Mar 20, 2026

How to Develop a Blue Economy Strategy for Corporations

Sustainability Strategy

In This Article

Practical guide for corporations to build a Blue Economy strategy: assess ocean impacts, set SMART goals, adopt circular practices, and secure blue finance.

How to Develop a Blue Economy Strategy for Corporations

The Blue Economy focuses on the responsible use of ocean and water resources to drive economic growth while protecting ecosystems. With a global value of $2.5 trillion annually, it ranks as one of the largest economic sectors. Corporations can benefit from this growing market by aligning their operations with sustainability principles, addressing risks like climate change, and exploring opportunities in marine industries.

Key Steps for Corporations:

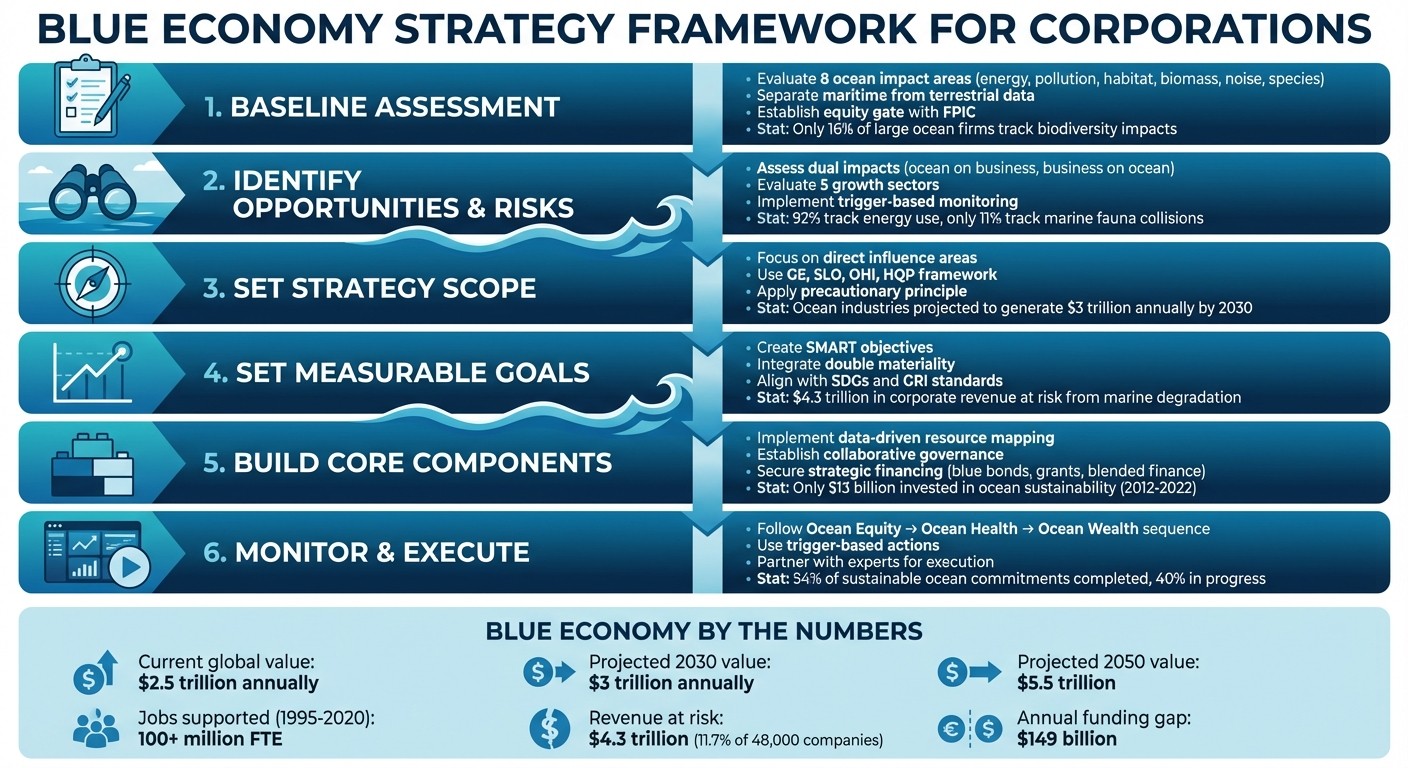

Baseline Assessment: Evaluate impacts across energy use, pollution, habitat changes, and biodiversity.

Engage Stakeholders: Secure community consent and ensure equitable practices.

Set Measurable Goals: Use SMART objectives tied to ocean health and UN SDGs.

Adopt Circular Practices: Reduce waste and create value from marine byproducts.

Leverage Data: Use advanced tools like Marine Spatial Planning and real-time monitoring.

Secure Financing: Explore blue bonds, grants, and blended finance options.

With ocean-based industries projected to generate over $3 trillion annually by 2030, transitioning to a sustainable model is both a business opportunity and a necessity. Companies must act now to balance profitability with the preservation of marine ecosystems.

6-Step Blue Economy Strategy Framework for Corporations

Rethinking Ocean Finance: Innovative Strategies for a Sustainable Blue Economy

Evaluating Your Company's Blue Economy Readiness

Assess how your company interacts with ocean ecosystems while aligning with principles of equity, environmental health, and sustainable economic growth.

Conducting a Baseline Assessment

Begin with the Blue Economy Development Approach (BEDA), which emphasizes a step-by-step progression: Ocean Equity → Ocean Health → Ocean Wealth [8]. This sequence ensures that social and environmental priorities are addressed before focusing on economic outcomes.

To create a comprehensive baseline, evaluate your operations across eight critical ocean impact areas, which go far beyond standard carbon reporting. These include energy use, pollution (solid waste, wastewater, hazardous substances, plastic), habitat changes, biomass extraction, noise pollution, and the introduction of non-native species [10]. A review of 75 major ocean-economy firms revealed the use of 443 different indicators to measure environmental impacts. However, fewer than 25% of these metrics specifically addressed ocean-related concerns beyond energy and greenhouse gas emissions [10].

Separate maritime data from terrestrial data, including emissions, waste, and water usage, to pinpoint marine-specific liabilities [10]. While 92% of large ocean firms track energy use, only 16% of their metrics cover biodiversity impacts, and just 7% measure or set targets for habitat alteration [10].

Establish an equity gate by obtaining Free, Prior, and Informed Consent (FPIC) from local and Indigenous communities. Ensure transparent benefit-sharing agreements are in place [8]. Use stakeholder mapping to assess your Social License to Operate (SLO), gauging the level of ongoing community acceptance for your operations [9].

Lawrence M. Mak and colleagues in Frontiers in Marine Science caution: "Equity-blind ocean policies can back-fire even when they are environmentally ambitious" [8].

Incorporate the "Two-Eyed Seeing" approach by combining scientific indicators, such as biodiversity scores, with Indigenous and local knowledge, like seasonal species patterns. This dual perspective enhances your understanding of environmental risks, as traditional knowledge often identifies ecosystem changes that scientific methods may overlook [8].

Utilize the Blue Economy Capacity Framework (BECF) to highlight gaps in four key areas: Gender Equity (GE), Social License to Operate (SLO), Ocean Health Investment (OHI), and Highly Qualified Personnel (HQP) [9]. Align these findings with relevant UN Sustainable Development Goals (SDGs), such as SDG 14.2 (ecosystem protection) and SDG 5.5 (gender equity), adapting them to your company’s specific needs [9].

With a solid baseline in place, you can assess how your operational impacts translate into risks and opportunities within the blue economy.

Identifying Opportunities and Risks

Once you’ve established a baseline, examine the interplay between how ocean health affects your business and how your business affects the ocean [10]. This dual perspective helps you identify vulnerabilities and environmental liabilities tied to your activities.

The blue economy offers growth opportunities in five key sectors: marine transportation, ocean exploration, seafood competitiveness, tourism and recreation, and coastal resilience [11]. By 2050, the sustainable ocean economy is expected to reach a market value of $5.5 trillion [3]. Between 1995 and 2020, it supported over 100 million full-time equivalent jobs globally [3].

Regulatory risks are also evolving. The Kunming-Montreal Global Biodiversity Framework (Target 15) now mandates large transnational companies to disclose biodiversity risks and impacts [10]. Additionally, the Ocean Investment Protocol, introduced in July 2025, provides actionable steps for aligning business practices with ocean health goals [3].

Implement trigger-based monitoring systems that incorporate environmental health thresholds informed by both scientific and traditional knowledge. Set "stop rules" or corrective actions to address any breaches of these thresholds [8]. This proactive approach minimizes the risk of minor issues escalating into significant environmental or regulatory challenges.

Jessica Smith and Suzanne Johnson from the UN Environment Programme Finance Initiative emphasize: "The blue economy links ocean health with prosperity, making targeted finance more urgent than ever" [3].

While most companies track energy use (92%) and pollution (92%), impacts such as noise (33%) and collisions with marine fauna (11%) are often overlooked [10]. Considering that the ocean has absorbed over 90% of the excess heat generated by human activity and about 25% of carbon dioxide emissions in the past 50 years [3], climate resilience must be a key focus for ocean-dependent businesses.

Setting Strategy Scope and Objectives

After assessing your baseline and identifying risks, it's time to craft a strategy that reflects your company’s tangible impact on marine ecosystems. This involves narrowing your focus to specific marine activities, regions, and stakeholder groups where meaningful change is possible. The goal is to move beyond the traditional "ocean economy" mindset, which prioritizes revenue, to embrace a blue economy approach that integrates social and environmental considerations [9].

Your strategy should focus on areas where your company has direct influence. For instance, if your operations affect local coastal fisheries, your goals should target those ecosystems rather than broader, less actionable goals like "improving ocean health." Avoid relying entirely on government mandates; instead, focus on what your business can achieve independently [9].

To shape your strategy, use the core focus areas identified in your baseline - GE, SLO, OHI, and HQP - as a framework [9]. This structure helps balance economic growth with environmental and social responsibilities. With ocean-based industries expected to generate over $3 trillion annually by 2030 [2], defining clear boundaries and realistic objectives is essential.

Incorporate the precautionary principle to mitigate risks associated with uncertain environmental impacts [12]. Once your scope is defined, the next step is to establish measurable objectives that drive actionable results.

Setting Measurable Goals

To ensure accountability, set SMART goals - Specific, Measurable, Achievable, Relevant, and Time-bound. Vague statements like “improve ocean health” lack clarity and impact. Instead, focus on specific targets, such as reducing wastewater discharge by 30% by December 31, 2030, or achieving 40% women’s representation in marine leadership roles by December 31, 2028.

Integrate double materiality to evaluate both the impact of your business on the ocean and how ocean health affects your financial performance [15]. Studies show that $4.3 trillion in corporate revenue - 11.7% of the total revenue from 48,000 companies - faces risks from marine ecosystem degradation [15]. This dual perspective helps identify priorities that align environmental preservation with financial stability.

Align your goals with established frameworks like the Global Reporting Initiative (GRI) for impact materiality, SASB for financial materiality, and TCFD for climate-related financial risks. Use the Blue Economy Capacity Assessment Framework (BECF) to translate UN Sustainable Development Goals (SDGs) into actionable company-level objectives. For example:

SDG Target | Blue Economy Industry Aim | Corporate Action Example |

|---|---|---|

5.5 & 16.7 | Gender Equity | Ensure women’s full participation in marine operations leadership |

1.4, 8.4, 11.7, 12.6 | Social License to Operate | Adopt sustainable reporting and ensure equitable access to ocean resources |

14.2 & 6.6 | Ocean Health Investment | Restore marine ecosystems and manage water quality impacts |

4.7 & 10.4 | Highly Qualified Personnel | Provide ocean literacy training and equitable wage policies |

Setting science-based targets with realistic timelines adds credibility to your strategy. While the 100 largest companies in the blue economy generated $1.1 trillion in revenue in 2018, only $13 billion was invested in ocean sustainability between 2012 and 2022 [2]. Bridging this funding gap requires deliberate commitments, such as allocating capital to marine conservation and restoration projects.

"Joining the Ocean 100 initiative motivates us to upgrade our global consciousness and action plans in favor of the ocean; it is also a platform to learn from other major ocean multinationals and take action to promote a sustainable ocean economy."

– Patrick Pouyanné, CEO, TotalEnergies [7]

Engage cross-functional ESG working groups that include local communities, fishers, and scientists. This collaborative approach ensures your goals address real-world needs and secures your Social License to Operate.

Incorporating Circular Economy Practices

In addition to setting traditional goals, adopt circular economy principles to enhance resource efficiency. A circular approach minimizes waste while maximizing the value of resources. For example, India generates 6–8 million tons of underutilized marine biomass waste annually, including fish waste, shells, and seaweed [13]. Disposing of this waste in developed countries can cost up to $150 per ton [13]. However, converting it into biopolymers, biofuels, or nutraceuticals not only reduces pollution but also creates new revenue streams.

Design offshore assets with circularity in mind. For example, in May 2025, Shanghai Electric Wind Power introduced recyclable wind turbine blades for offshore installations [2]. This innovation addresses the challenge of decommissioning renewable energy infrastructure without generating landfill waste. Similarly, the Port of Singapore has invested in zero-emission fuel bunkering, while the Port of Antwerp-Bruges has focused on ecological infrastructure to balance sustainability with economic growth [2].

Adopt waste-to-wealth models by transforming underutilized marine waste into valuable products. In India, 80,000 tons of shellfish waste and 34,000 tons of seaweed are generated annually [13]. These materials can be converted into bio-based products, turning a pollution problem into an economic opportunity. With the global cost of marine waste projected to reach $731 billion by 2050 [13], such initiatives offer both environmental and financial benefits.

"Implementing circular economy principles in marine waste management will reduce marine pollution, create employment opportunities, foster social development, and help achieve multiple UN Sustainable Development Goals."

– Poornima Vengaprath Bhattathiri, Observer Research Foundation [13]

Apply lifecycle management principles to legacy infrastructure. For instance, responsibly decommissioning oil and gas rigs can improve ecosystem health while creating jobs in marine restoration [14]. By converting end-of-life materials into new products, you can turn disposal challenges into opportunities. Investing in sustainable ocean sectors like offshore wind and mangrove restoration could yield returns over five times the cost by 2050 [4].

Set specific targets for recycling rates, waste reduction, and the use of bio-based materials in your supply chain. These measurable goals transform circular economy principles into actionable business strategies, ensuring both environmental and economic gains.

Building the Core Components of Your Blue Economy Strategy

After setting your scope and measurable goals, the next step is creating the foundational elements that bring your blue economy strategy to life. This foundation relies on three key components: data-driven resource mapping, collaborative governance structures, and strategic financing mechanisms. Together, these elements address existing gaps in identifying and funding ocean-based initiatives.

The ocean economy, valued at $1.5 trillion in 2010 and expected to reach $3.0 trillion by 2030 [18], faces a significant funding shortfall. Bridging this gap requires precise data, cross-sector collaboration, and innovative financing strategies that align economic growth with ocean health. Let’s dive into how these components work together.

Data-Driven Insights and Resource Mapping

Data is the backbone of the "New Blue Economy", a model that prioritizes knowledge and information to address societal challenges rather than relying solely on resource extraction [1].

Start by utilizing tools like Ocean Accounts to monitor both financial and ecological impacts [6]. Open-source data from NOAA, such as pH levels, salinity, hydrography, and marine life patterns, can guide the placement of offshore wind farms and aquaculture operations [1]. In 2019, the U.S. blue economy supported 2.4 million jobs and contributed $397 billion to the GDP [1].

Marine Spatial Planning (MSP) is another essential tool. By mapping the spatial and temporal distribution of marine activities, MSP reduces investment risks. It requires collecting diverse data types, including environmental factors (like pH and ocean currents), social considerations (such as community dependencies), and economic metrics (like the market value of ecosystem services) [17]. For example, offshore wind projects depend on hydrographic data for turbine placement, fisheries data to avoid conflicts, and economic analysis to ensure long-term benefits.

Companies like Shanghai Electric Wind Power demonstrate how data can drive sustainable practices. In 2025, they introduced recyclable wind turbine blades for offshore use, blending technological innovation with circular economy principles [2].

"The New Blue Economy is a 'knowledge-based economy, looking to the sea not just for extraction of material goods, but for data and information to address societal challenges and inspire their solutions.'"

– Dr. Richard Spinrad, Under Secretary of Commerce for Oceans and Atmosphere & NOAA Administrator [1]

In situations where data is scarce, apply the Precautionary Principle [12]. This means taking a cautious approach to avoid long-term ecological and financial harm when the full environmental impacts of an activity are uncertain.

Collaboration and Governance Structures

Strong partnerships and effective governance are critical for implementing a successful blue economy strategy. Collaboration across sectors ensures activities align with environmental and social goals.

One approach is developing Sustainable Ocean Plans (SOPs) to manage national ocean areas holistically. These plans integrate economic, environmental, and social considerations. For instance, Costa Rica’s National Decarbonization Plan, launched in 2019, secured over $3 billion for renewable infrastructure by prioritizing biodiversity and land-use protections [2].

Engage stakeholders through cross-functional working groups that include local communities, fishers, scientists, and industry representatives. The Port of Singapore exemplifies this approach by investing in zero-emission fuel bunkering infrastructure in collaboration with shipping companies, environmental regulators, and local communities [2].

Public–Private Partnerships (PPPs) are another powerful tool. They combine private-sector innovation and efficiency with public oversight [5][6]. Multistakeholder sessions, or "Deep-Dives", involving regulators, investors, and marine scientists, can generate actionable solutions. Notably, approximately 66% of publicly traded companies rely on the ocean economy to varying degrees [5].

"Momentum is building as more banks, insurers and investors wake up to the realisation that their financial activities can have a sizeable impact on ocean health, creating a negative feedback loop for key ocean industries."

– Eric Usher, Head of UNEP FI [16]

Finally, align governance structures with global agreements like the United Nations Convention on the Law of the Sea (UNCLOS) and the Paris Agreement to ensure long-term alignment with sustainability goals [12].

Financing Blue Economy Initiatives

Securing the right financing is crucial for implementing your strategy. Traditional funding methods often fall short due to perceived risks and difficulties in measuring environmental outcomes. Innovative financial tools can bridge this gap and attract capital.

Blue bonds are a promising option. These debt instruments fund ocean-related projects and are designed to align with sustainable objectives. The International Capital Market Association's (ICMA) Blue Guide offers standardized criteria for issuing blue bonds, which helps build investor confidence [5].

Grants provide low-cost funding without repayment obligations, though they are limited by donor and government budgets. Between 2012 and 2022, philanthropic and official aid sources accounted for most of the $13 billion invested in ocean sustainability [2].

Impact investing is gaining momentum, focusing on measurable ecological and social returns alongside financial results. Research shows that sustainable ocean investments can generate benefits five times greater than their initial costs [16]. However, Sustainable Development Goal (SDG) 14 receives the least investment among all 17 SDGs [18].

Blended finance combines public or philanthropic funds with private capital to reduce risks and attract commercial investors [18]. This approach works particularly well for high-risk projects, such as those in Small Island Developing States (SIDS). Debt-for-nature swaps, for example, are emerging as innovative models in these regions [6].

Creating an Action Plan and Monitoring Framework

Turning your Blue Economy strategy into actionable steps is essential for achieving measurable outcomes. This section explains how to develop a structured roadmap and monitoring framework to ensure your strategy stays on track and delivers results.

Creating an Actionable Roadmap

The Social Well-being Logic Model offers a structured way to sequence objectives: Ocean Equity → Ocean Health → Ocean Wealth [8]. This approach ensures that social and environmental priorities are addressed before advancing economic goals.

To avoid missteps, establish decision gates that require meeting social milestones first. For instance, obtaining Free, Prior, and Informed Consent (FPIC), documenting local roles, and securing benefit-sharing agreements should be prerequisites for project progression [8].

Your roadmap should also include mechanisms to achieve core Blue Economy goals, such as:

Gender Equity (GE): Promoting women's leadership roles.

Social License to Operate (SLO): Building and maintaining community trust.

Ocean Health Investment (OHI): Allocating funds for ecosystem restoration.

Highly Qualified Personnel (HQP): Supporting ocean literacy and workforce development.

For example, an offshore wind project could outline specific steps to ensure community acceptance, fund ecosystem restoration, and provide ocean-related training for local workers.

Collaboration is key. Co-design the roadmap with stakeholders by integrating Indigenous, local, and scientific knowledge through the Two-Eyed Seeing approach [8]. For example, a fishing community's observations about species migration patterns might reveal trends that complement scientific data, creating a more comprehensive understanding of ecosystem changes.

Aligning your roadmap with the UN Sustainable Development Goals (SDGs) ensures global accountability, while using established frameworks like the Global Reporting Initiative (GRI) strengthens reporting consistency [8][9].

Roadmap Phase | Key Action Items | Monitoring/Verification |

|---|---|---|

Step 1: Ocean Equity | Secure FPIC; define local roles; establish benefit-sharing agreements. | Track equity outcomes; implement grievance mechanisms. |

Step 2: Ocean Health | Set thresholds based on science and traditional knowledge; allocate mitigation budgets. | Monitor sentinel indicators; apply trigger-based stop rules. |

Step 3: Ocean Wealth | Define local prosperity metrics (e.g., jobs, procurement percentages). | Publicly report benefits; verify alignment with Ocean Accounts. |

Once your roadmap is in place, the focus shifts to monitoring progress effectively.

Monitoring and Evaluating Progress

A well-designed monitoring framework transforms plans into measurable progress. However, a study of 75 major ocean economy firms revealed that fewer than 25% track ocean-specific impacts beyond energy use and greenhouse gas emissions [10]. Addressing this gap requires adopting targeted, ocean-relevant indicators.

Trigger-based actions are essential for proactive management. For instance, if environmental DNA (eDNA) monitoring detects a significant decline in a keystone species, operations should pause, or stricter controls should be implemented to prevent further harm [8].

Leverage advanced tools to monitor environmental metrics, such as:

Real-time eDNA analysis to detect biodiversity changes.

ROV inspections for underwater assessments.

Satellite imagery for tracking large-scale environmental impacts [10].

Despite 92% of large ocean firms tracking energy use, fewer than one-third report biodiversity-related metrics [10]. Expanding monitoring efforts to include these indicators is critical.

The Blue Economy Capacity Assessment Framework (BECF) can help evaluate contributions to social equity, environmental health, and economic growth. By linking corporate actions to specific SDG targets, this tool ensures a balanced approach [9].

Adopt co-governance structures that bring together corporate representatives, regulators, and community partners for monitoring. This collaborative model has proven effective - 54% of commitments from the High Level Panel for a Sustainable Ocean Economy have been completed, with 40% still in progress [19].

Verification is another key step. Before reporting wealth metrics, confirm that local hiring targets, Indigenous procurement goals, and stewardship funding objectives have been met [8].

Given the fast-changing nature of ocean ecosystems - evidenced by the rise in marine invasive species from 329 in 2008 to over 2,300 by 2024 [10] - review and adjust indicators every 3–5 years based on outcomes and stakeholder input.

Lastly, to improve reporting consistency, move beyond the 443 distinct environmental indicators currently used by corporations [10]. Adopting sector-specific standards, such as those from the GRI or the Taskforce on Nature-related Financial Disclosures (TNFD), can provide clearer guidance tailored to ocean industries.

Working with Experts for Strategy Execution

Once your action plan is in place, the next step is ensuring its smooth execution, which often calls for expert input. Implementing a Blue Economy strategy demands specialized knowledge and seamless coordination across various departments[20].

When selecting a consultant, prioritize those with a strong background in sustainability planning, stakeholder engagement, and data-driven decision-making. They should be well-versed in aligning initiatives with frameworks such as the Kunming-Montreal Global Biodiversity Framework and the Paris Agreement[21]. Look for professionals with a track record of turning policies into actionable roadmaps, complete with clear stages and timelines[20]. These experts can also help create governance structures that strengthen public–private partnerships and promote inclusivity. This means involving all key players - internal teams, external collaborators, and supply chain stakeholders - throughout the implementation process[20].

For example, Council Fire offers expertise in translating sustainability strategies into measurable actions. Their approach integrates systems thinking and stakeholder-focused planning to drive results. By focusing on areas like climate resilience, circular economies, and sustainable infrastructure, they ensure that Blue Economy efforts generate lasting environmental, social, and economic benefits for marine and coastal operations.

Before bringing in external consultants, assess your organization’s internal readiness. Conduct a structured evaluation to determine your Blue Economy exposure, collect baseline data, and establish key performance indicators[21]. Partner with experts who can assist in setting measurable goals aligned with sustainability frameworks, developing monitoring systems to track progress, and building internal capacity to ensure the long-term success of your Blue Economy initiatives[21][22][23].

Conclusion: Taking Action on Blue Economy Opportunities

The blue economy represents an annual opportunity valued between $2.5 trillion and $6 trillion. However, unsustainable practices could jeopardize $8.4 trillion in corporate revenue, highlighting the urgency for action [24][5].

To safeguard operations, uncover new revenue streams, and protect vital marine ecosystems, it’s essential to craft a comprehensive Blue Economy strategy. This means taking proactive steps such as conducting an impact materiality assessment, embedding ocean health into your ESG framework, enhancing leadership’s understanding of ocean-related issues, and identifying connections to marine biodiversity. Financing these efforts can be supported through tools like sustainability-linked loans tied to Blue KPIs.

This holistic approach not only helps mitigate risks but also positions your business to capitalize on emerging market opportunities.

Alfredo Giron, Head of Ocean at the World Economic Forum, emphasizes: "By aligning capital flows with ocean regeneration, we can bring about the systemic change needed to build a resilient blue economy that protects marine ecosystems, empowers communities, and provides broad-based prosperity for future generations" [2].

Currently, the funding gap for sustainable ocean management is estimated at $149 billion annually [15]. While this presents a clear challenge, it also opens doors for companies willing to align their strategies with ocean regeneration. Real-world examples in blue finance show that directing capital toward these goals can yield tangible returns [2].

As this funding gap grows, the cost of inaction becomes even steeper. By building on circular economy principles and fostering collaborative governance, your company can adopt circular practices, integrate scientific insights into strategic planning, and work with marine experts. This approach transforms risks into opportunities, making the Blue Economy not just a concept for tomorrow but a critical business strategy for today.

FAQs

Where do we start with a blue economy strategy?

To effectively approach the sustainable use of ocean resources, start by delving into the key principles behind it. Begin with a detailed evaluation of existing ocean-related activities to understand their current impact and scope. Identify areas where sustainable growth can be achieved while ensuring alignment with established guidelines, such as NOAA’s Blue Economy Strategic Plan. Anchoring your strategy in these proven frameworks allows for a well-structured approach that supports responsible marine resource management and encourages collaboration among stakeholders within the U.S. blue economy.

What ocean KPIs should we track beyond carbon?

To truly understand and protect our oceans, it’s essential to go beyond carbon-focused metrics and track a broader range of ocean-related indicators. Key performance indicators (KPIs) should include aspects of marine ecosystem health, such as provisioning, regulating, supporting, and even cultural values tied to the oceans.

Some critical metrics to monitor include:

Biodiversity levels: Assess the variety of marine life and its resilience.

Habitat restoration progress: Track efforts to rehabilitate ecosystems like coral reefs and mangroves.

Pollution levels: Measure contaminants in water, including chemical pollutants and runoff.

Plastic waste entry: Monitor how much plastic is entering marine environments.

Overfishing rates: Evaluate the extent of unsustainable fishing practices.

Sustainable marine resource use: Analyze the balance between resource extraction and long-term ocean health.

By keeping an eye on these indicators, organizations and policymakers can better gauge environmental impact and advance efforts toward building a sustainable Blue Economy.

How do we fund blue economy projects?

Funding projects within the blue economy frequently requires a mix of public and private financing. Some of the most effective tools include blue bonds, blue loans, and other specialized financial instruments designed to back sustainable ocean-related efforts. Governments play a vital role by establishing clear investment guidelines that encourage participation. Combining public funds, contributions from development banks, and private capital proves especially important for initiatives such as coastal resilience, renewable energy projects, and the management of marine ecosystems.

Related Blog Posts

Latest Articles

©2025

FAQ

01

What does it really mean to “redefine profit”?

02

What makes Council Fire different?

03

Who does Council Fire you work with?

04

What does working with Council Fire actually look like?

05

How does Council Fire help organizations turn big goals into action?

06

How does Council Fire define and measure success?

Mar 20, 2026

How to Develop a Blue Economy Strategy for Corporations

Sustainability Strategy

In This Article

Practical guide for corporations to build a Blue Economy strategy: assess ocean impacts, set SMART goals, adopt circular practices, and secure blue finance.

How to Develop a Blue Economy Strategy for Corporations

The Blue Economy focuses on the responsible use of ocean and water resources to drive economic growth while protecting ecosystems. With a global value of $2.5 trillion annually, it ranks as one of the largest economic sectors. Corporations can benefit from this growing market by aligning their operations with sustainability principles, addressing risks like climate change, and exploring opportunities in marine industries.

Key Steps for Corporations:

Baseline Assessment: Evaluate impacts across energy use, pollution, habitat changes, and biodiversity.

Engage Stakeholders: Secure community consent and ensure equitable practices.

Set Measurable Goals: Use SMART objectives tied to ocean health and UN SDGs.

Adopt Circular Practices: Reduce waste and create value from marine byproducts.

Leverage Data: Use advanced tools like Marine Spatial Planning and real-time monitoring.

Secure Financing: Explore blue bonds, grants, and blended finance options.

With ocean-based industries projected to generate over $3 trillion annually by 2030, transitioning to a sustainable model is both a business opportunity and a necessity. Companies must act now to balance profitability with the preservation of marine ecosystems.

6-Step Blue Economy Strategy Framework for Corporations

Rethinking Ocean Finance: Innovative Strategies for a Sustainable Blue Economy

Evaluating Your Company's Blue Economy Readiness

Assess how your company interacts with ocean ecosystems while aligning with principles of equity, environmental health, and sustainable economic growth.

Conducting a Baseline Assessment

Begin with the Blue Economy Development Approach (BEDA), which emphasizes a step-by-step progression: Ocean Equity → Ocean Health → Ocean Wealth [8]. This sequence ensures that social and environmental priorities are addressed before focusing on economic outcomes.

To create a comprehensive baseline, evaluate your operations across eight critical ocean impact areas, which go far beyond standard carbon reporting. These include energy use, pollution (solid waste, wastewater, hazardous substances, plastic), habitat changes, biomass extraction, noise pollution, and the introduction of non-native species [10]. A review of 75 major ocean-economy firms revealed the use of 443 different indicators to measure environmental impacts. However, fewer than 25% of these metrics specifically addressed ocean-related concerns beyond energy and greenhouse gas emissions [10].

Separate maritime data from terrestrial data, including emissions, waste, and water usage, to pinpoint marine-specific liabilities [10]. While 92% of large ocean firms track energy use, only 16% of their metrics cover biodiversity impacts, and just 7% measure or set targets for habitat alteration [10].

Establish an equity gate by obtaining Free, Prior, and Informed Consent (FPIC) from local and Indigenous communities. Ensure transparent benefit-sharing agreements are in place [8]. Use stakeholder mapping to assess your Social License to Operate (SLO), gauging the level of ongoing community acceptance for your operations [9].

Lawrence M. Mak and colleagues in Frontiers in Marine Science caution: "Equity-blind ocean policies can back-fire even when they are environmentally ambitious" [8].

Incorporate the "Two-Eyed Seeing" approach by combining scientific indicators, such as biodiversity scores, with Indigenous and local knowledge, like seasonal species patterns. This dual perspective enhances your understanding of environmental risks, as traditional knowledge often identifies ecosystem changes that scientific methods may overlook [8].

Utilize the Blue Economy Capacity Framework (BECF) to highlight gaps in four key areas: Gender Equity (GE), Social License to Operate (SLO), Ocean Health Investment (OHI), and Highly Qualified Personnel (HQP) [9]. Align these findings with relevant UN Sustainable Development Goals (SDGs), such as SDG 14.2 (ecosystem protection) and SDG 5.5 (gender equity), adapting them to your company’s specific needs [9].

With a solid baseline in place, you can assess how your operational impacts translate into risks and opportunities within the blue economy.

Identifying Opportunities and Risks

Once you’ve established a baseline, examine the interplay between how ocean health affects your business and how your business affects the ocean [10]. This dual perspective helps you identify vulnerabilities and environmental liabilities tied to your activities.

The blue economy offers growth opportunities in five key sectors: marine transportation, ocean exploration, seafood competitiveness, tourism and recreation, and coastal resilience [11]. By 2050, the sustainable ocean economy is expected to reach a market value of $5.5 trillion [3]. Between 1995 and 2020, it supported over 100 million full-time equivalent jobs globally [3].

Regulatory risks are also evolving. The Kunming-Montreal Global Biodiversity Framework (Target 15) now mandates large transnational companies to disclose biodiversity risks and impacts [10]. Additionally, the Ocean Investment Protocol, introduced in July 2025, provides actionable steps for aligning business practices with ocean health goals [3].

Implement trigger-based monitoring systems that incorporate environmental health thresholds informed by both scientific and traditional knowledge. Set "stop rules" or corrective actions to address any breaches of these thresholds [8]. This proactive approach minimizes the risk of minor issues escalating into significant environmental or regulatory challenges.

Jessica Smith and Suzanne Johnson from the UN Environment Programme Finance Initiative emphasize: "The blue economy links ocean health with prosperity, making targeted finance more urgent than ever" [3].

While most companies track energy use (92%) and pollution (92%), impacts such as noise (33%) and collisions with marine fauna (11%) are often overlooked [10]. Considering that the ocean has absorbed over 90% of the excess heat generated by human activity and about 25% of carbon dioxide emissions in the past 50 years [3], climate resilience must be a key focus for ocean-dependent businesses.

Setting Strategy Scope and Objectives

After assessing your baseline and identifying risks, it's time to craft a strategy that reflects your company’s tangible impact on marine ecosystems. This involves narrowing your focus to specific marine activities, regions, and stakeholder groups where meaningful change is possible. The goal is to move beyond the traditional "ocean economy" mindset, which prioritizes revenue, to embrace a blue economy approach that integrates social and environmental considerations [9].

Your strategy should focus on areas where your company has direct influence. For instance, if your operations affect local coastal fisheries, your goals should target those ecosystems rather than broader, less actionable goals like "improving ocean health." Avoid relying entirely on government mandates; instead, focus on what your business can achieve independently [9].

To shape your strategy, use the core focus areas identified in your baseline - GE, SLO, OHI, and HQP - as a framework [9]. This structure helps balance economic growth with environmental and social responsibilities. With ocean-based industries expected to generate over $3 trillion annually by 2030 [2], defining clear boundaries and realistic objectives is essential.

Incorporate the precautionary principle to mitigate risks associated with uncertain environmental impacts [12]. Once your scope is defined, the next step is to establish measurable objectives that drive actionable results.

Setting Measurable Goals

To ensure accountability, set SMART goals - Specific, Measurable, Achievable, Relevant, and Time-bound. Vague statements like “improve ocean health” lack clarity and impact. Instead, focus on specific targets, such as reducing wastewater discharge by 30% by December 31, 2030, or achieving 40% women’s representation in marine leadership roles by December 31, 2028.

Integrate double materiality to evaluate both the impact of your business on the ocean and how ocean health affects your financial performance [15]. Studies show that $4.3 trillion in corporate revenue - 11.7% of the total revenue from 48,000 companies - faces risks from marine ecosystem degradation [15]. This dual perspective helps identify priorities that align environmental preservation with financial stability.

Align your goals with established frameworks like the Global Reporting Initiative (GRI) for impact materiality, SASB for financial materiality, and TCFD for climate-related financial risks. Use the Blue Economy Capacity Assessment Framework (BECF) to translate UN Sustainable Development Goals (SDGs) into actionable company-level objectives. For example:

SDG Target | Blue Economy Industry Aim | Corporate Action Example |

|---|---|---|

5.5 & 16.7 | Gender Equity | Ensure women’s full participation in marine operations leadership |

1.4, 8.4, 11.7, 12.6 | Social License to Operate | Adopt sustainable reporting and ensure equitable access to ocean resources |

14.2 & 6.6 | Ocean Health Investment | Restore marine ecosystems and manage water quality impacts |

4.7 & 10.4 | Highly Qualified Personnel | Provide ocean literacy training and equitable wage policies |

Setting science-based targets with realistic timelines adds credibility to your strategy. While the 100 largest companies in the blue economy generated $1.1 trillion in revenue in 2018, only $13 billion was invested in ocean sustainability between 2012 and 2022 [2]. Bridging this funding gap requires deliberate commitments, such as allocating capital to marine conservation and restoration projects.

"Joining the Ocean 100 initiative motivates us to upgrade our global consciousness and action plans in favor of the ocean; it is also a platform to learn from other major ocean multinationals and take action to promote a sustainable ocean economy."

– Patrick Pouyanné, CEO, TotalEnergies [7]

Engage cross-functional ESG working groups that include local communities, fishers, and scientists. This collaborative approach ensures your goals address real-world needs and secures your Social License to Operate.

Incorporating Circular Economy Practices

In addition to setting traditional goals, adopt circular economy principles to enhance resource efficiency. A circular approach minimizes waste while maximizing the value of resources. For example, India generates 6–8 million tons of underutilized marine biomass waste annually, including fish waste, shells, and seaweed [13]. Disposing of this waste in developed countries can cost up to $150 per ton [13]. However, converting it into biopolymers, biofuels, or nutraceuticals not only reduces pollution but also creates new revenue streams.

Design offshore assets with circularity in mind. For example, in May 2025, Shanghai Electric Wind Power introduced recyclable wind turbine blades for offshore installations [2]. This innovation addresses the challenge of decommissioning renewable energy infrastructure without generating landfill waste. Similarly, the Port of Singapore has invested in zero-emission fuel bunkering, while the Port of Antwerp-Bruges has focused on ecological infrastructure to balance sustainability with economic growth [2].

Adopt waste-to-wealth models by transforming underutilized marine waste into valuable products. In India, 80,000 tons of shellfish waste and 34,000 tons of seaweed are generated annually [13]. These materials can be converted into bio-based products, turning a pollution problem into an economic opportunity. With the global cost of marine waste projected to reach $731 billion by 2050 [13], such initiatives offer both environmental and financial benefits.

"Implementing circular economy principles in marine waste management will reduce marine pollution, create employment opportunities, foster social development, and help achieve multiple UN Sustainable Development Goals."

– Poornima Vengaprath Bhattathiri, Observer Research Foundation [13]

Apply lifecycle management principles to legacy infrastructure. For instance, responsibly decommissioning oil and gas rigs can improve ecosystem health while creating jobs in marine restoration [14]. By converting end-of-life materials into new products, you can turn disposal challenges into opportunities. Investing in sustainable ocean sectors like offshore wind and mangrove restoration could yield returns over five times the cost by 2050 [4].

Set specific targets for recycling rates, waste reduction, and the use of bio-based materials in your supply chain. These measurable goals transform circular economy principles into actionable business strategies, ensuring both environmental and economic gains.

Building the Core Components of Your Blue Economy Strategy

After setting your scope and measurable goals, the next step is creating the foundational elements that bring your blue economy strategy to life. This foundation relies on three key components: data-driven resource mapping, collaborative governance structures, and strategic financing mechanisms. Together, these elements address existing gaps in identifying and funding ocean-based initiatives.

The ocean economy, valued at $1.5 trillion in 2010 and expected to reach $3.0 trillion by 2030 [18], faces a significant funding shortfall. Bridging this gap requires precise data, cross-sector collaboration, and innovative financing strategies that align economic growth with ocean health. Let’s dive into how these components work together.

Data-Driven Insights and Resource Mapping

Data is the backbone of the "New Blue Economy", a model that prioritizes knowledge and information to address societal challenges rather than relying solely on resource extraction [1].

Start by utilizing tools like Ocean Accounts to monitor both financial and ecological impacts [6]. Open-source data from NOAA, such as pH levels, salinity, hydrography, and marine life patterns, can guide the placement of offshore wind farms and aquaculture operations [1]. In 2019, the U.S. blue economy supported 2.4 million jobs and contributed $397 billion to the GDP [1].

Marine Spatial Planning (MSP) is another essential tool. By mapping the spatial and temporal distribution of marine activities, MSP reduces investment risks. It requires collecting diverse data types, including environmental factors (like pH and ocean currents), social considerations (such as community dependencies), and economic metrics (like the market value of ecosystem services) [17]. For example, offshore wind projects depend on hydrographic data for turbine placement, fisheries data to avoid conflicts, and economic analysis to ensure long-term benefits.

Companies like Shanghai Electric Wind Power demonstrate how data can drive sustainable practices. In 2025, they introduced recyclable wind turbine blades for offshore use, blending technological innovation with circular economy principles [2].

"The New Blue Economy is a 'knowledge-based economy, looking to the sea not just for extraction of material goods, but for data and information to address societal challenges and inspire their solutions.'"

– Dr. Richard Spinrad, Under Secretary of Commerce for Oceans and Atmosphere & NOAA Administrator [1]

In situations where data is scarce, apply the Precautionary Principle [12]. This means taking a cautious approach to avoid long-term ecological and financial harm when the full environmental impacts of an activity are uncertain.

Collaboration and Governance Structures

Strong partnerships and effective governance are critical for implementing a successful blue economy strategy. Collaboration across sectors ensures activities align with environmental and social goals.

One approach is developing Sustainable Ocean Plans (SOPs) to manage national ocean areas holistically. These plans integrate economic, environmental, and social considerations. For instance, Costa Rica’s National Decarbonization Plan, launched in 2019, secured over $3 billion for renewable infrastructure by prioritizing biodiversity and land-use protections [2].

Engage stakeholders through cross-functional working groups that include local communities, fishers, scientists, and industry representatives. The Port of Singapore exemplifies this approach by investing in zero-emission fuel bunkering infrastructure in collaboration with shipping companies, environmental regulators, and local communities [2].

Public–Private Partnerships (PPPs) are another powerful tool. They combine private-sector innovation and efficiency with public oversight [5][6]. Multistakeholder sessions, or "Deep-Dives", involving regulators, investors, and marine scientists, can generate actionable solutions. Notably, approximately 66% of publicly traded companies rely on the ocean economy to varying degrees [5].

"Momentum is building as more banks, insurers and investors wake up to the realisation that their financial activities can have a sizeable impact on ocean health, creating a negative feedback loop for key ocean industries."

– Eric Usher, Head of UNEP FI [16]

Finally, align governance structures with global agreements like the United Nations Convention on the Law of the Sea (UNCLOS) and the Paris Agreement to ensure long-term alignment with sustainability goals [12].

Financing Blue Economy Initiatives

Securing the right financing is crucial for implementing your strategy. Traditional funding methods often fall short due to perceived risks and difficulties in measuring environmental outcomes. Innovative financial tools can bridge this gap and attract capital.

Blue bonds are a promising option. These debt instruments fund ocean-related projects and are designed to align with sustainable objectives. The International Capital Market Association's (ICMA) Blue Guide offers standardized criteria for issuing blue bonds, which helps build investor confidence [5].

Grants provide low-cost funding without repayment obligations, though they are limited by donor and government budgets. Between 2012 and 2022, philanthropic and official aid sources accounted for most of the $13 billion invested in ocean sustainability [2].

Impact investing is gaining momentum, focusing on measurable ecological and social returns alongside financial results. Research shows that sustainable ocean investments can generate benefits five times greater than their initial costs [16]. However, Sustainable Development Goal (SDG) 14 receives the least investment among all 17 SDGs [18].

Blended finance combines public or philanthropic funds with private capital to reduce risks and attract commercial investors [18]. This approach works particularly well for high-risk projects, such as those in Small Island Developing States (SIDS). Debt-for-nature swaps, for example, are emerging as innovative models in these regions [6].

Creating an Action Plan and Monitoring Framework

Turning your Blue Economy strategy into actionable steps is essential for achieving measurable outcomes. This section explains how to develop a structured roadmap and monitoring framework to ensure your strategy stays on track and delivers results.

Creating an Actionable Roadmap

The Social Well-being Logic Model offers a structured way to sequence objectives: Ocean Equity → Ocean Health → Ocean Wealth [8]. This approach ensures that social and environmental priorities are addressed before advancing economic goals.

To avoid missteps, establish decision gates that require meeting social milestones first. For instance, obtaining Free, Prior, and Informed Consent (FPIC), documenting local roles, and securing benefit-sharing agreements should be prerequisites for project progression [8].

Your roadmap should also include mechanisms to achieve core Blue Economy goals, such as:

Gender Equity (GE): Promoting women's leadership roles.

Social License to Operate (SLO): Building and maintaining community trust.

Ocean Health Investment (OHI): Allocating funds for ecosystem restoration.

Highly Qualified Personnel (HQP): Supporting ocean literacy and workforce development.

For example, an offshore wind project could outline specific steps to ensure community acceptance, fund ecosystem restoration, and provide ocean-related training for local workers.

Collaboration is key. Co-design the roadmap with stakeholders by integrating Indigenous, local, and scientific knowledge through the Two-Eyed Seeing approach [8]. For example, a fishing community's observations about species migration patterns might reveal trends that complement scientific data, creating a more comprehensive understanding of ecosystem changes.

Aligning your roadmap with the UN Sustainable Development Goals (SDGs) ensures global accountability, while using established frameworks like the Global Reporting Initiative (GRI) strengthens reporting consistency [8][9].

Roadmap Phase | Key Action Items | Monitoring/Verification |

|---|---|---|

Step 1: Ocean Equity | Secure FPIC; define local roles; establish benefit-sharing agreements. | Track equity outcomes; implement grievance mechanisms. |

Step 2: Ocean Health | Set thresholds based on science and traditional knowledge; allocate mitigation budgets. | Monitor sentinel indicators; apply trigger-based stop rules. |

Step 3: Ocean Wealth | Define local prosperity metrics (e.g., jobs, procurement percentages). | Publicly report benefits; verify alignment with Ocean Accounts. |

Once your roadmap is in place, the focus shifts to monitoring progress effectively.

Monitoring and Evaluating Progress

A well-designed monitoring framework transforms plans into measurable progress. However, a study of 75 major ocean economy firms revealed that fewer than 25% track ocean-specific impacts beyond energy use and greenhouse gas emissions [10]. Addressing this gap requires adopting targeted, ocean-relevant indicators.

Trigger-based actions are essential for proactive management. For instance, if environmental DNA (eDNA) monitoring detects a significant decline in a keystone species, operations should pause, or stricter controls should be implemented to prevent further harm [8].

Leverage advanced tools to monitor environmental metrics, such as:

Real-time eDNA analysis to detect biodiversity changes.

ROV inspections for underwater assessments.

Satellite imagery for tracking large-scale environmental impacts [10].

Despite 92% of large ocean firms tracking energy use, fewer than one-third report biodiversity-related metrics [10]. Expanding monitoring efforts to include these indicators is critical.

The Blue Economy Capacity Assessment Framework (BECF) can help evaluate contributions to social equity, environmental health, and economic growth. By linking corporate actions to specific SDG targets, this tool ensures a balanced approach [9].

Adopt co-governance structures that bring together corporate representatives, regulators, and community partners for monitoring. This collaborative model has proven effective - 54% of commitments from the High Level Panel for a Sustainable Ocean Economy have been completed, with 40% still in progress [19].

Verification is another key step. Before reporting wealth metrics, confirm that local hiring targets, Indigenous procurement goals, and stewardship funding objectives have been met [8].

Given the fast-changing nature of ocean ecosystems - evidenced by the rise in marine invasive species from 329 in 2008 to over 2,300 by 2024 [10] - review and adjust indicators every 3–5 years based on outcomes and stakeholder input.

Lastly, to improve reporting consistency, move beyond the 443 distinct environmental indicators currently used by corporations [10]. Adopting sector-specific standards, such as those from the GRI or the Taskforce on Nature-related Financial Disclosures (TNFD), can provide clearer guidance tailored to ocean industries.

Working with Experts for Strategy Execution

Once your action plan is in place, the next step is ensuring its smooth execution, which often calls for expert input. Implementing a Blue Economy strategy demands specialized knowledge and seamless coordination across various departments[20].

When selecting a consultant, prioritize those with a strong background in sustainability planning, stakeholder engagement, and data-driven decision-making. They should be well-versed in aligning initiatives with frameworks such as the Kunming-Montreal Global Biodiversity Framework and the Paris Agreement[21]. Look for professionals with a track record of turning policies into actionable roadmaps, complete with clear stages and timelines[20]. These experts can also help create governance structures that strengthen public–private partnerships and promote inclusivity. This means involving all key players - internal teams, external collaborators, and supply chain stakeholders - throughout the implementation process[20].

For example, Council Fire offers expertise in translating sustainability strategies into measurable actions. Their approach integrates systems thinking and stakeholder-focused planning to drive results. By focusing on areas like climate resilience, circular economies, and sustainable infrastructure, they ensure that Blue Economy efforts generate lasting environmental, social, and economic benefits for marine and coastal operations.

Before bringing in external consultants, assess your organization’s internal readiness. Conduct a structured evaluation to determine your Blue Economy exposure, collect baseline data, and establish key performance indicators[21]. Partner with experts who can assist in setting measurable goals aligned with sustainability frameworks, developing monitoring systems to track progress, and building internal capacity to ensure the long-term success of your Blue Economy initiatives[21][22][23].

Conclusion: Taking Action on Blue Economy Opportunities

The blue economy represents an annual opportunity valued between $2.5 trillion and $6 trillion. However, unsustainable practices could jeopardize $8.4 trillion in corporate revenue, highlighting the urgency for action [24][5].

To safeguard operations, uncover new revenue streams, and protect vital marine ecosystems, it’s essential to craft a comprehensive Blue Economy strategy. This means taking proactive steps such as conducting an impact materiality assessment, embedding ocean health into your ESG framework, enhancing leadership’s understanding of ocean-related issues, and identifying connections to marine biodiversity. Financing these efforts can be supported through tools like sustainability-linked loans tied to Blue KPIs.

This holistic approach not only helps mitigate risks but also positions your business to capitalize on emerging market opportunities.

Alfredo Giron, Head of Ocean at the World Economic Forum, emphasizes: "By aligning capital flows with ocean regeneration, we can bring about the systemic change needed to build a resilient blue economy that protects marine ecosystems, empowers communities, and provides broad-based prosperity for future generations" [2].

Currently, the funding gap for sustainable ocean management is estimated at $149 billion annually [15]. While this presents a clear challenge, it also opens doors for companies willing to align their strategies with ocean regeneration. Real-world examples in blue finance show that directing capital toward these goals can yield tangible returns [2].

As this funding gap grows, the cost of inaction becomes even steeper. By building on circular economy principles and fostering collaborative governance, your company can adopt circular practices, integrate scientific insights into strategic planning, and work with marine experts. This approach transforms risks into opportunities, making the Blue Economy not just a concept for tomorrow but a critical business strategy for today.

FAQs

Where do we start with a blue economy strategy?

To effectively approach the sustainable use of ocean resources, start by delving into the key principles behind it. Begin with a detailed evaluation of existing ocean-related activities to understand their current impact and scope. Identify areas where sustainable growth can be achieved while ensuring alignment with established guidelines, such as NOAA’s Blue Economy Strategic Plan. Anchoring your strategy in these proven frameworks allows for a well-structured approach that supports responsible marine resource management and encourages collaboration among stakeholders within the U.S. blue economy.

What ocean KPIs should we track beyond carbon?

To truly understand and protect our oceans, it’s essential to go beyond carbon-focused metrics and track a broader range of ocean-related indicators. Key performance indicators (KPIs) should include aspects of marine ecosystem health, such as provisioning, regulating, supporting, and even cultural values tied to the oceans.

Some critical metrics to monitor include:

Biodiversity levels: Assess the variety of marine life and its resilience.

Habitat restoration progress: Track efforts to rehabilitate ecosystems like coral reefs and mangroves.

Pollution levels: Measure contaminants in water, including chemical pollutants and runoff.

Plastic waste entry: Monitor how much plastic is entering marine environments.

Overfishing rates: Evaluate the extent of unsustainable fishing practices.

Sustainable marine resource use: Analyze the balance between resource extraction and long-term ocean health.

By keeping an eye on these indicators, organizations and policymakers can better gauge environmental impact and advance efforts toward building a sustainable Blue Economy.

How do we fund blue economy projects?

Funding projects within the blue economy frequently requires a mix of public and private financing. Some of the most effective tools include blue bonds, blue loans, and other specialized financial instruments designed to back sustainable ocean-related efforts. Governments play a vital role by establishing clear investment guidelines that encourage participation. Combining public funds, contributions from development banks, and private capital proves especially important for initiatives such as coastal resilience, renewable energy projects, and the management of marine ecosystems.

Related Blog Posts

FAQ

01

What does it really mean to “redefine profit”?

02

What makes Council Fire different?

03

Who does Council Fire you work with?

04

What does working with Council Fire actually look like?

05

How does Council Fire help organizations turn big goals into action?

06

How does Council Fire define and measure success?

Mar 20, 2026

How to Develop a Blue Economy Strategy for Corporations

Sustainability Strategy

In This Article

Practical guide for corporations to build a Blue Economy strategy: assess ocean impacts, set SMART goals, adopt circular practices, and secure blue finance.

How to Develop a Blue Economy Strategy for Corporations

The Blue Economy focuses on the responsible use of ocean and water resources to drive economic growth while protecting ecosystems. With a global value of $2.5 trillion annually, it ranks as one of the largest economic sectors. Corporations can benefit from this growing market by aligning their operations with sustainability principles, addressing risks like climate change, and exploring opportunities in marine industries.

Key Steps for Corporations:

Baseline Assessment: Evaluate impacts across energy use, pollution, habitat changes, and biodiversity.

Engage Stakeholders: Secure community consent and ensure equitable practices.

Set Measurable Goals: Use SMART objectives tied to ocean health and UN SDGs.

Adopt Circular Practices: Reduce waste and create value from marine byproducts.

Leverage Data: Use advanced tools like Marine Spatial Planning and real-time monitoring.

Secure Financing: Explore blue bonds, grants, and blended finance options.

With ocean-based industries projected to generate over $3 trillion annually by 2030, transitioning to a sustainable model is both a business opportunity and a necessity. Companies must act now to balance profitability with the preservation of marine ecosystems.

6-Step Blue Economy Strategy Framework for Corporations

Rethinking Ocean Finance: Innovative Strategies for a Sustainable Blue Economy

Evaluating Your Company's Blue Economy Readiness

Assess how your company interacts with ocean ecosystems while aligning with principles of equity, environmental health, and sustainable economic growth.

Conducting a Baseline Assessment

Begin with the Blue Economy Development Approach (BEDA), which emphasizes a step-by-step progression: Ocean Equity → Ocean Health → Ocean Wealth [8]. This sequence ensures that social and environmental priorities are addressed before focusing on economic outcomes.

To create a comprehensive baseline, evaluate your operations across eight critical ocean impact areas, which go far beyond standard carbon reporting. These include energy use, pollution (solid waste, wastewater, hazardous substances, plastic), habitat changes, biomass extraction, noise pollution, and the introduction of non-native species [10]. A review of 75 major ocean-economy firms revealed the use of 443 different indicators to measure environmental impacts. However, fewer than 25% of these metrics specifically addressed ocean-related concerns beyond energy and greenhouse gas emissions [10].

Separate maritime data from terrestrial data, including emissions, waste, and water usage, to pinpoint marine-specific liabilities [10]. While 92% of large ocean firms track energy use, only 16% of their metrics cover biodiversity impacts, and just 7% measure or set targets for habitat alteration [10].

Establish an equity gate by obtaining Free, Prior, and Informed Consent (FPIC) from local and Indigenous communities. Ensure transparent benefit-sharing agreements are in place [8]. Use stakeholder mapping to assess your Social License to Operate (SLO), gauging the level of ongoing community acceptance for your operations [9].

Lawrence M. Mak and colleagues in Frontiers in Marine Science caution: "Equity-blind ocean policies can back-fire even when they are environmentally ambitious" [8].

Incorporate the "Two-Eyed Seeing" approach by combining scientific indicators, such as biodiversity scores, with Indigenous and local knowledge, like seasonal species patterns. This dual perspective enhances your understanding of environmental risks, as traditional knowledge often identifies ecosystem changes that scientific methods may overlook [8].

Utilize the Blue Economy Capacity Framework (BECF) to highlight gaps in four key areas: Gender Equity (GE), Social License to Operate (SLO), Ocean Health Investment (OHI), and Highly Qualified Personnel (HQP) [9]. Align these findings with relevant UN Sustainable Development Goals (SDGs), such as SDG 14.2 (ecosystem protection) and SDG 5.5 (gender equity), adapting them to your company’s specific needs [9].

With a solid baseline in place, you can assess how your operational impacts translate into risks and opportunities within the blue economy.

Identifying Opportunities and Risks

Once you’ve established a baseline, examine the interplay between how ocean health affects your business and how your business affects the ocean [10]. This dual perspective helps you identify vulnerabilities and environmental liabilities tied to your activities.

The blue economy offers growth opportunities in five key sectors: marine transportation, ocean exploration, seafood competitiveness, tourism and recreation, and coastal resilience [11]. By 2050, the sustainable ocean economy is expected to reach a market value of $5.5 trillion [3]. Between 1995 and 2020, it supported over 100 million full-time equivalent jobs globally [3].

Regulatory risks are also evolving. The Kunming-Montreal Global Biodiversity Framework (Target 15) now mandates large transnational companies to disclose biodiversity risks and impacts [10]. Additionally, the Ocean Investment Protocol, introduced in July 2025, provides actionable steps for aligning business practices with ocean health goals [3].

Implement trigger-based monitoring systems that incorporate environmental health thresholds informed by both scientific and traditional knowledge. Set "stop rules" or corrective actions to address any breaches of these thresholds [8]. This proactive approach minimizes the risk of minor issues escalating into significant environmental or regulatory challenges.

Jessica Smith and Suzanne Johnson from the UN Environment Programme Finance Initiative emphasize: "The blue economy links ocean health with prosperity, making targeted finance more urgent than ever" [3].

While most companies track energy use (92%) and pollution (92%), impacts such as noise (33%) and collisions with marine fauna (11%) are often overlooked [10]. Considering that the ocean has absorbed over 90% of the excess heat generated by human activity and about 25% of carbon dioxide emissions in the past 50 years [3], climate resilience must be a key focus for ocean-dependent businesses.

Setting Strategy Scope and Objectives

After assessing your baseline and identifying risks, it's time to craft a strategy that reflects your company’s tangible impact on marine ecosystems. This involves narrowing your focus to specific marine activities, regions, and stakeholder groups where meaningful change is possible. The goal is to move beyond the traditional "ocean economy" mindset, which prioritizes revenue, to embrace a blue economy approach that integrates social and environmental considerations [9].

Your strategy should focus on areas where your company has direct influence. For instance, if your operations affect local coastal fisheries, your goals should target those ecosystems rather than broader, less actionable goals like "improving ocean health." Avoid relying entirely on government mandates; instead, focus on what your business can achieve independently [9].

To shape your strategy, use the core focus areas identified in your baseline - GE, SLO, OHI, and HQP - as a framework [9]. This structure helps balance economic growth with environmental and social responsibilities. With ocean-based industries expected to generate over $3 trillion annually by 2030 [2], defining clear boundaries and realistic objectives is essential.

Incorporate the precautionary principle to mitigate risks associated with uncertain environmental impacts [12]. Once your scope is defined, the next step is to establish measurable objectives that drive actionable results.

Setting Measurable Goals

To ensure accountability, set SMART goals - Specific, Measurable, Achievable, Relevant, and Time-bound. Vague statements like “improve ocean health” lack clarity and impact. Instead, focus on specific targets, such as reducing wastewater discharge by 30% by December 31, 2030, or achieving 40% women’s representation in marine leadership roles by December 31, 2028.

Integrate double materiality to evaluate both the impact of your business on the ocean and how ocean health affects your financial performance [15]. Studies show that $4.3 trillion in corporate revenue - 11.7% of the total revenue from 48,000 companies - faces risks from marine ecosystem degradation [15]. This dual perspective helps identify priorities that align environmental preservation with financial stability.

Align your goals with established frameworks like the Global Reporting Initiative (GRI) for impact materiality, SASB for financial materiality, and TCFD for climate-related financial risks. Use the Blue Economy Capacity Assessment Framework (BECF) to translate UN Sustainable Development Goals (SDGs) into actionable company-level objectives. For example:

SDG Target | Blue Economy Industry Aim | Corporate Action Example |

|---|---|---|

5.5 & 16.7 | Gender Equity | Ensure women’s full participation in marine operations leadership |

1.4, 8.4, 11.7, 12.6 | Social License to Operate | Adopt sustainable reporting and ensure equitable access to ocean resources |

14.2 & 6.6 | Ocean Health Investment | Restore marine ecosystems and manage water quality impacts |

4.7 & 10.4 | Highly Qualified Personnel | Provide ocean literacy training and equitable wage policies |

Setting science-based targets with realistic timelines adds credibility to your strategy. While the 100 largest companies in the blue economy generated $1.1 trillion in revenue in 2018, only $13 billion was invested in ocean sustainability between 2012 and 2022 [2]. Bridging this funding gap requires deliberate commitments, such as allocating capital to marine conservation and restoration projects.

"Joining the Ocean 100 initiative motivates us to upgrade our global consciousness and action plans in favor of the ocean; it is also a platform to learn from other major ocean multinationals and take action to promote a sustainable ocean economy."

– Patrick Pouyanné, CEO, TotalEnergies [7]

Engage cross-functional ESG working groups that include local communities, fishers, and scientists. This collaborative approach ensures your goals address real-world needs and secures your Social License to Operate.

Incorporating Circular Economy Practices

In addition to setting traditional goals, adopt circular economy principles to enhance resource efficiency. A circular approach minimizes waste while maximizing the value of resources. For example, India generates 6–8 million tons of underutilized marine biomass waste annually, including fish waste, shells, and seaweed [13]. Disposing of this waste in developed countries can cost up to $150 per ton [13]. However, converting it into biopolymers, biofuels, or nutraceuticals not only reduces pollution but also creates new revenue streams.

Design offshore assets with circularity in mind. For example, in May 2025, Shanghai Electric Wind Power introduced recyclable wind turbine blades for offshore installations [2]. This innovation addresses the challenge of decommissioning renewable energy infrastructure without generating landfill waste. Similarly, the Port of Singapore has invested in zero-emission fuel bunkering, while the Port of Antwerp-Bruges has focused on ecological infrastructure to balance sustainability with economic growth [2].

Adopt waste-to-wealth models by transforming underutilized marine waste into valuable products. In India, 80,000 tons of shellfish waste and 34,000 tons of seaweed are generated annually [13]. These materials can be converted into bio-based products, turning a pollution problem into an economic opportunity. With the global cost of marine waste projected to reach $731 billion by 2050 [13], such initiatives offer both environmental and financial benefits.

"Implementing circular economy principles in marine waste management will reduce marine pollution, create employment opportunities, foster social development, and help achieve multiple UN Sustainable Development Goals."

– Poornima Vengaprath Bhattathiri, Observer Research Foundation [13]

Apply lifecycle management principles to legacy infrastructure. For instance, responsibly decommissioning oil and gas rigs can improve ecosystem health while creating jobs in marine restoration [14]. By converting end-of-life materials into new products, you can turn disposal challenges into opportunities. Investing in sustainable ocean sectors like offshore wind and mangrove restoration could yield returns over five times the cost by 2050 [4].

Set specific targets for recycling rates, waste reduction, and the use of bio-based materials in your supply chain. These measurable goals transform circular economy principles into actionable business strategies, ensuring both environmental and economic gains.

Building the Core Components of Your Blue Economy Strategy

After setting your scope and measurable goals, the next step is creating the foundational elements that bring your blue economy strategy to life. This foundation relies on three key components: data-driven resource mapping, collaborative governance structures, and strategic financing mechanisms. Together, these elements address existing gaps in identifying and funding ocean-based initiatives.

The ocean economy, valued at $1.5 trillion in 2010 and expected to reach $3.0 trillion by 2030 [18], faces a significant funding shortfall. Bridging this gap requires precise data, cross-sector collaboration, and innovative financing strategies that align economic growth with ocean health. Let’s dive into how these components work together.

Data-Driven Insights and Resource Mapping

Data is the backbone of the "New Blue Economy", a model that prioritizes knowledge and information to address societal challenges rather than relying solely on resource extraction [1].

Start by utilizing tools like Ocean Accounts to monitor both financial and ecological impacts [6]. Open-source data from NOAA, such as pH levels, salinity, hydrography, and marine life patterns, can guide the placement of offshore wind farms and aquaculture operations [1]. In 2019, the U.S. blue economy supported 2.4 million jobs and contributed $397 billion to the GDP [1].

Marine Spatial Planning (MSP) is another essential tool. By mapping the spatial and temporal distribution of marine activities, MSP reduces investment risks. It requires collecting diverse data types, including environmental factors (like pH and ocean currents), social considerations (such as community dependencies), and economic metrics (like the market value of ecosystem services) [17]. For example, offshore wind projects depend on hydrographic data for turbine placement, fisheries data to avoid conflicts, and economic analysis to ensure long-term benefits.

Companies like Shanghai Electric Wind Power demonstrate how data can drive sustainable practices. In 2025, they introduced recyclable wind turbine blades for offshore use, blending technological innovation with circular economy principles [2].

"The New Blue Economy is a 'knowledge-based economy, looking to the sea not just for extraction of material goods, but for data and information to address societal challenges and inspire their solutions.'"

– Dr. Richard Spinrad, Under Secretary of Commerce for Oceans and Atmosphere & NOAA Administrator [1]

In situations where data is scarce, apply the Precautionary Principle [12]. This means taking a cautious approach to avoid long-term ecological and financial harm when the full environmental impacts of an activity are uncertain.

Collaboration and Governance Structures