Jul 8, 2026

AU vs. NZ ESG Policies: Key Differences

ESG Strategy

In This Article

Compare AU and NZ mandatory climate disclosure: timing, scope, standards, Scope 3, liability, and cross‑border compliance needs.

AU vs. NZ ESG Policies: Key Differences

If you work across Australia and New Zealand, I’d treat Australia as the tougher reporting base. New Zealand started first on 1/1/2023, but its rules cover only about 172 entities. Australia started later on 1/1/2025, yet its phased model is set to pull in 6,000+ entities by 2030 and asks for more disclosure detail.

Here’s the short version:

New Zealand moved first

Climate reporting applies from 1/1/2023

Focus is on listed issuers, banks, insurers, and investment managers

Regime is based on TCFD-style standards

Australia came later but reaches more companies

Climate reporting starts from 1/1/2025

Covers many listed and private entities through phased size tests

Rules align with IFRS S2 and include more disclosure points

The two systems do not match

A company outside New Zealand’s regime may still need to support an Australian entity

Scope 3 data requests can move across supplier and group lines

There is no mutual recognition, so one filing does not cover both markets

Liability is different

Australia gives a 3-year modified liability period for some forward-looking climate statements

New Zealand applies full director liability from the start

Both systems are climate-focused, not full ESG mandates , requiring organizations to prioritize climate resilience

Australia makes AASB S2 mandatory, while AASB S1 stays voluntary

New Zealand uses NZ CS 1–3 for climate statements

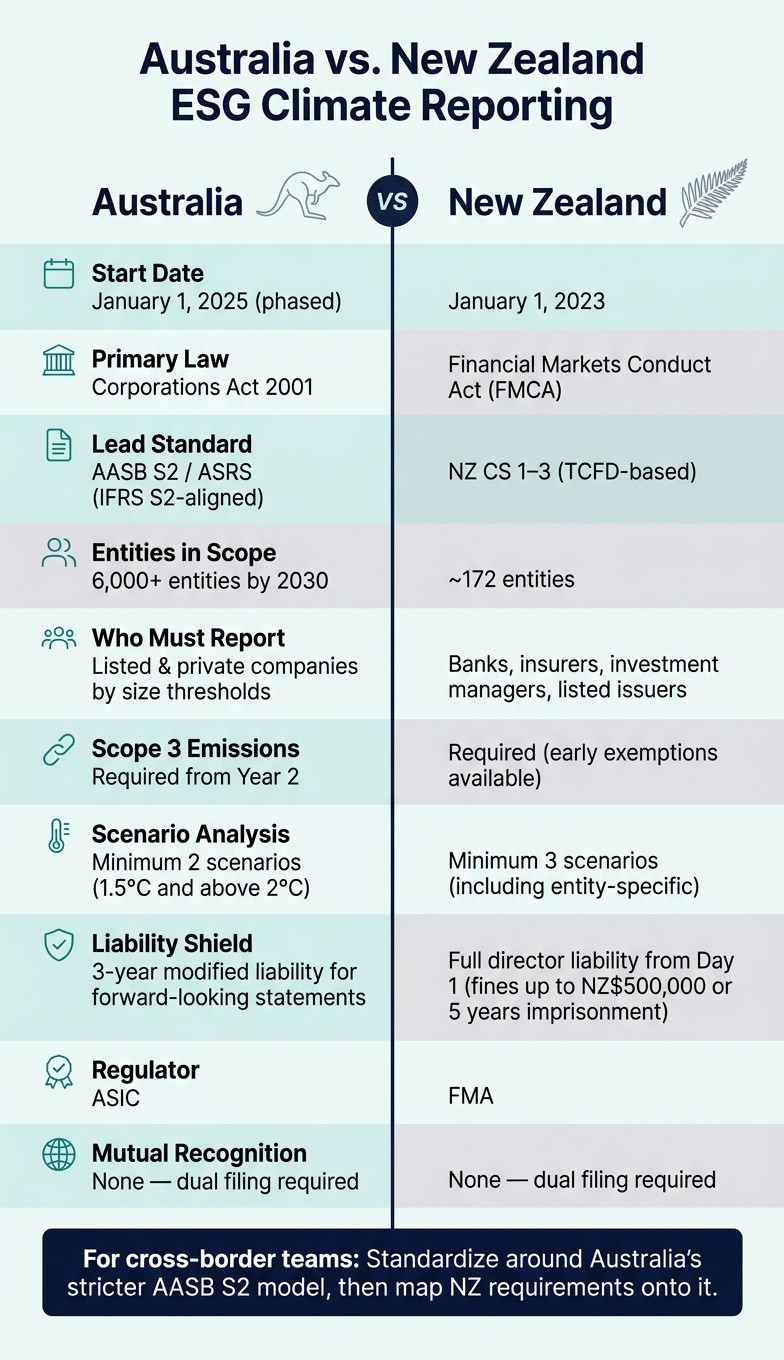

Australia vs. New Zealand ESG Climate Reporting: Key Differences at a Glance

Mandatory climate reporting in Australia: what Group 2 companies need to know for ASRS readiness

Quick Comparison

Topic | Australia | New Zealand |

|---|---|---|

Start date | 1/1/2025 | 1/1/2023 |

Main framework | AASB S2 / ASRS | NZ CS 1–3 |

Base model | IFRS S2-aligned | TCFD-based |

Scope | Many listed and private entities by size | Defined financial-sector and listed entities |

Estimated entities in scope | 6,000+ by 2030 | About 172 |

Scope 3 | Starts in year 2 | Required, with some early exemptions |

Scenario analysis | At least 2 scenarios | At least 3 scenarios |

Liability | Modified shield for some disclosures for 3 years | No comparable shield |

I see the core difference this way: New Zealand is earlier and narrower; Australia is later, broader, and more detailed. If you report in both places, you need dual planning, shared data controls, and clear board sign-off.

Australia ESG policies: corporate disclosure rules and phased mandatory climate reporting

Australia’s ESG framework sits across a set of separate laws, and the new mandatory reporting track is focused on climate.

Core ESG laws and governance expectations in Australia

Australia’s ESG duties are not housed in one single statute. Instead, they sit across separate laws, each aimed at a different compliance area. The Corporations Act 2001, the National Greenhouse and Energy Reporting (NGER) Act 2007, the Modern Slavery Act 2018, the Workplace Gender Equality Act 2012, and the ASX Corporate Governance Principles each form part of that structure. [5]

These rules run side by side. Each has its own subject matter, thresholds, and regulator. That split setup matters because it helps explain why Australia’s next move did not become a broad mandatory ESG system all at once.

ASRS and AASB S2: Australia's climate disclosure rollout

Australia’s mandatory regime is limited to climate-related financial disclosures. Under the Australian Sustainability Reporting Standards (ASRS), AASB S2 requires in-scope entities to submit a sustainability report alongside their annual financial report under the Corporations Act. [5]

By contrast, AASB S1 - the standard for broader sustainability-related disclosures - remains voluntary. In plain terms, the binding rule is climate-focused, not full ESG reporting. [5]

AASB S2 follows four pillars:

Governance

Strategy

Risk Management

Metrics and Targets

Entities must report Scope 1 and Scope 2 emissions from their first reporting year. Scope 3 emissions come in from the second year onward. Scenario analysis must use at least two temperature pathways: 1.5°C and above 2°C. [5]

The rollout is phased by entity size:

Reporting Group | Commencement Date | Size Thresholds (2 of 3 required) |

|---|---|---|

Group 1 | FY starting on or after January 1, 2025 | Revenue ≥ $500 million; Assets ≥ $1 billion; Employees ≥ 500 |

Group 2 | FY starting on or after July 1, 2026 | Revenue ≥ $200 million; Assets ≥ $500 million; Employees ≥ 250 |

Group 3 | FY starting on or after July 1, 2027 | Revenue ≥ $50 million; Assets ≥ $25 million; Employees ≥ 100 |

Group 3 entities report only where climate risks or opportunities are material.

Enforcement and compliance risk in Australia

ASIC is the main regulator overseeing this regime, and it treats RG 280 as the key implementation guide. [5]

ASIC has also made clear that greenwashing is a live enforcement issue. The message is simple: climate claims need data behind them, and that data must hold up under review. [5]

The regime also builds in a three-year limited immunity period for protected statements, including Scope 3 emissions, scenario analysis, and transition plans. During that period, entities are shielded from private civil litigation tied to those disclosures, but ASIC still keeps its enforcement powers. Directors, for the first three years, only need to declare that the entity took "reasonable steps" to comply. Sustainability records must be kept for seven years. [5]

New Zealand’s regime takes a different path: earlier, narrower, and built around a smaller group of defined entities.

New Zealand ESG policies: early mandatory climate reporting for defined entities

New Zealand moved earlier than Australia on mandatory climate reporting, but its system is much tighter in scope. Australia’s phased model is set to cover more than 6,000 entities by 2030. New Zealand, by contrast, applies the rules to a defined group of financial-sector participants and listed issuers, not the whole economy. That keeps the regime targeted rather than broad-based. [1][6]

The legal basis for mandatory climate statements in New Zealand

New Zealand’s mandatory climate-statement regime sits under the Financial Sector (Climate-related Disclosures and Other Matters) Amendment Act 2021, which amended the Financial Markets Conduct Act 2013. Under that law, designated Climate Reporting Entities (CREs) must file annual climate statements for periods beginning on or after Jan. 1, 2023. [6]

Those climate statements must be public. For reporting years ending on or after Oct. 27, 2024, entities must also obtain independent assurance for GHG emissions disclosures. [6]

Aotearoa New Zealand Climate Standards and who must report

The disclosure framework comes from the NZ Climate Standards (NZ CS 1–3), issued by the External Reporting Board (XRB). One point stands out right away: NZ CS 1 requires scenario analysis across at least three climate scenarios - a 1.5°C scenario, a 3°C or greater scenario, and a third scenario tied to the entity’s own context. Australia’s AASB S2 asks for only two. [1]

Reporting applies only to certain financial and listed entities:

Entity Type | Reporting Threshold |

|---|---|

Banks, credit unions, and building societies | Total assets > $1 billion |

Managers of registered investment schemes | Assets under management > $1 billion |

Licensed insurers | Total assets > $1 billion or annual premium income > $250 million |

Listed equity issuers | Market capitalization > $60 million |

Listed debt issuers | Face value of quoted debt > $60 million |

Large private companies outside the financial sector are generally left out. That’s a clear contrast with Australia’s broader size-based model. [1]

Oversight and reporting expectations in New Zealand

The Financial Markets Authority oversees compliance and has leaned toward education as it rolls the regime out. Even so, the penalties are not light. Directors can face fines of up to NZ$500,000 or five years’ imprisonment for failing to prepare climate statements, and New Zealand does not offer a modified liability shield for forward-looking statements. [1][2]

The aim is to make climate risk a normal part of business, investment, lending, and insurance decisions, often requiring sustainability consulting to navigate these complex regulatory shifts. In plain terms, the rules may apply to a narrower group, but for the entities inside the system, the reporting duty carries real weight.

Australia vs. New Zealand ESG policies: key differences

Both regimes make climate risk something companies must report, but the two systems part ways on scope, rollout, and legal exposure. In plain terms, Australia casts a much wider net and rolls in by phases, while New Zealand covers a smaller set of entities and is already in force.

Feature | Australia | New Zealand |

|---|---|---|

Primary law | Corporations Act 2001 [1] | Financial Markets Conduct Act (FMCA) [1] |

Lead standard setter | External Reporting Board (XRB) [1] | |

Entities in scope | Listed and unlisted public/private companies meeting size thresholds; NGER reporters [1] | Large NZX-listed issuers, banks, insurers, and managed investment scheme managers, about 172 entities [1] |

Start date | Phased from Jan. 1, 2025 [1] | |

Coverage beyond climate | Mandatory climate disclosure under AASB S2; AASB S1 provides a voluntary general sustainability standard [1] | Climate-related disclosures under NZ CS 1, 2, and 3 [1] |

Emissions disclosures | Scope 1, 2, and 3; initial Scope 3 exemptions are available [1] | |

Enforcement approach | ASIC; three-year modified liability period for Scope 3 and scenario analysis [1] |

Regulatory design, scope, and timing

Australia places climate disclosure inside annual corporate reporting. New Zealand, by contrast, uses a narrower FMCA-based model aimed at a defined group of entities. The scale gap is hard to miss: by 2030, Australia expects more than 6,000 entities in scope, while New Zealand covers about 172 [1].

That changes the day-to-day workload. In Australia, many more companies will need reporting systems, review processes, and board oversight. In New Zealand, the pool is smaller, but the rules are already live, so covered entities have less room to wait and see.

Climate-only mandates versus broader ESG expectations

Australia’s mandatory system is still climate-only. AASB S2 is required, while AASB S1 serves as a voluntary general sustainability standard [1]. New Zealand also stays focused on climate through NZ CS 1, 2, and 3 [1].

So despite the way people often group these topics under the ESG label, the required disclosures in both markets are not a full ESG package. They are centered on climate, not the whole set of social and governance topics.

What the differences mean for multinational compliance teams

For cross-border compliance teams, the hard part is not just filing on time. It’s building one reporting process that can handle two systems built from different starting points. AASB S2 aligns with IFRS S2, while New Zealand’s standards were built from TCFD recommendations [1][2].

Liability is another big dividing line. Australia gives companies a three-year modified liability period for Scope 3 emissions and scenario analysis, which gives teams some room as they build data processes [1][2][4]. New Zealand takes a firmer line: directors face full liability right away [1][4].

There’s also a supply-chain angle that matters in practice. A New Zealand company may fall outside the Climate Reporting Entity, or CRE, regime and still get pulled into the process if it supplies an Australian company that needs upstream GHG data for Scope 3 reporting [3][4]. That can shift reporting work across borders, even when the legal duty sits somewhere else.

For many teams, that means the job is less about one clean policy and more about clear ownership:

Who collects emissions data

Who reviews assumptions and scenario inputs

Who signs off at the entity and board level

Those design choices tend to shape reporting calendars, internal controls, and how risk gets divided between finance, legal, and sustainability teams.

Conclusion: Key takeaways from the Australia vs. New Zealand comparison

New Zealand moved first with a narrower, TCFD-based regime. Australia came later with a broader, phased model aligned to IFRS S2.

The main point is straightforward: both countries require climate disclosure, and neither country has put a full ESG reporting mandate in place. In both markets, the rules stay focused on climate rather than covering the whole ESG landscape.

For multinational teams, the simplest path is to standardize around the stricter Australian model. For cross-border teams, AASB S2 sets the higher bar, so it makes sense to use it as the baseline and then map New Zealand requirements onto it. Since there is no mutual recognition between the two regimes, companies working in both jurisdictions still need to plan for dual compliance [3].

That shift from rulebook to day-to-day execution comes down to data, governance, and clear accountability. Council Fire helps organizations turn climate disclosure into practical decarbonization and resilience action.

FAQs

Which companies are most likely to be in scope in Australia but not in New Zealand?

Australia’s climate disclosure regime casts a much wider net than New Zealand’s. That difference matters.

New Zealand’s rules mainly center on a narrower group: certain financial institutions, licensed insurers, banks, and listed issuers. Australia goes further. It also brings in large non-financial and private companies that meet size thresholds under the Corporations Act 2001.

In plain terms, that means many large private entities and non-financial institutions that may be exempt in New Zealand could still have to comply in Australia. For companies operating across both markets, the gap isn’t minor - it can change who falls inside the reporting perimeter and who doesn’t.

How should multinational teams handle dual compliance across both countries?

Multinational teams need to follow the main legislation in both jurisdictions. There’s no mutual recognition between the Australian and New Zealand regimes, so meeting the rules in one country does not mean you’re covered in the other.

Since both frameworks are built on TCFD recommendations, the smartest move is to use a centralized climate data and governance model. From there, teams can adjust disclosures, formats, and timing to match each country’s rules and reporting deadlines.

Starting with New Zealand standards can be a practical base, but it also means getting ready for Australia’s added requirements, including the Greenhouse Gas Protocol.

What practical steps are needed for Scope 3 reporting?

Move past spreadsheets and take a more structured approach. Bring your supply chain into the process early, work directly with material suppliers, and record your assumptions clearly so the audit trail holds up under review.

You’ll also need solid systems to handle complex, high-volume data without the whole process turning into a mess. Established standards such as the GHG Protocol Corporate Accounting Standard and ISO 14064-1:2018 can help you set boundaries and pick measurement methods with more consistency.

Related Blog Posts

Latest Articles

©2025

FAQ

01

What does it really mean to “redefine profit”?

02

What makes Council Fire different?

03

Who does Council Fire you work with?

04

What does working with Council Fire actually look like?

05

How does Council Fire help organizations turn big goals into action?

06

How does Council Fire define and measure success?

Jul 8, 2026

AU vs. NZ ESG Policies: Key Differences

ESG Strategy

In This Article

Compare AU and NZ mandatory climate disclosure: timing, scope, standards, Scope 3, liability, and cross‑border compliance needs.

AU vs. NZ ESG Policies: Key Differences

If you work across Australia and New Zealand, I’d treat Australia as the tougher reporting base. New Zealand started first on 1/1/2023, but its rules cover only about 172 entities. Australia started later on 1/1/2025, yet its phased model is set to pull in 6,000+ entities by 2030 and asks for more disclosure detail.

Here’s the short version:

New Zealand moved first

Climate reporting applies from 1/1/2023

Focus is on listed issuers, banks, insurers, and investment managers

Regime is based on TCFD-style standards

Australia came later but reaches more companies

Climate reporting starts from 1/1/2025

Covers many listed and private entities through phased size tests

Rules align with IFRS S2 and include more disclosure points

The two systems do not match

A company outside New Zealand’s regime may still need to support an Australian entity

Scope 3 data requests can move across supplier and group lines

There is no mutual recognition, so one filing does not cover both markets

Liability is different

Australia gives a 3-year modified liability period for some forward-looking climate statements

New Zealand applies full director liability from the start

Both systems are climate-focused, not full ESG mandates , requiring organizations to prioritize climate resilience

Australia makes AASB S2 mandatory, while AASB S1 stays voluntary

New Zealand uses NZ CS 1–3 for climate statements

Australia vs. New Zealand ESG Climate Reporting: Key Differences at a Glance

Mandatory climate reporting in Australia: what Group 2 companies need to know for ASRS readiness

Quick Comparison

Topic | Australia | New Zealand |

|---|---|---|

Start date | 1/1/2025 | 1/1/2023 |

Main framework | AASB S2 / ASRS | NZ CS 1–3 |

Base model | IFRS S2-aligned | TCFD-based |

Scope | Many listed and private entities by size | Defined financial-sector and listed entities |

Estimated entities in scope | 6,000+ by 2030 | About 172 |

Scope 3 | Starts in year 2 | Required, with some early exemptions |

Scenario analysis | At least 2 scenarios | At least 3 scenarios |

Liability | Modified shield for some disclosures for 3 years | No comparable shield |

I see the core difference this way: New Zealand is earlier and narrower; Australia is later, broader, and more detailed. If you report in both places, you need dual planning, shared data controls, and clear board sign-off.

Australia ESG policies: corporate disclosure rules and phased mandatory climate reporting

Australia’s ESG framework sits across a set of separate laws, and the new mandatory reporting track is focused on climate.

Core ESG laws and governance expectations in Australia

Australia’s ESG duties are not housed in one single statute. Instead, they sit across separate laws, each aimed at a different compliance area. The Corporations Act 2001, the National Greenhouse and Energy Reporting (NGER) Act 2007, the Modern Slavery Act 2018, the Workplace Gender Equality Act 2012, and the ASX Corporate Governance Principles each form part of that structure. [5]

These rules run side by side. Each has its own subject matter, thresholds, and regulator. That split setup matters because it helps explain why Australia’s next move did not become a broad mandatory ESG system all at once.

ASRS and AASB S2: Australia's climate disclosure rollout

Australia’s mandatory regime is limited to climate-related financial disclosures. Under the Australian Sustainability Reporting Standards (ASRS), AASB S2 requires in-scope entities to submit a sustainability report alongside their annual financial report under the Corporations Act. [5]

By contrast, AASB S1 - the standard for broader sustainability-related disclosures - remains voluntary. In plain terms, the binding rule is climate-focused, not full ESG reporting. [5]

AASB S2 follows four pillars:

Governance

Strategy

Risk Management

Metrics and Targets

Entities must report Scope 1 and Scope 2 emissions from their first reporting year. Scope 3 emissions come in from the second year onward. Scenario analysis must use at least two temperature pathways: 1.5°C and above 2°C. [5]

The rollout is phased by entity size:

Reporting Group | Commencement Date | Size Thresholds (2 of 3 required) |

|---|---|---|

Group 1 | FY starting on or after January 1, 2025 | Revenue ≥ $500 million; Assets ≥ $1 billion; Employees ≥ 500 |

Group 2 | FY starting on or after July 1, 2026 | Revenue ≥ $200 million; Assets ≥ $500 million; Employees ≥ 250 |

Group 3 | FY starting on or after July 1, 2027 | Revenue ≥ $50 million; Assets ≥ $25 million; Employees ≥ 100 |

Group 3 entities report only where climate risks or opportunities are material.

Enforcement and compliance risk in Australia

ASIC is the main regulator overseeing this regime, and it treats RG 280 as the key implementation guide. [5]

ASIC has also made clear that greenwashing is a live enforcement issue. The message is simple: climate claims need data behind them, and that data must hold up under review. [5]

The regime also builds in a three-year limited immunity period for protected statements, including Scope 3 emissions, scenario analysis, and transition plans. During that period, entities are shielded from private civil litigation tied to those disclosures, but ASIC still keeps its enforcement powers. Directors, for the first three years, only need to declare that the entity took "reasonable steps" to comply. Sustainability records must be kept for seven years. [5]

New Zealand’s regime takes a different path: earlier, narrower, and built around a smaller group of defined entities.

New Zealand ESG policies: early mandatory climate reporting for defined entities

New Zealand moved earlier than Australia on mandatory climate reporting, but its system is much tighter in scope. Australia’s phased model is set to cover more than 6,000 entities by 2030. New Zealand, by contrast, applies the rules to a defined group of financial-sector participants and listed issuers, not the whole economy. That keeps the regime targeted rather than broad-based. [1][6]

The legal basis for mandatory climate statements in New Zealand

New Zealand’s mandatory climate-statement regime sits under the Financial Sector (Climate-related Disclosures and Other Matters) Amendment Act 2021, which amended the Financial Markets Conduct Act 2013. Under that law, designated Climate Reporting Entities (CREs) must file annual climate statements for periods beginning on or after Jan. 1, 2023. [6]

Those climate statements must be public. For reporting years ending on or after Oct. 27, 2024, entities must also obtain independent assurance for GHG emissions disclosures. [6]

Aotearoa New Zealand Climate Standards and who must report

The disclosure framework comes from the NZ Climate Standards (NZ CS 1–3), issued by the External Reporting Board (XRB). One point stands out right away: NZ CS 1 requires scenario analysis across at least three climate scenarios - a 1.5°C scenario, a 3°C or greater scenario, and a third scenario tied to the entity’s own context. Australia’s AASB S2 asks for only two. [1]

Reporting applies only to certain financial and listed entities:

Entity Type | Reporting Threshold |

|---|---|

Banks, credit unions, and building societies | Total assets > $1 billion |

Managers of registered investment schemes | Assets under management > $1 billion |

Licensed insurers | Total assets > $1 billion or annual premium income > $250 million |

Listed equity issuers | Market capitalization > $60 million |

Listed debt issuers | Face value of quoted debt > $60 million |

Large private companies outside the financial sector are generally left out. That’s a clear contrast with Australia’s broader size-based model. [1]

Oversight and reporting expectations in New Zealand

The Financial Markets Authority oversees compliance and has leaned toward education as it rolls the regime out. Even so, the penalties are not light. Directors can face fines of up to NZ$500,000 or five years’ imprisonment for failing to prepare climate statements, and New Zealand does not offer a modified liability shield for forward-looking statements. [1][2]

The aim is to make climate risk a normal part of business, investment, lending, and insurance decisions, often requiring sustainability consulting to navigate these complex regulatory shifts. In plain terms, the rules may apply to a narrower group, but for the entities inside the system, the reporting duty carries real weight.

Australia vs. New Zealand ESG policies: key differences

Both regimes make climate risk something companies must report, but the two systems part ways on scope, rollout, and legal exposure. In plain terms, Australia casts a much wider net and rolls in by phases, while New Zealand covers a smaller set of entities and is already in force.

Feature | Australia | New Zealand |

|---|---|---|

Primary law | Corporations Act 2001 [1] | Financial Markets Conduct Act (FMCA) [1] |

Lead standard setter | External Reporting Board (XRB) [1] | |

Entities in scope | Listed and unlisted public/private companies meeting size thresholds; NGER reporters [1] | Large NZX-listed issuers, banks, insurers, and managed investment scheme managers, about 172 entities [1] |

Start date | Phased from Jan. 1, 2025 [1] | |

Coverage beyond climate | Mandatory climate disclosure under AASB S2; AASB S1 provides a voluntary general sustainability standard [1] | Climate-related disclosures under NZ CS 1, 2, and 3 [1] |

Emissions disclosures | Scope 1, 2, and 3; initial Scope 3 exemptions are available [1] | |

Enforcement approach | ASIC; three-year modified liability period for Scope 3 and scenario analysis [1] |

Regulatory design, scope, and timing

Australia places climate disclosure inside annual corporate reporting. New Zealand, by contrast, uses a narrower FMCA-based model aimed at a defined group of entities. The scale gap is hard to miss: by 2030, Australia expects more than 6,000 entities in scope, while New Zealand covers about 172 [1].

That changes the day-to-day workload. In Australia, many more companies will need reporting systems, review processes, and board oversight. In New Zealand, the pool is smaller, but the rules are already live, so covered entities have less room to wait and see.

Climate-only mandates versus broader ESG expectations

Australia’s mandatory system is still climate-only. AASB S2 is required, while AASB S1 serves as a voluntary general sustainability standard [1]. New Zealand also stays focused on climate through NZ CS 1, 2, and 3 [1].

So despite the way people often group these topics under the ESG label, the required disclosures in both markets are not a full ESG package. They are centered on climate, not the whole set of social and governance topics.

What the differences mean for multinational compliance teams

For cross-border compliance teams, the hard part is not just filing on time. It’s building one reporting process that can handle two systems built from different starting points. AASB S2 aligns with IFRS S2, while New Zealand’s standards were built from TCFD recommendations [1][2].

Liability is another big dividing line. Australia gives companies a three-year modified liability period for Scope 3 emissions and scenario analysis, which gives teams some room as they build data processes [1][2][4]. New Zealand takes a firmer line: directors face full liability right away [1][4].

There’s also a supply-chain angle that matters in practice. A New Zealand company may fall outside the Climate Reporting Entity, or CRE, regime and still get pulled into the process if it supplies an Australian company that needs upstream GHG data for Scope 3 reporting [3][4]. That can shift reporting work across borders, even when the legal duty sits somewhere else.

For many teams, that means the job is less about one clean policy and more about clear ownership:

Who collects emissions data

Who reviews assumptions and scenario inputs

Who signs off at the entity and board level

Those design choices tend to shape reporting calendars, internal controls, and how risk gets divided between finance, legal, and sustainability teams.

Conclusion: Key takeaways from the Australia vs. New Zealand comparison

New Zealand moved first with a narrower, TCFD-based regime. Australia came later with a broader, phased model aligned to IFRS S2.

The main point is straightforward: both countries require climate disclosure, and neither country has put a full ESG reporting mandate in place. In both markets, the rules stay focused on climate rather than covering the whole ESG landscape.

For multinational teams, the simplest path is to standardize around the stricter Australian model. For cross-border teams, AASB S2 sets the higher bar, so it makes sense to use it as the baseline and then map New Zealand requirements onto it. Since there is no mutual recognition between the two regimes, companies working in both jurisdictions still need to plan for dual compliance [3].

That shift from rulebook to day-to-day execution comes down to data, governance, and clear accountability. Council Fire helps organizations turn climate disclosure into practical decarbonization and resilience action.

FAQs

Which companies are most likely to be in scope in Australia but not in New Zealand?

Australia’s climate disclosure regime casts a much wider net than New Zealand’s. That difference matters.

New Zealand’s rules mainly center on a narrower group: certain financial institutions, licensed insurers, banks, and listed issuers. Australia goes further. It also brings in large non-financial and private companies that meet size thresholds under the Corporations Act 2001.

In plain terms, that means many large private entities and non-financial institutions that may be exempt in New Zealand could still have to comply in Australia. For companies operating across both markets, the gap isn’t minor - it can change who falls inside the reporting perimeter and who doesn’t.

How should multinational teams handle dual compliance across both countries?

Multinational teams need to follow the main legislation in both jurisdictions. There’s no mutual recognition between the Australian and New Zealand regimes, so meeting the rules in one country does not mean you’re covered in the other.

Since both frameworks are built on TCFD recommendations, the smartest move is to use a centralized climate data and governance model. From there, teams can adjust disclosures, formats, and timing to match each country’s rules and reporting deadlines.

Starting with New Zealand standards can be a practical base, but it also means getting ready for Australia’s added requirements, including the Greenhouse Gas Protocol.

What practical steps are needed for Scope 3 reporting?

Move past spreadsheets and take a more structured approach. Bring your supply chain into the process early, work directly with material suppliers, and record your assumptions clearly so the audit trail holds up under review.

You’ll also need solid systems to handle complex, high-volume data without the whole process turning into a mess. Established standards such as the GHG Protocol Corporate Accounting Standard and ISO 14064-1:2018 can help you set boundaries and pick measurement methods with more consistency.

Related Blog Posts

FAQ

01

What does it really mean to “redefine profit”?

02

What makes Council Fire different?

03

Who does Council Fire you work with?

04

What does working with Council Fire actually look like?

05

How does Council Fire help organizations turn big goals into action?

06

How does Council Fire define and measure success?

Jul 8, 2026

AU vs. NZ ESG Policies: Key Differences

ESG Strategy

In This Article

Compare AU and NZ mandatory climate disclosure: timing, scope, standards, Scope 3, liability, and cross‑border compliance needs.

AU vs. NZ ESG Policies: Key Differences

If you work across Australia and New Zealand, I’d treat Australia as the tougher reporting base. New Zealand started first on 1/1/2023, but its rules cover only about 172 entities. Australia started later on 1/1/2025, yet its phased model is set to pull in 6,000+ entities by 2030 and asks for more disclosure detail.

Here’s the short version:

New Zealand moved first

Climate reporting applies from 1/1/2023

Focus is on listed issuers, banks, insurers, and investment managers

Regime is based on TCFD-style standards

Australia came later but reaches more companies

Climate reporting starts from 1/1/2025

Covers many listed and private entities through phased size tests

Rules align with IFRS S2 and include more disclosure points

The two systems do not match

A company outside New Zealand’s regime may still need to support an Australian entity

Scope 3 data requests can move across supplier and group lines

There is no mutual recognition, so one filing does not cover both markets

Liability is different

Australia gives a 3-year modified liability period for some forward-looking climate statements

New Zealand applies full director liability from the start

Both systems are climate-focused, not full ESG mandates , requiring organizations to prioritize climate resilience

Australia makes AASB S2 mandatory, while AASB S1 stays voluntary

New Zealand uses NZ CS 1–3 for climate statements

Australia vs. New Zealand ESG Climate Reporting: Key Differences at a Glance

Mandatory climate reporting in Australia: what Group 2 companies need to know for ASRS readiness

Quick Comparison

Topic | Australia | New Zealand |

|---|---|---|

Start date | 1/1/2025 | 1/1/2023 |

Main framework | AASB S2 / ASRS | NZ CS 1–3 |

Base model | IFRS S2-aligned | TCFD-based |

Scope | Many listed and private entities by size | Defined financial-sector and listed entities |

Estimated entities in scope | 6,000+ by 2030 | About 172 |

Scope 3 | Starts in year 2 | Required, with some early exemptions |

Scenario analysis | At least 2 scenarios | At least 3 scenarios |

Liability | Modified shield for some disclosures for 3 years | No comparable shield |

I see the core difference this way: New Zealand is earlier and narrower; Australia is later, broader, and more detailed. If you report in both places, you need dual planning, shared data controls, and clear board sign-off.

Australia ESG policies: corporate disclosure rules and phased mandatory climate reporting

Australia’s ESG framework sits across a set of separate laws, and the new mandatory reporting track is focused on climate.

Core ESG laws and governance expectations in Australia

Australia’s ESG duties are not housed in one single statute. Instead, they sit across separate laws, each aimed at a different compliance area. The Corporations Act 2001, the National Greenhouse and Energy Reporting (NGER) Act 2007, the Modern Slavery Act 2018, the Workplace Gender Equality Act 2012, and the ASX Corporate Governance Principles each form part of that structure. [5]

These rules run side by side. Each has its own subject matter, thresholds, and regulator. That split setup matters because it helps explain why Australia’s next move did not become a broad mandatory ESG system all at once.

ASRS and AASB S2: Australia's climate disclosure rollout

Australia’s mandatory regime is limited to climate-related financial disclosures. Under the Australian Sustainability Reporting Standards (ASRS), AASB S2 requires in-scope entities to submit a sustainability report alongside their annual financial report under the Corporations Act. [5]

By contrast, AASB S1 - the standard for broader sustainability-related disclosures - remains voluntary. In plain terms, the binding rule is climate-focused, not full ESG reporting. [5]

AASB S2 follows four pillars:

Governance

Strategy

Risk Management

Metrics and Targets

Entities must report Scope 1 and Scope 2 emissions from their first reporting year. Scope 3 emissions come in from the second year onward. Scenario analysis must use at least two temperature pathways: 1.5°C and above 2°C. [5]

The rollout is phased by entity size:

Reporting Group | Commencement Date | Size Thresholds (2 of 3 required) |

|---|---|---|

Group 1 | FY starting on or after January 1, 2025 | Revenue ≥ $500 million; Assets ≥ $1 billion; Employees ≥ 500 |

Group 2 | FY starting on or after July 1, 2026 | Revenue ≥ $200 million; Assets ≥ $500 million; Employees ≥ 250 |

Group 3 | FY starting on or after July 1, 2027 | Revenue ≥ $50 million; Assets ≥ $25 million; Employees ≥ 100 |

Group 3 entities report only where climate risks or opportunities are material.

Enforcement and compliance risk in Australia

ASIC is the main regulator overseeing this regime, and it treats RG 280 as the key implementation guide. [5]

ASIC has also made clear that greenwashing is a live enforcement issue. The message is simple: climate claims need data behind them, and that data must hold up under review. [5]

The regime also builds in a three-year limited immunity period for protected statements, including Scope 3 emissions, scenario analysis, and transition plans. During that period, entities are shielded from private civil litigation tied to those disclosures, but ASIC still keeps its enforcement powers. Directors, for the first three years, only need to declare that the entity took "reasonable steps" to comply. Sustainability records must be kept for seven years. [5]

New Zealand’s regime takes a different path: earlier, narrower, and built around a smaller group of defined entities.

New Zealand ESG policies: early mandatory climate reporting for defined entities

New Zealand moved earlier than Australia on mandatory climate reporting, but its system is much tighter in scope. Australia’s phased model is set to cover more than 6,000 entities by 2030. New Zealand, by contrast, applies the rules to a defined group of financial-sector participants and listed issuers, not the whole economy. That keeps the regime targeted rather than broad-based. [1][6]

The legal basis for mandatory climate statements in New Zealand

New Zealand’s mandatory climate-statement regime sits under the Financial Sector (Climate-related Disclosures and Other Matters) Amendment Act 2021, which amended the Financial Markets Conduct Act 2013. Under that law, designated Climate Reporting Entities (CREs) must file annual climate statements for periods beginning on or after Jan. 1, 2023. [6]

Those climate statements must be public. For reporting years ending on or after Oct. 27, 2024, entities must also obtain independent assurance for GHG emissions disclosures. [6]

Aotearoa New Zealand Climate Standards and who must report

The disclosure framework comes from the NZ Climate Standards (NZ CS 1–3), issued by the External Reporting Board (XRB). One point stands out right away: NZ CS 1 requires scenario analysis across at least three climate scenarios - a 1.5°C scenario, a 3°C or greater scenario, and a third scenario tied to the entity’s own context. Australia’s AASB S2 asks for only two. [1]

Reporting applies only to certain financial and listed entities:

Entity Type | Reporting Threshold |

|---|---|

Banks, credit unions, and building societies | Total assets > $1 billion |

Managers of registered investment schemes | Assets under management > $1 billion |

Licensed insurers | Total assets > $1 billion or annual premium income > $250 million |

Listed equity issuers | Market capitalization > $60 million |

Listed debt issuers | Face value of quoted debt > $60 million |

Large private companies outside the financial sector are generally left out. That’s a clear contrast with Australia’s broader size-based model. [1]

Oversight and reporting expectations in New Zealand

The Financial Markets Authority oversees compliance and has leaned toward education as it rolls the regime out. Even so, the penalties are not light. Directors can face fines of up to NZ$500,000 or five years’ imprisonment for failing to prepare climate statements, and New Zealand does not offer a modified liability shield for forward-looking statements. [1][2]

The aim is to make climate risk a normal part of business, investment, lending, and insurance decisions, often requiring sustainability consulting to navigate these complex regulatory shifts. In plain terms, the rules may apply to a narrower group, but for the entities inside the system, the reporting duty carries real weight.

Australia vs. New Zealand ESG policies: key differences

Both regimes make climate risk something companies must report, but the two systems part ways on scope, rollout, and legal exposure. In plain terms, Australia casts a much wider net and rolls in by phases, while New Zealand covers a smaller set of entities and is already in force.

Feature | Australia | New Zealand |

|---|---|---|

Primary law | Corporations Act 2001 [1] | Financial Markets Conduct Act (FMCA) [1] |

Lead standard setter | External Reporting Board (XRB) [1] | |

Entities in scope | Listed and unlisted public/private companies meeting size thresholds; NGER reporters [1] | Large NZX-listed issuers, banks, insurers, and managed investment scheme managers, about 172 entities [1] |

Start date | Phased from Jan. 1, 2025 [1] | |

Coverage beyond climate | Mandatory climate disclosure under AASB S2; AASB S1 provides a voluntary general sustainability standard [1] | Climate-related disclosures under NZ CS 1, 2, and 3 [1] |

Emissions disclosures | Scope 1, 2, and 3; initial Scope 3 exemptions are available [1] | |

Enforcement approach | ASIC; three-year modified liability period for Scope 3 and scenario analysis [1] |

Regulatory design, scope, and timing

Australia places climate disclosure inside annual corporate reporting. New Zealand, by contrast, uses a narrower FMCA-based model aimed at a defined group of entities. The scale gap is hard to miss: by 2030, Australia expects more than 6,000 entities in scope, while New Zealand covers about 172 [1].

That changes the day-to-day workload. In Australia, many more companies will need reporting systems, review processes, and board oversight. In New Zealand, the pool is smaller, but the rules are already live, so covered entities have less room to wait and see.

Climate-only mandates versus broader ESG expectations

Australia’s mandatory system is still climate-only. AASB S2 is required, while AASB S1 serves as a voluntary general sustainability standard [1]. New Zealand also stays focused on climate through NZ CS 1, 2, and 3 [1].

So despite the way people often group these topics under the ESG label, the required disclosures in both markets are not a full ESG package. They are centered on climate, not the whole set of social and governance topics.

What the differences mean for multinational compliance teams

For cross-border compliance teams, the hard part is not just filing on time. It’s building one reporting process that can handle two systems built from different starting points. AASB S2 aligns with IFRS S2, while New Zealand’s standards were built from TCFD recommendations [1][2].

Liability is another big dividing line. Australia gives companies a three-year modified liability period for Scope 3 emissions and scenario analysis, which gives teams some room as they build data processes [1][2][4]. New Zealand takes a firmer line: directors face full liability right away [1][4].

There’s also a supply-chain angle that matters in practice. A New Zealand company may fall outside the Climate Reporting Entity, or CRE, regime and still get pulled into the process if it supplies an Australian company that needs upstream GHG data for Scope 3 reporting [3][4]. That can shift reporting work across borders, even when the legal duty sits somewhere else.

For many teams, that means the job is less about one clean policy and more about clear ownership:

Who collects emissions data

Who reviews assumptions and scenario inputs

Who signs off at the entity and board level

Those design choices tend to shape reporting calendars, internal controls, and how risk gets divided between finance, legal, and sustainability teams.

Conclusion: Key takeaways from the Australia vs. New Zealand comparison

New Zealand moved first with a narrower, TCFD-based regime. Australia came later with a broader, phased model aligned to IFRS S2.

The main point is straightforward: both countries require climate disclosure, and neither country has put a full ESG reporting mandate in place. In both markets, the rules stay focused on climate rather than covering the whole ESG landscape.

For multinational teams, the simplest path is to standardize around the stricter Australian model. For cross-border teams, AASB S2 sets the higher bar, so it makes sense to use it as the baseline and then map New Zealand requirements onto it. Since there is no mutual recognition between the two regimes, companies working in both jurisdictions still need to plan for dual compliance [3].

That shift from rulebook to day-to-day execution comes down to data, governance, and clear accountability. Council Fire helps organizations turn climate disclosure into practical decarbonization and resilience action.

FAQs

Which companies are most likely to be in scope in Australia but not in New Zealand?

Australia’s climate disclosure regime casts a much wider net than New Zealand’s. That difference matters.

New Zealand’s rules mainly center on a narrower group: certain financial institutions, licensed insurers, banks, and listed issuers. Australia goes further. It also brings in large non-financial and private companies that meet size thresholds under the Corporations Act 2001.

In plain terms, that means many large private entities and non-financial institutions that may be exempt in New Zealand could still have to comply in Australia. For companies operating across both markets, the gap isn’t minor - it can change who falls inside the reporting perimeter and who doesn’t.

How should multinational teams handle dual compliance across both countries?

Multinational teams need to follow the main legislation in both jurisdictions. There’s no mutual recognition between the Australian and New Zealand regimes, so meeting the rules in one country does not mean you’re covered in the other.

Since both frameworks are built on TCFD recommendations, the smartest move is to use a centralized climate data and governance model. From there, teams can adjust disclosures, formats, and timing to match each country’s rules and reporting deadlines.

Starting with New Zealand standards can be a practical base, but it also means getting ready for Australia’s added requirements, including the Greenhouse Gas Protocol.

What practical steps are needed for Scope 3 reporting?

Move past spreadsheets and take a more structured approach. Bring your supply chain into the process early, work directly with material suppliers, and record your assumptions clearly so the audit trail holds up under review.

You’ll also need solid systems to handle complex, high-volume data without the whole process turning into a mess. Established standards such as the GHG Protocol Corporate Accounting Standard and ISO 14064-1:2018 can help you set boundaries and pick measurement methods with more consistency.

Related Blog Posts

FAQ

What does it really mean to “redefine profit”?

What makes Council Fire different?

Who does Council Fire you work with?

What does working with Council Fire actually look like?

How does Council Fire help organizations turn big goals into action?

How does Council Fire define and measure success?