from the Energy for Growth Hub highlight the complexity of this situation:

Low-income countries... are not likely to be able to leapfrog to a grid that is entirely powered by wind and solar plus energy storage - at least not while also expanding electricity access and driving economic growth [2].

Adding to these technical hurdles are significant financial obstacles. Despite representing two-thirds of the global population, emerging markets attract only one-fifth of clean energy investment. Moreover, financing costs in these regions can be as much as seven times higher than in the United States or Europe [1]. The International Energy Agency (IEA) has issued a stark warning:

If clean energy transitions falter in these countries, this will become the major fault line in global efforts to address climate change [1].

However, the way forward is becoming clearer. Success lies in integrated planning that aligns energy policy with technological innovation and broader economic goals [3]. For instance, smart grid technologies have the potential to save $1.8 trillion in global grid investments by 2050. Meanwhile, blended finance models, which have already shown promise in countries like India, Brazil, and South Africa, offer a practical pathway to tackle financial barriers [1][3]. These solutions, as previously discussed, are crucial for addressing the layered challenges these markets face.

The stakes are immense, extending far beyond climate objectives. In some emerging economies, unreliable energy grids account for economic losses of up to 6% of GDP, with total losses projected to hit $1.3 trillion by 2030 [3]. Bridging these gaps requires collaborative efforts. Organizations like Council Fire play a pivotal role by uniting governments, utilities, developers, and local communities to develop energy strategies that balance financial, environmental, and social goals.

Decisions made in emerging markets will have a profound impact on the global energy landscape. With electricity demand in these regions expected to grow three times faster than in advanced economies [3], coordinated action is not optional - it is essential. By fostering collaboration, leveraging innovative financing, and adopting systems-level strategies, these countries can achieve energy transitions that not only support economic growth but also contribute meaningfully to global climate solutions. The importance of unified energy planning and stakeholder partnerships cannot be overstated in this journey.

FAQs

Why is financing clean energy projects more expensive in emerging markets?

Financing clean energy projects in emerging markets often comes with a hefty price tag due to a range of perceived risks. These include unpredictable policy and regulatory landscapes, underdeveloped local capital markets, and a shortage of renewable energy projects that meet the rigorous standards of bankability. To make matters more complex, developers frequently depend on foreign currency financing, which exposes them to challenges like exchange rate fluctuations and sovereign risk premiums. These factors lead lenders to demand higher interest rates and stricter terms, driving up the overall cost of clean energy investments.

Council Fire plays a pivotal role in addressing these hurdles. They work closely with stakeholders to align project designs with what investors are looking for, enhance policy stability, and create a reliable pipeline of renewable energy projects. By tackling these barriers, they help lower financing costs, paving the way for clean energy investments to be more attainable and financially viable.

How does international collaboration support energy development in emerging markets?

International partnerships are key to helping emerging markets meet their energy objectives. By offering access to technical know-how, funding solutions, and policy guidance, these collaborations pave the way for more reliable and affordable energy systems. Sharing advanced tools like smart-grid technologies and exchanging proven strategies can lead to improved efficiency and lower operational costs. Moreover, working together allows nations to combine resources, modernize grids more effectively, and broaden the reach of renewable energy solutions.

One impactful approach is blended financing, which merges contributions from development banks, private investors, and sovereign funds. This model helps address the high upfront costs often associated with large-scale solar, wind, and energy storage projects. Collaborative efforts also extend to joint research on region-specific renewable technologies and training programs for grid operators, both of which accelerate the shift to clean energy. Through these partnerships, emerging markets can build stronger energy systems while aligning with global climate objectives. Council Fire supports governments and organizations in transforming these international collaborations into practical strategies that balance financial returns with environmental and social progress.

How are digital technologies improving energy grids in emerging markets?

Digital technologies are reshaping energy grids in emerging markets, making them more efficient and dependable. With tools like sensors, advanced metering systems, and automated communication platforms, utilities can now gather real-time data, identify faults quickly, and manage energy supply and demand more effectively. These advancements are especially important for incorporating renewable energy sources like solar and wind while ensuring grid stability.

Through demand-response systems, digital tools also enable appliances in homes and buildings to adjust energy usage during peak periods. This not only eases the strain on the grid but also helps reduce overall energy consumption. Experts project that these improvements could lead to global savings of $1.8 trillion in grid investments by 2050, thanks to better asset management and decreased reliance on backup power.

Council Fire supports organizations in emerging markets by providing strategic guidance, encouraging collaboration, and aligning digital solutions with sustainability objectives. This work accelerates the shift to clean, reliable energy for millions, delivering both financial and environmental advantages.

Related Blog Posts

Latest Articles

©2025

FAQ

01

What does it really mean to “redefine profit”?

02

What makes Council Fire different?

03

Who does Council Fire you work with?

04

What does working with Council Fire actually look like?

05

How does Council Fire help organizations turn big goals into action?

06

How does Council Fire define and measure success?

Dec 24, 2025

Energy Sector Challenges in Emerging Markets

Sustainability Strategy

In This Article

Why emerging markets lag in clean energy: gaps in access, aging grids, and high financing costs — and the policy, tech, and blended‑finance fixes.

Energy Sector Challenges in Emerging Markets

Emerging markets face a daunting energy challenge: balancing growing demand with clean energy transitions. These regions, home to two-thirds of the global population, receive only 20% of global clean energy investments, despite their critical role in combating climate change. Key issues include:

Energy Access: 775–800 million people lack electricity, mainly in these regions.

Outdated Grids: Power outages and inefficiencies cost up to $1.3 trillion by 2030.

High Financing Costs: Clean energy projects are up to 7x more expensive than in advanced economies.

Countries like India, Brazil, and South Africa demonstrate progress through tailored policies, grid upgrades, and financing models. However, achieving energy goals requires $1 trillion annually in investments by the late 2020s, alongside global collaboration and innovative solutions and sustainability consulting.

Key Takeaways:

Investments in infrastructure, grids, and renewables are critical.

Policies addressing financial risks and grid inefficiencies show promise.

International support and private financing are essential for success.

Energy Challenges in Emerging Markets: Key Statistics and Investment Gaps

Main Challenges in Energy Sustainability

Access to Renewable Energy

Emerging markets encounter steep obstacles when it comes to renewable energy development. High capital costs - sometimes up to seven times higher than in the U.S. and Europe - make it difficult to kickstart renewable energy projects that require substantial upfront investments [1].

The situation is further complicated by financially unstable state-owned utilities. Many distribution companies in these markets struggle with insolvency, making them unreliable as buyers for renewable power. To address this, India introduced creditworthy intermediaries in 2021 to bridge the gap between developers and financially weak distribution companies. This move helped reduce revenue risks for large-scale solar and wind projects [1]. Brazil, on the other hand, tackled the issue by implementing competitive procurement auctions and leveraging public financing to lower costs for utility-scale renewable projects. The government also set policies to encourage the growth of distributed solar [1].

Adding to these challenges are fluctuating local currencies and subsidies for fossil fuels, which further erode the competitiveness of renewable energy.

These financial barriers directly affect the readiness of power grids, which is the next hurdle.

Grid Infrastructure Problems

Emerging markets face what experts describe as a "vertical transition." Unlike advanced economies that can replace aging fossil fuel plants within stable grids, these nations must simultaneously build basic grid infrastructure and integrate renewable energy systems [2].

The integration of variable renewables and distributed solar requires advanced capabilities like automated voltage control and bidirectional energy flow - features that most legacy systems simply do not have [2].

The consequences of inadequate infrastructure are significant. Outdated electricity grids result in technical losses that account for roughly 1 gigaton of CO₂ emissions annually [3]. In some emerging economies, unreliable power infrastructure leads to GDP losses as high as 6% [3]. In Sub-Saharan Africa in 2021, diesel-powered backup generators produced more electricity for end-users than the total renewable energy generated in the region. Additionally, non-technical losses, including theft and billing errors, drain $80–$100 billion in annual revenue from utilities [3].

"Low-income countries must add large quantities of renewable energy while rapidly building out grid and distribution infrastructure, grid management capability, workable energy market regulations, and dispatchable capacity to back up intermittent sources like wind and solar." - Mark Thurber and Murefu Barasa [2]

Digitalization offers some hope. Technologies that can detect faults and restore power more quickly could extend the lifespan of grid assets, potentially saving $1.8 trillion in global grid investments [3]. Yet, to meet net-zero targets, annual investments in power grids need to more than double - from about $330 billion today to $750 billion by 2030 [3].

These technical and infrastructure challenges only exacerbate the financial barriers confronting emerging markets.

Investment Gaps and Financing Barriers

The financial challenges don’t stop with capital costs or outdated grids. Emerging markets, which account for two-thirds of the global population, receive just one-fifth of worldwide clean energy investments [1]. To meet net-zero targets, annual clean energy investments in these economies must increase more than sevenfold, surpassing $1 trillion by the late 2020s [1].

The Covid-19 pandemic worsened this situation, straining public finances and leaving many governments with heavy debt burdens. This limits their ability to directly fund or guarantee clean energy projects. As a result, over 70% of clean energy investments in these markets are expected to come from private financing [1]. However, private investors remain cautious without robust measures to mitigate risks.

Kenya provides an example of how targeted reforms can help. The government restructured its debt to fund energy access projects and improve the financial management of its utility sector [1]. Such efforts are critical, as financially stable utilities are essential for ensuring reliable renewable energy purchases.

"The affordability of clean energy transitions will depend on reducing the cost and improving the availability of capital." - IEA [1]

Emerging markets also face unique costs compared to advanced economies. While advanced economies focus on "horizontal transitions" like upgrading existing systems, emerging markets must invest in generation, grid infrastructure, and backup capacity all at once [1]. Despite the higher complexity, the cost of reducing emissions in these economies is roughly half that of advanced economies [1], making them attractive candidates for global climate financing. Yet, the necessary capital remains elusive.

Panel | Driving the Energy Transition in Emerging and Developing Countries

Country-Specific Case Studies

Case studies from India, Brazil, and South Africa showcase how tailored strategies are addressing energy transition challenges.

India: Renewable Energy Policies Driving Progress

India has positioned itself as a leader in renewable energy, setting an ambitious goal of achieving 500 GW of renewable power capacity by 2030, with 50% of its generation capacity coming from non-fossil fuel sources [4].

One of India’s key strategies has been the use of reverse auctions to secure competitive electricity prices. This approach has fueled remarkable growth, with renewable capacity expanding from 30 GW in 2015 to over 120 GW by the end of 2022 [4]. In 2022 alone, solar PV investments reached $15 billion, a significant 50% increase compared to the annual average between 2017 and 2021 [4].

To mitigate credit risks, India established the Solar Energy Corporation of India (SECI). Acting as an intermediary, SECI signs Power Purchase Agreements with developers and Power Sale Agreements with state distribution companies (DISCOMs), backed by a Payment Security Fund [4]. This structure safeguards developers from financial risks tied to utilities.

India has also addressed DISCOM financial struggles through policies like the Late Payment Surcharge (LPS) Rules, which penalize late payments to electricity generators. Between June 2022 and January 2024, this reduced outstanding dues by 50%, from $18 billion to $9 billion [4]. Additionally, the Revamped Distribution Sector Scheme (RDSS) modernized infrastructure, leading to improvements in aggregate technical and commercial (AT&C) losses, which dropped from 22% in 2020/21 to 16% in 2021/22, while payment delays shortened from 175 days to 163 days [4].

"Accelerating the deployment of renewable sources therefore necessitated addressing risks arising from off-taker risk." - IEA [4]

Despite these advancements, challenges persist. The cost of capital for utility-scale solar PV in India remains 80% higher than in advanced economies, influenced by regulatory, currency, and off-taker risks [4]. States like Karnataka and Rajasthan have made strides, with solar and wind contributing 29% and 20% of annual electricity generation, respectively, during fiscal year 2020/21 [5].

Brazil: Diversifying Energy Sources with Wind and Solar

Brazil’s energy strategy highlights the benefits of diversification, transitioning from a hydro-dominated system to one supported by hydro, solar, and wind power [9]. Wind energy alone grew significantly, increasing its share from 8.8% in 2019 to 15% by 2024 [7]. By August 2025, wind and solar together accounted for 34% of Brazil's electricity, with wind contributing 21% [7].

The Brazilian National Development Bank (BNDES) has played a pivotal role by offering low-cost financing for large-scale renewable projects [6][8]. Between 2012 and 2022, Brazil attracted over $93 billion in renewable energy investments, representing more than one-third of all renewable energy investments in emerging markets (excluding China) in 2022 [8].

This diversified energy mix has proven valuable during drought years, allowing hydroelectric reservoirs to conserve water while reducing reliance on costly, high-emission fossil fuels [7][9]. As a result, Brazil’s power sector emissions dropped by 31% between 2014 and 2024, even as electricity demand rose by 22% [7].

"Solar and wind are a perfect match for Brazil's hydropower resources, taking the pressure off in drought years. A diversified mix is a fundamental strategy for tackling risks related to climate change." - Raul Miranda, Global Programme Director, Ember [7]

However, Brazil’s renewable expansion has not been without criticism. Paulo Pedrosa, President of Abrace Energia, has pointed out that "the excess of renewable energy subsidy models has increased the cost of energy and, ironically, promoted the contracting of expensive thermal energy, which is necessary to keep the system balanced when there is no wind and no sun" [9]. To address these challenges, the government has focused on resolving infrastructure bottlenecks through new transmission line auctions and reforms to solar compensation rules [7].

South Africa: Balancing Ambition with Policy Challenges

South Africa’s renewable energy journey has been marked by both progress and setbacks. While the country has mature procurement practices and financing capacity, policy instability, regulatory hurdles, and political risks have created significant obstacles [8]. Retroactive policy changes and the cancellation of clean power procurement auctions have undermined investor confidence [8].

"Despite being a mature renewables market in terms of procurement experience and financing capacity, South Africa faces major energy transition stumbling blocks in its policy instability, regulatory tightness and political risk." - BloombergNEF [8]

Despite these challenges, South Africa was among the top three investment destinations for renewable energy in emerging markets (excluding China) in 2022, alongside Brazil and India [8]. Recent regulatory reforms have unlocked the potential of distributed solar PV, offering a solution to the country’s ongoing power shortages [8].

The Just Energy Transition Partnership (JETP) has emerged as a key initiative, bringing together governments, private sector stakeholders, and multilateral development banks to mobilize financing for a comprehensive energy transition plan [8]. As of December 2023, the program aims to meet ambitious climate goals, contingent on technical and financial support from global partners [8].

"Country platforms [like JETPs] are designed to bring stakeholders together around a comprehensive transition plan and mobilize financing against it, including from the private sector." - BloombergNEF [8]

The most complex issue for South Africa is managing the phase-out of coal-fired power plants, a process that requires transforming utilities and communities heavily reliant on these assets [8]. Experts emphasize that success will depend on extensive collaboration between domestic and international stakeholders to ensure public funds are used effectively to attract private investment [8].

Pathways Toward Sustainable Energy Futures

Energy Planning and Policy Reform

Integrated policy approaches consistently deliver better results than isolated regulations. A study by the IEA examining 11 emerging economies highlights that comprehensive "clean energy innovation ecosystems" are far more effective than simply mandating individual technologies [10]. According to the IEA:

"Government policies play an essential role in clean energy innovation, and it is the combination of a broad range of measures that makes them effective." [10]

Emerging economies are showcasing this principle in action by implementing tailored reforms. Examples include deploying ultra-high voltage (UHV) grids, expanding off-grid solar solutions, and prioritizing energy efficiency [10]. These examples highlight the importance of customizing policies to address unique infrastructure gaps and development goals. Such reforms not only pave the way for collaborative initiatives but also open doors for innovative financing strategies, as explored in later sections.

Stakeholder Collaboration and Systems Thinking

Achieving sustainable energy transitions requires a whole-systems perspective that integrates digital innovations into broader energy and economic frameworks. Governments must align energy, digital, and economic policies to strengthen national innovation systems while fostering collaboration among diverse stakeholders [3].

Council Fire adopts a stakeholder-focused approach, bringing together governments, utilities, private developers, and local communities to craft integrated energy solutions. By applying systems thinking and forming strong partnerships, Council Fire helps organizations move beyond basic compliance, turning ambitious sustainability goals into actionable plans for decarbonization and resilient infrastructure development. These collaborations not only harmonize policies but also drive digital advancements that enhance grid performance and lifespan.

Digital technologies, for instance, can significantly improve grid maintenance, potentially deferring up to $1.8 trillion in global grid investments by 2050 [3]. However, to meet net-zero targets, global grid investments must increase from approximately $330 billion annually to $750 billion by 2030 [3]. Collaborative demonstration projects play a crucial role here, validating business models and reducing risks for future investments, ultimately supporting sustainable energy transitions in emerging markets.

Risk Mitigation and Financing Solutions

Policy reforms and collaboration set the stage, but effective financing strategies are essential to accelerate the energy transition. In emerging and developing economies, annual clean energy investments need to increase more than sevenfold - reaching over $1 trillion by the late 2020s. This challenge is compounded by financing costs that are up to seven times higher than in developed markets [1].

Blended finance has proven to be a viable solution. By leveraging concessional capital, development finance institutions can attract private investment for high-risk projects, such as those targeting remote energy access [1][11]. Countries like India and South Africa have successfully deployed creditworthy intermediaries to lower revenue-related risks for large-scale projects. Similarly, Indonesia, Senegal, and South Africa have used blended finance models to draw in private capital.

The IEA emphasizes the importance of affordable financing:

"The affordability of clean energy transitions will depend on reducing the cost and improving the availability of capital." [1]

Competitive procurement, such as auctions, has also emerged as an effective tool for reducing costs and drawing international developers. Argentina and Brazil have successfully utilized this method, while regions like West Africa and Bangladesh have adopted pay-as-you-go (PAYG) models to finance solar energy and clean cooking technologies. Strengthening domestic banking systems and capital markets to improve access to local-currency debt is another critical step. This is particularly important as over 70% of clean energy investments in emerging markets are expected to come from private financing in climate-driven scenarios [1].

Conclusion

Emerging markets face a steep challenge often referred to as a "vertical transition." This involves building energy grids from scratch, incorporating renewable sources, and ensuring reliable backup systems - all starting from a minimal base of infrastructure [2]. Mark Thurber and Murefu Barasa from the Energy for Growth Hub highlight the complexity of this situation:

Low-income countries... are not likely to be able to leapfrog to a grid that is entirely powered by wind and solar plus energy storage - at least not while also expanding electricity access and driving economic growth [2].

Adding to these technical hurdles are significant financial obstacles. Despite representing two-thirds of the global population, emerging markets attract only one-fifth of clean energy investment. Moreover, financing costs in these regions can be as much as seven times higher than in the United States or Europe [1]. The International Energy Agency (IEA) has issued a stark warning:

If clean energy transitions falter in these countries, this will become the major fault line in global efforts to address climate change [1].

However, the way forward is becoming clearer. Success lies in integrated planning that aligns energy policy with technological innovation and broader economic goals [3]. For instance, smart grid technologies have the potential to save $1.8 trillion in global grid investments by 2050. Meanwhile, blended finance models, which have already shown promise in countries like India, Brazil, and South Africa, offer a practical pathway to tackle financial barriers [1][3]. These solutions, as previously discussed, are crucial for addressing the layered challenges these markets face.

The stakes are immense, extending far beyond climate objectives. In some emerging economies, unreliable energy grids account for economic losses of up to 6% of GDP, with total losses projected to hit $1.3 trillion by 2030 [3]. Bridging these gaps requires collaborative efforts. Organizations like Council Fire play a pivotal role by uniting governments, utilities, developers, and local communities to develop energy strategies that balance financial, environmental, and social goals.

Decisions made in emerging markets will have a profound impact on the global energy landscape. With electricity demand in these regions expected to grow three times faster than in advanced economies [3], coordinated action is not optional - it is essential. By fostering collaboration, leveraging innovative financing, and adopting systems-level strategies, these countries can achieve energy transitions that not only support economic growth but also contribute meaningfully to global climate solutions. The importance of unified energy planning and stakeholder partnerships cannot be overstated in this journey.

FAQs

Why is financing clean energy projects more expensive in emerging markets?

Financing clean energy projects in emerging markets often comes with a hefty price tag due to a range of perceived risks. These include unpredictable policy and regulatory landscapes, underdeveloped local capital markets, and a shortage of renewable energy projects that meet the rigorous standards of bankability. To make matters more complex, developers frequently depend on foreign currency financing, which exposes them to challenges like exchange rate fluctuations and sovereign risk premiums. These factors lead lenders to demand higher interest rates and stricter terms, driving up the overall cost of clean energy investments.

Council Fire plays a pivotal role in addressing these hurdles. They work closely with stakeholders to align project designs with what investors are looking for, enhance policy stability, and create a reliable pipeline of renewable energy projects. By tackling these barriers, they help lower financing costs, paving the way for clean energy investments to be more attainable and financially viable.

How does international collaboration support energy development in emerging markets?

International partnerships are key to helping emerging markets meet their energy objectives. By offering access to technical know-how, funding solutions, and policy guidance, these collaborations pave the way for more reliable and affordable energy systems. Sharing advanced tools like smart-grid technologies and exchanging proven strategies can lead to improved efficiency and lower operational costs. Moreover, working together allows nations to combine resources, modernize grids more effectively, and broaden the reach of renewable energy solutions.

One impactful approach is blended financing, which merges contributions from development banks, private investors, and sovereign funds. This model helps address the high upfront costs often associated with large-scale solar, wind, and energy storage projects. Collaborative efforts also extend to joint research on region-specific renewable technologies and training programs for grid operators, both of which accelerate the shift to clean energy. Through these partnerships, emerging markets can build stronger energy systems while aligning with global climate objectives. Council Fire supports governments and organizations in transforming these international collaborations into practical strategies that balance financial returns with environmental and social progress.

How are digital technologies improving energy grids in emerging markets?

Digital technologies are reshaping energy grids in emerging markets, making them more efficient and dependable. With tools like sensors, advanced metering systems, and automated communication platforms, utilities can now gather real-time data, identify faults quickly, and manage energy supply and demand more effectively. These advancements are especially important for incorporating renewable energy sources like solar and wind while ensuring grid stability.

Through demand-response systems, digital tools also enable appliances in homes and buildings to adjust energy usage during peak periods. This not only eases the strain on the grid but also helps reduce overall energy consumption. Experts project that these improvements could lead to global savings of $1.8 trillion in grid investments by 2050, thanks to better asset management and decreased reliance on backup power.

Council Fire supports organizations in emerging markets by providing strategic guidance, encouraging collaboration, and aligning digital solutions with sustainability objectives. This work accelerates the shift to clean, reliable energy for millions, delivering both financial and environmental advantages.

Related Blog Posts

FAQ

01

What does it really mean to “redefine profit”?

02

What makes Council Fire different?

03

Who does Council Fire you work with?

04

What does working with Council Fire actually look like?

05

How does Council Fire help organizations turn big goals into action?

06

How does Council Fire define and measure success?

Dec 24, 2025

Energy Sector Challenges in Emerging Markets

Sustainability Strategy

In This Article

Why emerging markets lag in clean energy: gaps in access, aging grids, and high financing costs — and the policy, tech, and blended‑finance fixes.

Energy Sector Challenges in Emerging Markets

Emerging markets face a daunting energy challenge: balancing growing demand with clean energy transitions. These regions, home to two-thirds of the global population, receive only 20% of global clean energy investments, despite their critical role in combating climate change. Key issues include:

Energy Access: 775–800 million people lack electricity, mainly in these regions.

Outdated Grids: Power outages and inefficiencies cost up to $1.3 trillion by 2030.

High Financing Costs: Clean energy projects are up to 7x more expensive than in advanced economies.

Countries like India, Brazil, and South Africa demonstrate progress through tailored policies, grid upgrades, and financing models. However, achieving energy goals requires $1 trillion annually in investments by the late 2020s, alongside global collaboration and innovative solutions and sustainability consulting.

Key Takeaways:

Investments in infrastructure, grids, and renewables are critical.

Policies addressing financial risks and grid inefficiencies show promise.

International support and private financing are essential for success.

Energy Challenges in Emerging Markets: Key Statistics and Investment Gaps

Main Challenges in Energy Sustainability

Access to Renewable Energy

Emerging markets encounter steep obstacles when it comes to renewable energy development. High capital costs - sometimes up to seven times higher than in the U.S. and Europe - make it difficult to kickstart renewable energy projects that require substantial upfront investments [1].

The situation is further complicated by financially unstable state-owned utilities. Many distribution companies in these markets struggle with insolvency, making them unreliable as buyers for renewable power. To address this, India introduced creditworthy intermediaries in 2021 to bridge the gap between developers and financially weak distribution companies. This move helped reduce revenue risks for large-scale solar and wind projects [1]. Brazil, on the other hand, tackled the issue by implementing competitive procurement auctions and leveraging public financing to lower costs for utility-scale renewable projects. The government also set policies to encourage the growth of distributed solar [1].

Adding to these challenges are fluctuating local currencies and subsidies for fossil fuels, which further erode the competitiveness of renewable energy.

These financial barriers directly affect the readiness of power grids, which is the next hurdle.

Grid Infrastructure Problems

Emerging markets face what experts describe as a "vertical transition." Unlike advanced economies that can replace aging fossil fuel plants within stable grids, these nations must simultaneously build basic grid infrastructure and integrate renewable energy systems [2].

The integration of variable renewables and distributed solar requires advanced capabilities like automated voltage control and bidirectional energy flow - features that most legacy systems simply do not have [2].

The consequences of inadequate infrastructure are significant. Outdated electricity grids result in technical losses that account for roughly 1 gigaton of CO₂ emissions annually [3]. In some emerging economies, unreliable power infrastructure leads to GDP losses as high as 6% [3]. In Sub-Saharan Africa in 2021, diesel-powered backup generators produced more electricity for end-users than the total renewable energy generated in the region. Additionally, non-technical losses, including theft and billing errors, drain $80–$100 billion in annual revenue from utilities [3].

"Low-income countries must add large quantities of renewable energy while rapidly building out grid and distribution infrastructure, grid management capability, workable energy market regulations, and dispatchable capacity to back up intermittent sources like wind and solar." - Mark Thurber and Murefu Barasa [2]

Digitalization offers some hope. Technologies that can detect faults and restore power more quickly could extend the lifespan of grid assets, potentially saving $1.8 trillion in global grid investments [3]. Yet, to meet net-zero targets, annual investments in power grids need to more than double - from about $330 billion today to $750 billion by 2030 [3].

These technical and infrastructure challenges only exacerbate the financial barriers confronting emerging markets.

Investment Gaps and Financing Barriers

The financial challenges don’t stop with capital costs or outdated grids. Emerging markets, which account for two-thirds of the global population, receive just one-fifth of worldwide clean energy investments [1]. To meet net-zero targets, annual clean energy investments in these economies must increase more than sevenfold, surpassing $1 trillion by the late 2020s [1].

The Covid-19 pandemic worsened this situation, straining public finances and leaving many governments with heavy debt burdens. This limits their ability to directly fund or guarantee clean energy projects. As a result, over 70% of clean energy investments in these markets are expected to come from private financing [1]. However, private investors remain cautious without robust measures to mitigate risks.

Kenya provides an example of how targeted reforms can help. The government restructured its debt to fund energy access projects and improve the financial management of its utility sector [1]. Such efforts are critical, as financially stable utilities are essential for ensuring reliable renewable energy purchases.

"The affordability of clean energy transitions will depend on reducing the cost and improving the availability of capital." - IEA [1]

Emerging markets also face unique costs compared to advanced economies. While advanced economies focus on "horizontal transitions" like upgrading existing systems, emerging markets must invest in generation, grid infrastructure, and backup capacity all at once [1]. Despite the higher complexity, the cost of reducing emissions in these economies is roughly half that of advanced economies [1], making them attractive candidates for global climate financing. Yet, the necessary capital remains elusive.

Panel | Driving the Energy Transition in Emerging and Developing Countries

Country-Specific Case Studies

Case studies from India, Brazil, and South Africa showcase how tailored strategies are addressing energy transition challenges.

India: Renewable Energy Policies Driving Progress

India has positioned itself as a leader in renewable energy, setting an ambitious goal of achieving 500 GW of renewable power capacity by 2030, with 50% of its generation capacity coming from non-fossil fuel sources [4].

One of India’s key strategies has been the use of reverse auctions to secure competitive electricity prices. This approach has fueled remarkable growth, with renewable capacity expanding from 30 GW in 2015 to over 120 GW by the end of 2022 [4]. In 2022 alone, solar PV investments reached $15 billion, a significant 50% increase compared to the annual average between 2017 and 2021 [4].

To mitigate credit risks, India established the Solar Energy Corporation of India (SECI). Acting as an intermediary, SECI signs Power Purchase Agreements with developers and Power Sale Agreements with state distribution companies (DISCOMs), backed by a Payment Security Fund [4]. This structure safeguards developers from financial risks tied to utilities.

India has also addressed DISCOM financial struggles through policies like the Late Payment Surcharge (LPS) Rules, which penalize late payments to electricity generators. Between June 2022 and January 2024, this reduced outstanding dues by 50%, from $18 billion to $9 billion [4]. Additionally, the Revamped Distribution Sector Scheme (RDSS) modernized infrastructure, leading to improvements in aggregate technical and commercial (AT&C) losses, which dropped from 22% in 2020/21 to 16% in 2021/22, while payment delays shortened from 175 days to 163 days [4].

"Accelerating the deployment of renewable sources therefore necessitated addressing risks arising from off-taker risk." - IEA [4]

Despite these advancements, challenges persist. The cost of capital for utility-scale solar PV in India remains 80% higher than in advanced economies, influenced by regulatory, currency, and off-taker risks [4]. States like Karnataka and Rajasthan have made strides, with solar and wind contributing 29% and 20% of annual electricity generation, respectively, during fiscal year 2020/21 [5].

Brazil: Diversifying Energy Sources with Wind and Solar

Brazil’s energy strategy highlights the benefits of diversification, transitioning from a hydro-dominated system to one supported by hydro, solar, and wind power [9]. Wind energy alone grew significantly, increasing its share from 8.8% in 2019 to 15% by 2024 [7]. By August 2025, wind and solar together accounted for 34% of Brazil's electricity, with wind contributing 21% [7].

The Brazilian National Development Bank (BNDES) has played a pivotal role by offering low-cost financing for large-scale renewable projects [6][8]. Between 2012 and 2022, Brazil attracted over $93 billion in renewable energy investments, representing more than one-third of all renewable energy investments in emerging markets (excluding China) in 2022 [8].

This diversified energy mix has proven valuable during drought years, allowing hydroelectric reservoirs to conserve water while reducing reliance on costly, high-emission fossil fuels [7][9]. As a result, Brazil’s power sector emissions dropped by 31% between 2014 and 2024, even as electricity demand rose by 22% [7].

"Solar and wind are a perfect match for Brazil's hydropower resources, taking the pressure off in drought years. A diversified mix is a fundamental strategy for tackling risks related to climate change." - Raul Miranda, Global Programme Director, Ember [7]

However, Brazil’s renewable expansion has not been without criticism. Paulo Pedrosa, President of Abrace Energia, has pointed out that "the excess of renewable energy subsidy models has increased the cost of energy and, ironically, promoted the contracting of expensive thermal energy, which is necessary to keep the system balanced when there is no wind and no sun" [9]. To address these challenges, the government has focused on resolving infrastructure bottlenecks through new transmission line auctions and reforms to solar compensation rules [7].

South Africa: Balancing Ambition with Policy Challenges

South Africa’s renewable energy journey has been marked by both progress and setbacks. While the country has mature procurement practices and financing capacity, policy instability, regulatory hurdles, and political risks have created significant obstacles [8]. Retroactive policy changes and the cancellation of clean power procurement auctions have undermined investor confidence [8].

"Despite being a mature renewables market in terms of procurement experience and financing capacity, South Africa faces major energy transition stumbling blocks in its policy instability, regulatory tightness and political risk." - BloombergNEF [8]

Despite these challenges, South Africa was among the top three investment destinations for renewable energy in emerging markets (excluding China) in 2022, alongside Brazil and India [8]. Recent regulatory reforms have unlocked the potential of distributed solar PV, offering a solution to the country’s ongoing power shortages [8].

The Just Energy Transition Partnership (JETP) has emerged as a key initiative, bringing together governments, private sector stakeholders, and multilateral development banks to mobilize financing for a comprehensive energy transition plan [8]. As of December 2023, the program aims to meet ambitious climate goals, contingent on technical and financial support from global partners [8].

"Country platforms [like JETPs] are designed to bring stakeholders together around a comprehensive transition plan and mobilize financing against it, including from the private sector." - BloombergNEF [8]

The most complex issue for South Africa is managing the phase-out of coal-fired power plants, a process that requires transforming utilities and communities heavily reliant on these assets [8]. Experts emphasize that success will depend on extensive collaboration between domestic and international stakeholders to ensure public funds are used effectively to attract private investment [8].

Pathways Toward Sustainable Energy Futures

Energy Planning and Policy Reform

Integrated policy approaches consistently deliver better results than isolated regulations. A study by the IEA examining 11 emerging economies highlights that comprehensive "clean energy innovation ecosystems" are far more effective than simply mandating individual technologies [10]. According to the IEA:

"Government policies play an essential role in clean energy innovation, and it is the combination of a broad range of measures that makes them effective." [10]

Emerging economies are showcasing this principle in action by implementing tailored reforms. Examples include deploying ultra-high voltage (UHV) grids, expanding off-grid solar solutions, and prioritizing energy efficiency [10]. These examples highlight the importance of customizing policies to address unique infrastructure gaps and development goals. Such reforms not only pave the way for collaborative initiatives but also open doors for innovative financing strategies, as explored in later sections.

Stakeholder Collaboration and Systems Thinking

Achieving sustainable energy transitions requires a whole-systems perspective that integrates digital innovations into broader energy and economic frameworks. Governments must align energy, digital, and economic policies to strengthen national innovation systems while fostering collaboration among diverse stakeholders [3].

Council Fire adopts a stakeholder-focused approach, bringing together governments, utilities, private developers, and local communities to craft integrated energy solutions. By applying systems thinking and forming strong partnerships, Council Fire helps organizations move beyond basic compliance, turning ambitious sustainability goals into actionable plans for decarbonization and resilient infrastructure development. These collaborations not only harmonize policies but also drive digital advancements that enhance grid performance and lifespan.

Digital technologies, for instance, can significantly improve grid maintenance, potentially deferring up to $1.8 trillion in global grid investments by 2050 [3]. However, to meet net-zero targets, global grid investments must increase from approximately $330 billion annually to $750 billion by 2030 [3]. Collaborative demonstration projects play a crucial role here, validating business models and reducing risks for future investments, ultimately supporting sustainable energy transitions in emerging markets.

Risk Mitigation and Financing Solutions

Policy reforms and collaboration set the stage, but effective financing strategies are essential to accelerate the energy transition. In emerging and developing economies, annual clean energy investments need to increase more than sevenfold - reaching over $1 trillion by the late 2020s. This challenge is compounded by financing costs that are up to seven times higher than in developed markets [1].

Blended finance has proven to be a viable solution. By leveraging concessional capital, development finance institutions can attract private investment for high-risk projects, such as those targeting remote energy access [1][11]. Countries like India and South Africa have successfully deployed creditworthy intermediaries to lower revenue-related risks for large-scale projects. Similarly, Indonesia, Senegal, and South Africa have used blended finance models to draw in private capital.

The IEA emphasizes the importance of affordable financing:

"The affordability of clean energy transitions will depend on reducing the cost and improving the availability of capital." [1]

Competitive procurement, such as auctions, has also emerged as an effective tool for reducing costs and drawing international developers. Argentina and Brazil have successfully utilized this method, while regions like West Africa and Bangladesh have adopted pay-as-you-go (PAYG) models to finance solar energy and clean cooking technologies. Strengthening domestic banking systems and capital markets to improve access to local-currency debt is another critical step. This is particularly important as over 70% of clean energy investments in emerging markets are expected to come from private financing in climate-driven scenarios [1].

Conclusion

Emerging markets face a steep challenge often referred to as a "vertical transition." This involves building energy grids from scratch, incorporating renewable sources, and ensuring reliable backup systems - all starting from a minimal base of infrastructure [2]. Mark Thurber and Murefu Barasa from the Energy for Growth Hub highlight the complexity of this situation:

Low-income countries... are not likely to be able to leapfrog to a grid that is entirely powered by wind and solar plus energy storage - at least not while also expanding electricity access and driving economic growth [2].

Adding to these technical hurdles are significant financial obstacles. Despite representing two-thirds of the global population, emerging markets attract only one-fifth of clean energy investment. Moreover, financing costs in these regions can be as much as seven times higher than in the United States or Europe [1]. The International Energy Agency (IEA) has issued a stark warning:

If clean energy transitions falter in these countries, this will become the major fault line in global efforts to address climate change [1].

However, the way forward is becoming clearer. Success lies in integrated planning that aligns energy policy with technological innovation and broader economic goals [3]. For instance, smart grid technologies have the potential to save $1.8 trillion in global grid investments by 2050. Meanwhile, blended finance models, which have already shown promise in countries like India, Brazil, and South Africa, offer a practical pathway to tackle financial barriers [1][3]. These solutions, as previously discussed, are crucial for addressing the layered challenges these markets face.

The stakes are immense, extending far beyond climate objectives. In some emerging economies, unreliable energy grids account for economic losses of up to 6% of GDP, with total losses projected to hit $1.3 trillion by 2030 [3]. Bridging these gaps requires collaborative efforts. Organizations like Council Fire play a pivotal role by uniting governments, utilities, developers, and local communities to develop energy strategies that balance financial, environmental, and social goals.

Decisions made in emerging markets will have a profound impact on the global energy landscape. With electricity demand in these regions expected to grow three times faster than in advanced economies [3], coordinated action is not optional - it is essential. By fostering collaboration, leveraging innovative financing, and adopting systems-level strategies, these countries can achieve energy transitions that not only support economic growth but also contribute meaningfully to global climate solutions. The importance of unified energy planning and stakeholder partnerships cannot be overstated in this journey.

FAQs

Why is financing clean energy projects more expensive in emerging markets?

Financing clean energy projects in emerging markets often comes with a hefty price tag due to a range of perceived risks. These include unpredictable policy and regulatory landscapes, underdeveloped local capital markets, and a shortage of renewable energy projects that meet the rigorous standards of bankability. To make matters more complex, developers frequently depend on foreign currency financing, which exposes them to challenges like exchange rate fluctuations and sovereign risk premiums. These factors lead lenders to demand higher interest rates and stricter terms, driving up the overall cost of clean energy investments.

Council Fire plays a pivotal role in addressing these hurdles. They work closely with stakeholders to align project designs with what investors are looking for, enhance policy stability, and create a reliable pipeline of renewable energy projects. By tackling these barriers, they help lower financing costs, paving the way for clean energy investments to be more attainable and financially viable.

How does international collaboration support energy development in emerging markets?

International partnerships are key to helping emerging markets meet their energy objectives. By offering access to technical know-how, funding solutions, and policy guidance, these collaborations pave the way for more reliable and affordable energy systems. Sharing advanced tools like smart-grid technologies and exchanging proven strategies can lead to improved efficiency and lower operational costs. Moreover, working together allows nations to combine resources, modernize grids more effectively, and broaden the reach of renewable energy solutions.

One impactful approach is blended financing, which merges contributions from development banks, private investors, and sovereign funds. This model helps address the high upfront costs often associated with large-scale solar, wind, and energy storage projects. Collaborative efforts also extend to joint research on region-specific renewable technologies and training programs for grid operators, both of which accelerate the shift to clean energy. Through these partnerships, emerging markets can build stronger energy systems while aligning with global climate objectives. Council Fire supports governments and organizations in transforming these international collaborations into practical strategies that balance financial returns with environmental and social progress.

How are digital technologies improving energy grids in emerging markets?

Digital technologies are reshaping energy grids in emerging markets, making them more efficient and dependable. With tools like sensors, advanced metering systems, and automated communication platforms, utilities can now gather real-time data, identify faults quickly, and manage energy supply and demand more effectively. These advancements are especially important for incorporating renewable energy sources like solar and wind while ensuring grid stability.

Through demand-response systems, digital tools also enable appliances in homes and buildings to adjust energy usage during peak periods. This not only eases the strain on the grid but also helps reduce overall energy consumption. Experts project that these improvements could lead to global savings of $1.8 trillion in grid investments by 2050, thanks to better asset management and decreased reliance on backup power.

Council Fire supports organizations in emerging markets by providing strategic guidance, encouraging collaboration, and aligning digital solutions with sustainability objectives. This work accelerates the shift to clean, reliable energy for millions, delivering both financial and environmental advantages.

Related Blog Posts

FAQ

What does it really mean to “redefine profit”?

What makes Council Fire different?

Who does Council Fire you work with?

What does working with Council Fire actually look like?

How does Council Fire help organizations turn big goals into action?

How does Council Fire define and measure success?