Mar 21, 2026

How to Develop a Blue Economy Strategy for NGOs & Nonprofits

Sustainability Strategy

In This Article

A practical framework for NGOs to assess readiness, map ocean assets, build partnerships, secure blended finance, and measure Blue Economy impact.

How to Develop a Blue Economy Strategy for NGOs & Nonprofits

The Blue Economy offers NGOs and nonprofits a chance to combine marine conservation with job creation and economic growth. With the ocean economy valued at $2.5 trillion annually, this approach supports livelihoods, strengthens climate resilience, and aligns with global sustainability goals like SDG 14 (Life Below Water) and SDG 13 (Climate Action).

To get started, organizations should:

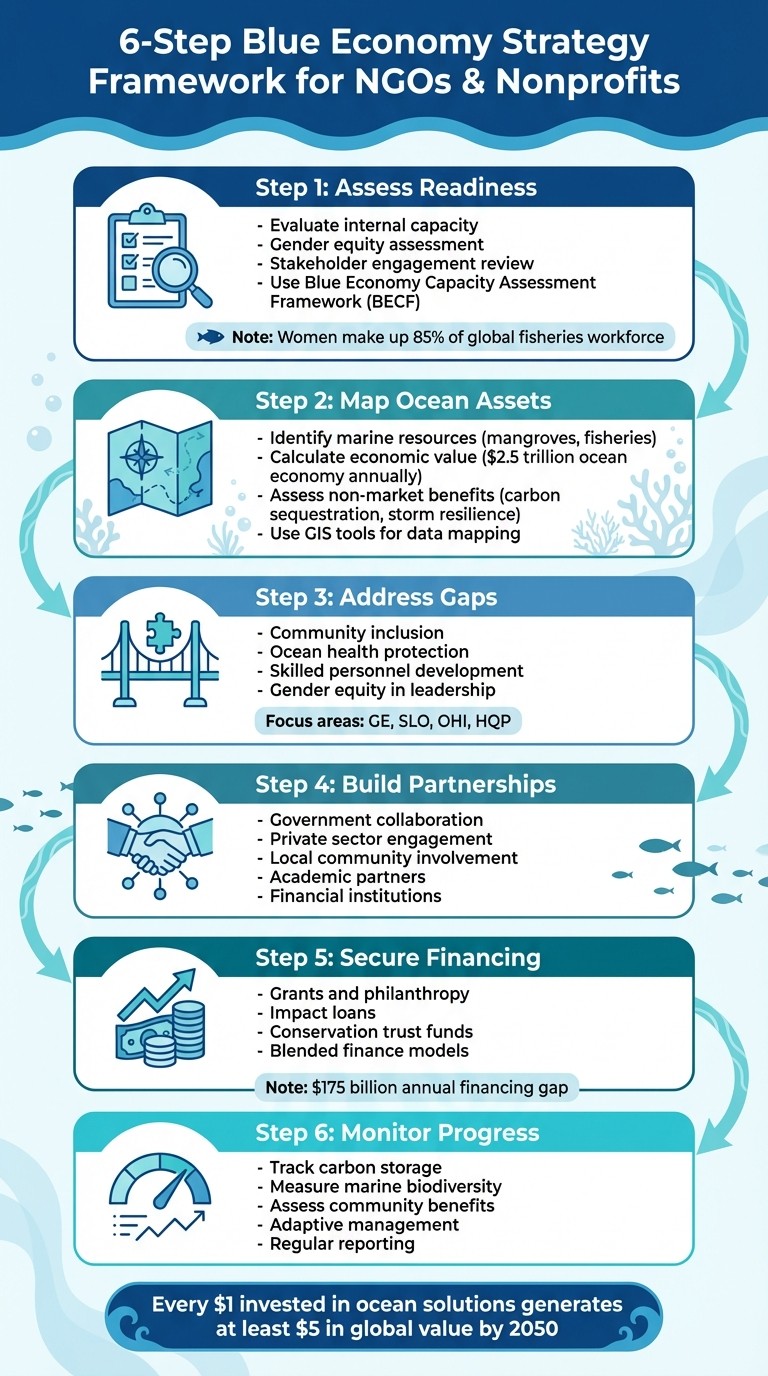

Assess Readiness: Evaluate internal capacity, gender equity, and stakeholder engagement.

Map Ocean Assets: Identify resources like mangroves and fisheries, including their economic and non-economic value.

Address Gaps: Focus on areas like community inclusion, ocean health, and skilled personnel.

Build Partnerships: Collaborate with governments, private sectors, and local communities.

Secure Financing: Use grants, impact loans, and conservation funds to support projects.

Monitor Progress: Track outcomes like carbon storage, marine biodiversity, and community benefits.

6-Step Blue Economy Strategy Framework for NGOs and Nonprofits

Sustainable Blue Economy

Assessing Your Organization's Readiness for Blue Economy Work

Before diving into Blue Economy initiatives, it's crucial to evaluate your organization's current capabilities. This assessment ensures your operational strengths align with the strategic goals of the Blue Economy. Key areas to examine include internal capacity, engagement with marine ecosystems, and the need for partnerships.

Conducting an Internal Audit

Start by reviewing your organization's readiness using the Blue Economy Capacity Assessment Framework (BECF). This framework evaluates four key areas: Gender Equity (GE), Social License to Operate (SLO), Ocean Health Investment (OHI), and Highly Qualified Personnel (HQP) [9].

Ask yourself some essential questions during this audit. Does your team include individuals trained in ocean literacy and sustainable development? Women make up 85% of the global fisheries workforce, yet they are often underrepresented in leadership roles [3]. Assess whether your leadership promotes gender equity (aligned with SDG 5.5) and if decision-making processes are inclusive (SDG 16.7) [9].

"The blue economy should not be confused with the ocean economy which is measured in terms of the oceans-based industries' contribution to economic output and employment." - Ronnie Noonan-Birch et al., Frontiers in Marine Science [9]

Additionally, evaluate whether your operations prioritize decoupling economic growth from environmental harm, incorporating sustainability metrics (SDG 8.4 & SDG 12.6) [9]. A compelling example of this is The Ocean Foundation's collaboration with Fundación Tropicalia in the Dominican Republic. By developing a Sustainability Management System rooted in UN Global Compact principles and Global Reporting Initiative guidelines, the organization produced five consecutive sustainability reports that documented its adherence to Blue Economy principles [2].

Lastly, consider your ability to engage stakeholders. Securing a "Social License to Operate" requires ongoing approval from local communities impacted by marine projects [9].

This internal review lays the groundwork for mapping your organization's ocean-related assets.

Mapping Ocean-Dependent Assets

Understanding your organization's reliance on ocean resources involves identifying both market and non-market values. While the global ocean economy generates approximately $2.3 trillion annually from market goods [11], it's equally important to account for non-market benefits like carbon sequestration from seagrass and mangroves, storm resilience, and the cultural connections tied to marine ecosystems [11][2].

Tools like Geographic Information Systems (GIS) and environmental assessments can help determine the quality and availability of data for your planning efforts [10]. For instance, in the Caribbean, where over 90% of economies depend directly on the ocean [7], mapping becomes a critical step. Make sure to include marginalized groups, women, and Indigenous communities in your stakeholder analysis to build genuine social license rather than superficial sustainability claims [9][3].

Rhode Island provides a useful example. The state's Blue Economy accounts for 8.8% of its GDP, supporting over 36,500 jobs across industries like defense ($3.16 billion), marine trades ($1.45 billion), and fisheries ($151.5 million) [6]. By conducting thorough mapping, Rhode Island identified specific opportunities and gaps across various marine sectors.

Early stakeholder engagement is essential for defining mandatory standards for resource use and conservation [10]. A notable example is The Ocean Foundation's 2017 training for Philippine government officials. This initiative prepared the country for its ASEAN chairmanship by focusing on sustainable Blue Economy practices and financing coastal and marine resources. The training enabled officials to identify regulatory gaps and establish a cohesive approach to marine resource management [2].

Use these mapped assets to uncover areas where your strategy can be refined.

Identifying Gaps and Opportunities

Building on the insights from your audit and asset mapping, conduct a "Blue Shortcoming" assessment to identify areas for improvement across the four BECF categories [9].

Assessment Area | Key Focus | Strategic Value |

|---|---|---|

Gender Equity (GE) | Leadership roles and women’s participation | Enhances profitability and productivity [9] |

Social License (SLO) | Community acceptance and stakeholder buy-in | Ensures project viability and reduces political risks [9] |

Ocean Health (OHI) | Protection of carbon sinks and habitats | Safeguards critical ecosystem assets driving the economy [9][2] |

Qualified Personnel (HQP) | Skills in sustainability and innovation | Attracts investment and fosters innovation [9] |

In fiscal year 2024, the PROBLUE multi-donor trust fund approved 64 technical assistance proposals totaling $37.8 million [8]. Accessing such resources requires demonstrating strong capacity in these assessment areas.

Your gap analysis should also evaluate your organization's digital readiness. Are you equipped to use tools like the "Aquaculture Digital Roadmap" to enhance marine resource management efficiency? [8] Can you implement Marine Spatial Planning (MSP) to reduce investment risks and improve access to marine resources? [10]

Finally, ensure that Indigenous and local knowledge systems are not just consulted but actively integrated into your governance and scientific practices [9][3]. This approach is essential for achieving equity, a cornerstone of sustainable Blue Economy strategies.

"Equity is a prerequisite for a sustainable ocean economy, where humanity safeguards marine and coastal ecosystems, sustainably uses ocean resources, and ensures equitable distribution of benefits." - Micheline Khan and Eliza Northrop, World Resources Institute [3]

Building Partnerships for Blue Economy Success

Creating successful strategies for the Blue Economy hinges on forging partnerships across various sectors. These collaborations lay the groundwork for effective governance and networking in Blue Economy initiatives.

Engaging Stakeholders Across Sectors

The first step is identifying the right stakeholders. A comprehensive stakeholder map should include:

Public sector: For regulatory guidance and policy alignment.

Private sector: To drive investment and innovation.

Civil society organizations: For community engagement and advocacy.

Financial institutions: To manage investment risks.

Academic partners: For research and technical insights.

A great example of this multi-sector approach is the partnership between the Global Green Growth Institute (GGGI) and the Caribbean Biodiversity Fund (CBF), formed in September 2025. This collaboration, led by CBF CEO Karen McDonald Gayle and GGGI Representative Daniel Muñoz-Smith, aims to unlock funding for coastal restoration in the Caribbean. So far, the CBF has supported over 100 projects across 12 countries, with more than $30 million in funding provided [7].

"This partnership with GGGI empowers us to turn ambition into action, unlocking finance for communities to restore coastal ecosystems, protect biodiversity, and build resilient livelihoods that sustain us all" [7].

Inclusive planning is key. Ensure Indigenous leaders, women, and marginalized groups are part of the decision-making process. This not only promotes fairness but also strengthens local support and regulatory compliance. Stakeholders should work together on a unified plan that balances competing interests like fishing, conservation, shipping, and tourism [3].

When working with private sector partners, consider teaming up with multilateral development banks and insurers to reduce risks through tools like concessional financing and first-loss guarantees [12]. Additionally, identifying "industry clusters" - geographical hubs of interconnected businesses - can help locate infrastructure and research collaborators [6].

Once stakeholder engagement is in place, the next step is establishing a governance framework to ensure these partnerships thrive.

Establishing Governance Frameworks

Governance structures are critical for turning collaboration into results. A strong governance framework should be inclusive, adaptive, accountable, and transparent [1]. This involves creating decision-making processes that involve all relevant local stakeholders, particularly those whose livelihoods depend on marine resources.

Area-based decision platforms can align human and natural resources at the local level [5]. These platforms streamline public and private investments while ensuring ecosystem restoration remains a priority in economic development.

Align governance efforts with international agreements like the UN 2030 Agenda for Sustainable Development and the Paris Agreement. Regional strategies, such as the African Union Blue Economy Strategy, also provide useful blueprints [5]. Indigenous organizations should be granted permanent status and full consultation rights, as seen in the Arctic Council model [3]. This approach ensures Indigenous communities have a genuine role in strategic decision-making [15].

Adopting policies that recognize a clean and sustainable environment as a human right provides a legal framework for protecting communities from environmental harm. This rights-based approach also enhances accountability in partnerships [3].

Leveraging Existing Alliances and Networks

Established networks can amplify the impact of your partnerships and governance structures. Global coalitions like the Blue Prosperity Coalition bring technical expertise and assist governments in implementing sustainable ocean plans across their waters [13]. Regional groups, such as the Northeast Regional Ocean Council (NROC), enable organizations to align objectives, share data, and combine resources for Blue Economy projects [14].

The World Bank's PROBLUE program is another valuable resource. In fiscal year 2024, it approved 64 proposals worth $37.8 million, supporting technical work in over 100 economies [8]. One standout initiative is the "Unleashing the Blue Economy of the Caribbean" (UBEC) project, a $90 million program launched in November 2024. This project, funded by the World Bank and PROBLUE, focuses on empowering women entrepreneurs in the Blue Economy sector [8].

Engaging with international bodies like the Commonwealth Blue Charter or the High-Level Panel for a Sustainable Ocean Economy can help shape global standards for sustainable ocean practices [2]. Using standardized ocean accounting frameworks enables reliable data collection on ecosystem services, which is essential for reducing investment risks and supporting blended finance approaches [16]. When working with data related to Indigenous waters, adhere to the CARE Principles (Collective benefit, Authority to control, Responsibility, Ethics) to ensure Indigenous communities maintain control over their data [15].

Finally, innovation hubs like Blue Tech Week and OceanHub Africa offer opportunities to connect with startups and technologies focused on sustainable ocean use. These platforms foster collaboration and provide access to cutting-edge solutions for tackling shared challenges.

Developing and Implementing Your Blue Economy Strategy

Once partnerships and governance structures are in place, the next step is crafting a strategy that delivers measurable outcomes. The focus should shift from traditional "ocean business" models to regenerative practices that restore ecosystems while supporting sustainable livelihoods [2].

Mapping Ocean Wealth and Setting Goals

Start by using your mapped ocean-dependent assets to establish measurable and integrated targets. This involves collecting both quantitative data - such as the current value of marine activities, resource availability, and funding levels - and qualitative insights, including community interests, iconic features, and political support [17].

"We see value in an economy that has restorative activities. One that can lead to enhanced human health and well-being, including food security and the creation of sustainable livelihoods" [2].

Set goals that balance ecological health, social equity, and economic viability. For example, when Chile expanded its Marine Protected Area (MPA) coverage from 150,000 hectares to 150 million hectares in 2018, the government collaborated with the Blue Nature Alliance to identify viable financing mechanisms. Using a simple 2x2 matrix, they assessed funding sources based on "feasibility" and "potential revenue", ultimately highlighting philanthropy and levies on sustainable use as the most effective options due to Chile's eco-tourism potential and MPA usage rates [17].

Develop long-term budget forecasts that go beyond standard planning cycles. Nature-based solutions often come with fluctuating management costs, so understanding these financial gaps early is essential for successful project launches [17]. With clear objectives in hand, the next step is to focus on implementing regenerative solutions.

Prioritizing Nature-Based Solutions

With targets set, prioritize projects that actively restore marine ecosystems while offering direct benefits to coastal communities. Special attention should go to blue carbon ecosystems - such as seagrasses, mangroves, and salt marshes - which are vital for climate mitigation [2].

The Great Blue Wall initiative offers a compelling example. Spearheaded by the IUCN and supported by African partners, this project aims to protect 30% of the Western Indian Ocean's waters (over 2 million square kilometers) by 2030, sequestering 100 million tons of CO2. Additionally, it is expected to generate 2 million jobs and create income opportunities for over 70 million people [4].

When selecting projects, consider the enabling conditions of your target area. This includes local interest, political support, and the presence of iconic marine features that can attract investments. A standout example is the Climate Sheroes Project in Pakistan, which involves over 500 women in mangrove planting and management. The project not only improves marine health but also provides steady income through the sale of mangrove products, diversifying local livelihoods [4].

Use a clear three-step framework to guide financing for nature-based solutions:

Collect detailed data on potential projects and funding sources.

Rank financing instruments by feasibility and revenue potential.

Develop roadmaps with 3–5 actionable steps for each goal, identifying key stakeholders, donors, and decision-makers [17].

Incorporating Systems Thinking and Adaptive Management

The interconnected nature of Blue Economy challenges calls for systems thinking, which considers how various marine sectors interact. For instance, St. Kitts and Nevis developed a comprehensive marine zoning plan by engaging government agencies, community groups, and fishers' associations. This participatory process integrated fishing, conservation, shipping, and tourism into a unified vision for sustainable ocean management [3].

Pair this approach with adaptive management practices that allow for ongoing performance monitoring and quick adjustments. A Sustainability Management System, featuring indicator matrices, can help track progress and refine strategies over time [2]. Such flexibility is crucial, as ocean conditions are constantly changing.

It's also important to mainstream biodiversity and ecosystem services into the objectives of other economic sectors. This ensures that shared resources are managed sustainably and that trade-offs are well-informed [10]. Early stakeholder engagement is critical to identify non-negotiable thresholds for resource use - limits that safeguard essential ecosystem functions even as economic development progresses [10].

"Sustainability and equity are two sides of the same coin" [3].

Finally, ensure that your adaptive management approach evaluates whether benefits are reaching marginalized groups, including women and Indigenous communities. These groups often bear the brunt of ocean-related activities while being excluded from their rewards. Addressing this imbalance is key to building an equitable Blue Economy.

Securing and Managing Financing for Blue Economy Projects

NGOs and nonprofits face a daunting $175 billion annual financing gap for advancing ocean sustainability [21]. To address this, combining diverse funding sources and creating sustainable financial systems is essential.

Blended Financing for Blue Economy Projects

Blended finance combines philanthropic grants with impact investments and concessional debt, aiming to reduce risks for commercial investors. Catalytic capital, such as grants for early-stage costs like legal structuring and business planning, plays a critical role in this process.

In October 2024, Blue Alliance and BNP Paribas introduced an impact loan facility focused on coral reef conservation. This initiative blended a $5.2 million grant from the Global Fund for Coral Reefs with impact loans from BNP Paribas. The program supports 1.7 million hectares of Marine Protected Areas across the Philippines, Tanzania, and Indonesia, fostering seven reef-positive businesses in ecotourism and aquaculture. By 2040, it aims to scale up to 70 million hectares and unlock $20 million in private investments [20][19].

"A multi-stakeholder approach is central to successful project development and management. This should include governments, engaged and experienced NGOs, and partners with skills in social entrepreneurship, financial planning, and marine conservation."

– Nicolas Pascal, Executive Director, Blue Alliance Marine Protected Areas [19]

Grants are often crucial for covering the initial management costs of Marine Protected Areas until revenue-generating ventures can sustain themselves.

Comparing Financing Options

Different financing mechanisms cater to various stages, scales, and risk tolerances of Blue Economy projects.

Conservation Trust Funds (CTFs) come in three forms:

Endowment funds: Invest capital and use interest earnings, ideal for long-term funding of no-take zones.

Sinking funds: Gradually spend down capital for time-bound projects.

Revolving funds: Replenish through taxes or fees, supporting ongoing coastal management.

Between 2009 and 2018, CTFs globally disbursed over $2 billion [22].

Debt-for-nature swaps restructure sovereign debt to fund conservation. For instance, Belize raised $364 million to pay off $546 million in old debt at a 45% discount, freeing up $180 million for marine conservation. Similarly, the Seychelles refinanced debt to secure protection for 32% of its waters (400,000 km²) by March 2020 [22].

Parametric insurance provides quick payouts after extreme weather events. Following Hurricane Delta in December 2020, Quintana Roo, Mexico, received $800,000 from a $3.8 million policy to fund coral reef restoration [22].

Mechanism | Primary Source | Risk Level | Best Use Case |

|---|---|---|---|

Grants | Philanthropy/Government | Low | Early-stage management and technical assistance [19] |

Impact Loans | Private Investors | Moderate | Scaling reef-positive businesses with proven models [19] |

Blue Bonds | Capital Markets | High | Large-scale national marine spatial planning [18] |

CTF Endowment | Philanthropy | Low | Perpetual funding for no-take zones [22] |

These mechanisms offer tailored solutions for building financial stability and advancing ocean conservation.

Building Financial Resilience

For NGOs and nonprofits, ensuring the long-term success of Blue Economy projects requires a mix of funding sources and proactive financial risk management. Pairing early-stage grants with revenue-generating reef-positive businesses creates more sustainable funding streams.

Establishing reliable baselines with measurable impact metrics and third-party monitoring is crucial. Data like fish biomass, carbon sequestration rates, and coral health assessments can boost donor and investor confidence. Frameworks such as the IFC Performance Standards or GIIN IRIS+ metrics ensure transparency in reporting [19].

Regional conservation trust funds, such as the Caribbean Biodiversity Fund, can streamline access to funding by reducing transaction costs and providing technical assistance [21].

"We need to step out of our investor, grant maker, policymaker, and practitioner siloes to continue these important conversations that create the enabling conditions to collaboratively mobilize resources to fill the gaps."

– Stacy Jupiter, Executive Director, WCS Global Marine Program [21]

Incorporating tools like parametric insurance protects coastal projects from climate-related risks, making them more appealing to cautious investors [20].

Investing in sustainable ocean solutions offers immense returns - every $1 invested can yield at least $5 in benefits by 2050 [23][24]. By diversifying funding strategies, organizations can transform short-term efforts into enduring conservation systems.

Monitoring, Scaling, and Sustaining Blue Economy Strategies

Monitoring progress is more than a checkpoint - it’s the foundation for creating scalable and adaptable strategies that support long-term ocean stewardship. By combining these efforts, NGOs and nonprofits can maintain effective Blue Economy strategies that align with sustainable development goals and promote fairness.

Establishing Monitoring and Evaluation Metrics

Tracking progress happens on three fronts: implementation (like spending and behavioral changes), environmental impact (such as biomass and carbon storage), and long-term socio-economic benefits (economic growth, food security, and equity) [26].

Metrics should go beyond financial results to include non-monetary benefits. For instance, calculate carbon stored in seagrass meadows and mangroves, measure storm protection offered by coastal wetlands, and assess pollution filtration services [2][26]. Success indicators might include reductions in plastic waste, nutrient runoff, and noise pollution [26]. Equity metrics are equally important - these assess whether marginalized groups are involved in decision-making and if Indigenous cultural heritage is safeguarded [3][26].

A practical example comes from The Ocean Foundation’s Sustainability Management System (SMS) for Fundación Tropicalia. This system enabled annual reporting on environmental, social, and economic progress through detailed indicator matrices, ensuring alignment with local socio-economic priorities [2].

"Meaningful blue economy investing must have real, measurable positive outcomes."

– Mark J. Spalding, President, The Ocean Foundation [26]

With well-defined metrics, organizations can confidently expand and sustain regenerative initiatives.

Scaling Successful Initiatives

Scaling efforts often transition from mitigation to full-scale ecosystem restoration. A standout example is the Great Blue Wall initiative, spearheaded by the IUCN and African partners. Launched in 2024, this project aims to protect 30% of the Western Indian Ocean - an area of roughly 772,000 square miles - by 2030. Its ambitious goals include sequestering 100 million tons of CO₂ and creating 2 million jobs through restored mangroves, seagrasses, and coral reefs [4].

Key to scaling is the use of blended finance models. These models combine philanthropic or grant funding to support early-stage reef-positive businesses until they can attract private investment [27]. When expanding to new regions, establishing local nonprofit entities is essential. These organizations collaborate with regional authorities, empowering communities to manage Marine Protected Areas while governments oversee regulations [27].

The Climate Sheroes project in Pakistan offers a powerful example of this approach. By involving over 500 women in mangrove restoration and management, the project linked ecological recovery with social equity. Local livelihoods were diversified through income generated from selling mangrove products, showcasing how scaling can balance environmental and social goals [4].

These initiatives highlight how scaling efforts can pave the way for adaptive management practices that ensure long-term success.

Ensuring Sustainability Through Adaptive Management

Sustainability hinges on continuous learning and adjustments informed by monitoring data. Implementation roadmaps are crucial - they outline specific actions, identify key stakeholders, and evaluate potential revenue alongside time commitments for each project [17]. Budgets should extend beyond standard funding cycles to account for shifting management costs and potential financing gaps over time [17].

A review of Ocean Panel countries revealed that 54% of ocean-related commitments have been completed, with 40% still in progress. This underscores the importance of systematic tracking and accountability [25]. Using a feasibility-versus-revenue matrix can help prioritize funding sources, ranging from philanthropic contributions to sustainable use levies, for short-, medium-, and long-term needs [17].

Adaptive management also involves addressing the true costs of harmful activities, such as plastic pollution and carbon emissions, to reduce financial risks [26]. Evaluating both economic returns and "ocean returns" - like biomass growth and carbon storage - ensures that strategies remain both financially viable and ecologically responsible [26]. Advances in technology, such as AI and satellite monitoring, now make it possible to track ecological changes in real time [4].

"We need to keep in mind what measurable outputs investors can deliver themselves, versus the outcomes that depend on others to occur... and we need to acknowledge our need to measure both."

– Mark J. Spalding, President, The Ocean Foundation [26]

Conclusion: Key Steps for Developing a Blue Economy Strategy

Creating a strong Blue Economy strategy means shifting focus from exploiting ocean resources to adopting regenerative practices that promote human well-being, ensure food security, and support sustainable livelihoods [2]. Start by assessing your internal capabilities, mapping out ocean resources, and identifying any existing gaps, as outlined in earlier sections. From there, craft Sustainable Ocean Plans that connect all sectors - conservation, fishing, shipping, tourism, and more - so that ocean management becomes holistic rather than fragmented [3].

Collaboration is essential. Build multi-stakeholder platforms that bring together scientists, industry leaders, policymakers, and local communities [5]. This approach goes beyond simply gathering input; it ensures decision-making is inclusive. As Micheline Khan and Eliza Northrop from the World Resources Institute state:

"Sustainability and equity are two sides of the same coin. Equity is a prerequisite for a sustainable ocean economy" [3].

Your funding strategy should combine various sources, such as philanthropic grants, concessional financing, and private investments. This blend supports both early-stage initiatives and long-term sustainability efforts while emphasizing non-market benefits like carbon storage, storm protection, and cultural heritage preservation [2]. Highlighting these values strengthens your case for funding and showcases meaningful impacts beyond financial gains.

Emerging technologies and data-driven tools can significantly enhance your efforts. Use innovations like IoT devices and satellite monitoring for real-time tracking of ecological changes [5]. Investing in ocean-related initiatives offers not only ecological benefits but also economic returns, with every $1 spent on key ocean actions generating at least $5 in global value [28].

Adopt flexible management practices that rely on continuous monitoring and timely adjustments. Align your strategy with global goals such as the UN Sustainable Development Goals and the Paris Agreement to ensure your work contributes to larger ocean stewardship objectives [5]. While the ocean economy demands substantial investment and long-term commitment, clear planning, inclusive governance, and innovative solutions can drive meaningful change for communities and ecosystems that depend on the ocean.

FAQs

What’s the difference between the Blue Economy and the ocean economy?

The ocean economy encompasses all industries and activities connected to the ocean, including shipping, fishing, and oil extraction, without necessarily considering their environmental impact. In contrast, the Blue Economy emphasizes the responsible and sustainable use of ocean resources. Its goal is to balance economic growth, support for livelihoods, and the preservation of marine ecosystems, ensuring the health of the oceans for future generations. While the ocean economy focuses broadly on economic activities, the Blue Economy prioritizes practices that safeguard marine environments.

How can our nonprofit measure “ocean returns” like carbon and biodiversity?

Nonprofits aiming to measure "ocean returns" - such as carbon storage and biodiversity - can rely on established frameworks and tools to guide their efforts. For carbon tracking, frameworks like the High-Quality Blue Carbon Principles and tools such as the Progress Wheel are invaluable. These resources help monitor carbon sequestration and evaluate overall ecosystem health.

When assessing biodiversity, focus on ecosystem services, including provisioning (resources like food and water), regulating (climate control and water purification), and cultural benefits (recreational and spiritual value). By aligning these metrics with widely recognized standards, your organization can ensure precise measurement and advance its blue economy objectives effectively.

Which funding option fits our project stage (grants, impact loans, blue bonds)?

Grants work well for early-stage efforts like managing Marine Protected Areas (MPAs) or building capacity. They help cover operational costs until the project can sustain itself financially. Impact loans, on the other hand, are geared toward ventures that have proven their viability and are ready to expand. These loans often fund activities such as enterprises that benefit reefs or initiatives supporting community livelihoods. For larger, well-established projects with steady revenue streams, blue bonds offer long-term funding, making them a strong option for scaling up significant initiatives.

Related Blog Posts

Latest Articles

©2025

FAQ

01

What does it really mean to “redefine profit”?

02

What makes Council Fire different?

03

Who does Council Fire you work with?

04

What does working with Council Fire actually look like?

05

How does Council Fire help organizations turn big goals into action?

06

How does Council Fire define and measure success?

Mar 21, 2026

How to Develop a Blue Economy Strategy for NGOs & Nonprofits

Sustainability Strategy

In This Article

A practical framework for NGOs to assess readiness, map ocean assets, build partnerships, secure blended finance, and measure Blue Economy impact.

How to Develop a Blue Economy Strategy for NGOs & Nonprofits

The Blue Economy offers NGOs and nonprofits a chance to combine marine conservation with job creation and economic growth. With the ocean economy valued at $2.5 trillion annually, this approach supports livelihoods, strengthens climate resilience, and aligns with global sustainability goals like SDG 14 (Life Below Water) and SDG 13 (Climate Action).

To get started, organizations should:

Assess Readiness: Evaluate internal capacity, gender equity, and stakeholder engagement.

Map Ocean Assets: Identify resources like mangroves and fisheries, including their economic and non-economic value.

Address Gaps: Focus on areas like community inclusion, ocean health, and skilled personnel.

Build Partnerships: Collaborate with governments, private sectors, and local communities.

Secure Financing: Use grants, impact loans, and conservation funds to support projects.

Monitor Progress: Track outcomes like carbon storage, marine biodiversity, and community benefits.

6-Step Blue Economy Strategy Framework for NGOs and Nonprofits

Sustainable Blue Economy

Assessing Your Organization's Readiness for Blue Economy Work

Before diving into Blue Economy initiatives, it's crucial to evaluate your organization's current capabilities. This assessment ensures your operational strengths align with the strategic goals of the Blue Economy. Key areas to examine include internal capacity, engagement with marine ecosystems, and the need for partnerships.

Conducting an Internal Audit

Start by reviewing your organization's readiness using the Blue Economy Capacity Assessment Framework (BECF). This framework evaluates four key areas: Gender Equity (GE), Social License to Operate (SLO), Ocean Health Investment (OHI), and Highly Qualified Personnel (HQP) [9].

Ask yourself some essential questions during this audit. Does your team include individuals trained in ocean literacy and sustainable development? Women make up 85% of the global fisheries workforce, yet they are often underrepresented in leadership roles [3]. Assess whether your leadership promotes gender equity (aligned with SDG 5.5) and if decision-making processes are inclusive (SDG 16.7) [9].

"The blue economy should not be confused with the ocean economy which is measured in terms of the oceans-based industries' contribution to economic output and employment." - Ronnie Noonan-Birch et al., Frontiers in Marine Science [9]

Additionally, evaluate whether your operations prioritize decoupling economic growth from environmental harm, incorporating sustainability metrics (SDG 8.4 & SDG 12.6) [9]. A compelling example of this is The Ocean Foundation's collaboration with Fundación Tropicalia in the Dominican Republic. By developing a Sustainability Management System rooted in UN Global Compact principles and Global Reporting Initiative guidelines, the organization produced five consecutive sustainability reports that documented its adherence to Blue Economy principles [2].

Lastly, consider your ability to engage stakeholders. Securing a "Social License to Operate" requires ongoing approval from local communities impacted by marine projects [9].

This internal review lays the groundwork for mapping your organization's ocean-related assets.

Mapping Ocean-Dependent Assets

Understanding your organization's reliance on ocean resources involves identifying both market and non-market values. While the global ocean economy generates approximately $2.3 trillion annually from market goods [11], it's equally important to account for non-market benefits like carbon sequestration from seagrass and mangroves, storm resilience, and the cultural connections tied to marine ecosystems [11][2].

Tools like Geographic Information Systems (GIS) and environmental assessments can help determine the quality and availability of data for your planning efforts [10]. For instance, in the Caribbean, where over 90% of economies depend directly on the ocean [7], mapping becomes a critical step. Make sure to include marginalized groups, women, and Indigenous communities in your stakeholder analysis to build genuine social license rather than superficial sustainability claims [9][3].

Rhode Island provides a useful example. The state's Blue Economy accounts for 8.8% of its GDP, supporting over 36,500 jobs across industries like defense ($3.16 billion), marine trades ($1.45 billion), and fisheries ($151.5 million) [6]. By conducting thorough mapping, Rhode Island identified specific opportunities and gaps across various marine sectors.

Early stakeholder engagement is essential for defining mandatory standards for resource use and conservation [10]. A notable example is The Ocean Foundation's 2017 training for Philippine government officials. This initiative prepared the country for its ASEAN chairmanship by focusing on sustainable Blue Economy practices and financing coastal and marine resources. The training enabled officials to identify regulatory gaps and establish a cohesive approach to marine resource management [2].

Use these mapped assets to uncover areas where your strategy can be refined.

Identifying Gaps and Opportunities

Building on the insights from your audit and asset mapping, conduct a "Blue Shortcoming" assessment to identify areas for improvement across the four BECF categories [9].

Assessment Area | Key Focus | Strategic Value |

|---|---|---|

Gender Equity (GE) | Leadership roles and women’s participation | Enhances profitability and productivity [9] |

Social License (SLO) | Community acceptance and stakeholder buy-in | Ensures project viability and reduces political risks [9] |

Ocean Health (OHI) | Protection of carbon sinks and habitats | Safeguards critical ecosystem assets driving the economy [9][2] |

Qualified Personnel (HQP) | Skills in sustainability and innovation | Attracts investment and fosters innovation [9] |

In fiscal year 2024, the PROBLUE multi-donor trust fund approved 64 technical assistance proposals totaling $37.8 million [8]. Accessing such resources requires demonstrating strong capacity in these assessment areas.

Your gap analysis should also evaluate your organization's digital readiness. Are you equipped to use tools like the "Aquaculture Digital Roadmap" to enhance marine resource management efficiency? [8] Can you implement Marine Spatial Planning (MSP) to reduce investment risks and improve access to marine resources? [10]

Finally, ensure that Indigenous and local knowledge systems are not just consulted but actively integrated into your governance and scientific practices [9][3]. This approach is essential for achieving equity, a cornerstone of sustainable Blue Economy strategies.

"Equity is a prerequisite for a sustainable ocean economy, where humanity safeguards marine and coastal ecosystems, sustainably uses ocean resources, and ensures equitable distribution of benefits." - Micheline Khan and Eliza Northrop, World Resources Institute [3]

Building Partnerships for Blue Economy Success

Creating successful strategies for the Blue Economy hinges on forging partnerships across various sectors. These collaborations lay the groundwork for effective governance and networking in Blue Economy initiatives.

Engaging Stakeholders Across Sectors

The first step is identifying the right stakeholders. A comprehensive stakeholder map should include:

Public sector: For regulatory guidance and policy alignment.

Private sector: To drive investment and innovation.

Civil society organizations: For community engagement and advocacy.

Financial institutions: To manage investment risks.

Academic partners: For research and technical insights.

A great example of this multi-sector approach is the partnership between the Global Green Growth Institute (GGGI) and the Caribbean Biodiversity Fund (CBF), formed in September 2025. This collaboration, led by CBF CEO Karen McDonald Gayle and GGGI Representative Daniel Muñoz-Smith, aims to unlock funding for coastal restoration in the Caribbean. So far, the CBF has supported over 100 projects across 12 countries, with more than $30 million in funding provided [7].

"This partnership with GGGI empowers us to turn ambition into action, unlocking finance for communities to restore coastal ecosystems, protect biodiversity, and build resilient livelihoods that sustain us all" [7].

Inclusive planning is key. Ensure Indigenous leaders, women, and marginalized groups are part of the decision-making process. This not only promotes fairness but also strengthens local support and regulatory compliance. Stakeholders should work together on a unified plan that balances competing interests like fishing, conservation, shipping, and tourism [3].

When working with private sector partners, consider teaming up with multilateral development banks and insurers to reduce risks through tools like concessional financing and first-loss guarantees [12]. Additionally, identifying "industry clusters" - geographical hubs of interconnected businesses - can help locate infrastructure and research collaborators [6].

Once stakeholder engagement is in place, the next step is establishing a governance framework to ensure these partnerships thrive.

Establishing Governance Frameworks

Governance structures are critical for turning collaboration into results. A strong governance framework should be inclusive, adaptive, accountable, and transparent [1]. This involves creating decision-making processes that involve all relevant local stakeholders, particularly those whose livelihoods depend on marine resources.

Area-based decision platforms can align human and natural resources at the local level [5]. These platforms streamline public and private investments while ensuring ecosystem restoration remains a priority in economic development.

Align governance efforts with international agreements like the UN 2030 Agenda for Sustainable Development and the Paris Agreement. Regional strategies, such as the African Union Blue Economy Strategy, also provide useful blueprints [5]. Indigenous organizations should be granted permanent status and full consultation rights, as seen in the Arctic Council model [3]. This approach ensures Indigenous communities have a genuine role in strategic decision-making [15].

Adopting policies that recognize a clean and sustainable environment as a human right provides a legal framework for protecting communities from environmental harm. This rights-based approach also enhances accountability in partnerships [3].

Leveraging Existing Alliances and Networks

Established networks can amplify the impact of your partnerships and governance structures. Global coalitions like the Blue Prosperity Coalition bring technical expertise and assist governments in implementing sustainable ocean plans across their waters [13]. Regional groups, such as the Northeast Regional Ocean Council (NROC), enable organizations to align objectives, share data, and combine resources for Blue Economy projects [14].

The World Bank's PROBLUE program is another valuable resource. In fiscal year 2024, it approved 64 proposals worth $37.8 million, supporting technical work in over 100 economies [8]. One standout initiative is the "Unleashing the Blue Economy of the Caribbean" (UBEC) project, a $90 million program launched in November 2024. This project, funded by the World Bank and PROBLUE, focuses on empowering women entrepreneurs in the Blue Economy sector [8].

Engaging with international bodies like the Commonwealth Blue Charter or the High-Level Panel for a Sustainable Ocean Economy can help shape global standards for sustainable ocean practices [2]. Using standardized ocean accounting frameworks enables reliable data collection on ecosystem services, which is essential for reducing investment risks and supporting blended finance approaches [16]. When working with data related to Indigenous waters, adhere to the CARE Principles (Collective benefit, Authority to control, Responsibility, Ethics) to ensure Indigenous communities maintain control over their data [15].

Finally, innovation hubs like Blue Tech Week and OceanHub Africa offer opportunities to connect with startups and technologies focused on sustainable ocean use. These platforms foster collaboration and provide access to cutting-edge solutions for tackling shared challenges.

Developing and Implementing Your Blue Economy Strategy

Once partnerships and governance structures are in place, the next step is crafting a strategy that delivers measurable outcomes. The focus should shift from traditional "ocean business" models to regenerative practices that restore ecosystems while supporting sustainable livelihoods [2].

Mapping Ocean Wealth and Setting Goals

Start by using your mapped ocean-dependent assets to establish measurable and integrated targets. This involves collecting both quantitative data - such as the current value of marine activities, resource availability, and funding levels - and qualitative insights, including community interests, iconic features, and political support [17].

"We see value in an economy that has restorative activities. One that can lead to enhanced human health and well-being, including food security and the creation of sustainable livelihoods" [2].

Set goals that balance ecological health, social equity, and economic viability. For example, when Chile expanded its Marine Protected Area (MPA) coverage from 150,000 hectares to 150 million hectares in 2018, the government collaborated with the Blue Nature Alliance to identify viable financing mechanisms. Using a simple 2x2 matrix, they assessed funding sources based on "feasibility" and "potential revenue", ultimately highlighting philanthropy and levies on sustainable use as the most effective options due to Chile's eco-tourism potential and MPA usage rates [17].

Develop long-term budget forecasts that go beyond standard planning cycles. Nature-based solutions often come with fluctuating management costs, so understanding these financial gaps early is essential for successful project launches [17]. With clear objectives in hand, the next step is to focus on implementing regenerative solutions.

Prioritizing Nature-Based Solutions

With targets set, prioritize projects that actively restore marine ecosystems while offering direct benefits to coastal communities. Special attention should go to blue carbon ecosystems - such as seagrasses, mangroves, and salt marshes - which are vital for climate mitigation [2].

The Great Blue Wall initiative offers a compelling example. Spearheaded by the IUCN and supported by African partners, this project aims to protect 30% of the Western Indian Ocean's waters (over 2 million square kilometers) by 2030, sequestering 100 million tons of CO2. Additionally, it is expected to generate 2 million jobs and create income opportunities for over 70 million people [4].

When selecting projects, consider the enabling conditions of your target area. This includes local interest, political support, and the presence of iconic marine features that can attract investments. A standout example is the Climate Sheroes Project in Pakistan, which involves over 500 women in mangrove planting and management. The project not only improves marine health but also provides steady income through the sale of mangrove products, diversifying local livelihoods [4].

Use a clear three-step framework to guide financing for nature-based solutions:

Collect detailed data on potential projects and funding sources.

Rank financing instruments by feasibility and revenue potential.

Develop roadmaps with 3–5 actionable steps for each goal, identifying key stakeholders, donors, and decision-makers [17].

Incorporating Systems Thinking and Adaptive Management

The interconnected nature of Blue Economy challenges calls for systems thinking, which considers how various marine sectors interact. For instance, St. Kitts and Nevis developed a comprehensive marine zoning plan by engaging government agencies, community groups, and fishers' associations. This participatory process integrated fishing, conservation, shipping, and tourism into a unified vision for sustainable ocean management [3].

Pair this approach with adaptive management practices that allow for ongoing performance monitoring and quick adjustments. A Sustainability Management System, featuring indicator matrices, can help track progress and refine strategies over time [2]. Such flexibility is crucial, as ocean conditions are constantly changing.

It's also important to mainstream biodiversity and ecosystem services into the objectives of other economic sectors. This ensures that shared resources are managed sustainably and that trade-offs are well-informed [10]. Early stakeholder engagement is critical to identify non-negotiable thresholds for resource use - limits that safeguard essential ecosystem functions even as economic development progresses [10].

"Sustainability and equity are two sides of the same coin" [3].

Finally, ensure that your adaptive management approach evaluates whether benefits are reaching marginalized groups, including women and Indigenous communities. These groups often bear the brunt of ocean-related activities while being excluded from their rewards. Addressing this imbalance is key to building an equitable Blue Economy.

Securing and Managing Financing for Blue Economy Projects

NGOs and nonprofits face a daunting $175 billion annual financing gap for advancing ocean sustainability [21]. To address this, combining diverse funding sources and creating sustainable financial systems is essential.

Blended Financing for Blue Economy Projects

Blended finance combines philanthropic grants with impact investments and concessional debt, aiming to reduce risks for commercial investors. Catalytic capital, such as grants for early-stage costs like legal structuring and business planning, plays a critical role in this process.

In October 2024, Blue Alliance and BNP Paribas introduced an impact loan facility focused on coral reef conservation. This initiative blended a $5.2 million grant from the Global Fund for Coral Reefs with impact loans from BNP Paribas. The program supports 1.7 million hectares of Marine Protected Areas across the Philippines, Tanzania, and Indonesia, fostering seven reef-positive businesses in ecotourism and aquaculture. By 2040, it aims to scale up to 70 million hectares and unlock $20 million in private investments [20][19].

"A multi-stakeholder approach is central to successful project development and management. This should include governments, engaged and experienced NGOs, and partners with skills in social entrepreneurship, financial planning, and marine conservation."

– Nicolas Pascal, Executive Director, Blue Alliance Marine Protected Areas [19]

Grants are often crucial for covering the initial management costs of Marine Protected Areas until revenue-generating ventures can sustain themselves.

Comparing Financing Options

Different financing mechanisms cater to various stages, scales, and risk tolerances of Blue Economy projects.

Conservation Trust Funds (CTFs) come in three forms:

Endowment funds: Invest capital and use interest earnings, ideal for long-term funding of no-take zones.

Sinking funds: Gradually spend down capital for time-bound projects.

Revolving funds: Replenish through taxes or fees, supporting ongoing coastal management.

Between 2009 and 2018, CTFs globally disbursed over $2 billion [22].

Debt-for-nature swaps restructure sovereign debt to fund conservation. For instance, Belize raised $364 million to pay off $546 million in old debt at a 45% discount, freeing up $180 million for marine conservation. Similarly, the Seychelles refinanced debt to secure protection for 32% of its waters (400,000 km²) by March 2020 [22].

Parametric insurance provides quick payouts after extreme weather events. Following Hurricane Delta in December 2020, Quintana Roo, Mexico, received $800,000 from a $3.8 million policy to fund coral reef restoration [22].

Mechanism | Primary Source | Risk Level | Best Use Case |

|---|---|---|---|

Grants | Philanthropy/Government | Low | Early-stage management and technical assistance [19] |

Impact Loans | Private Investors | Moderate | Scaling reef-positive businesses with proven models [19] |

Blue Bonds | Capital Markets | High | Large-scale national marine spatial planning [18] |

CTF Endowment | Philanthropy | Low | Perpetual funding for no-take zones [22] |

These mechanisms offer tailored solutions for building financial stability and advancing ocean conservation.

Building Financial Resilience

For NGOs and nonprofits, ensuring the long-term success of Blue Economy projects requires a mix of funding sources and proactive financial risk management. Pairing early-stage grants with revenue-generating reef-positive businesses creates more sustainable funding streams.

Establishing reliable baselines with measurable impact metrics and third-party monitoring is crucial. Data like fish biomass, carbon sequestration rates, and coral health assessments can boost donor and investor confidence. Frameworks such as the IFC Performance Standards or GIIN IRIS+ metrics ensure transparency in reporting [19].

Regional conservation trust funds, such as the Caribbean Biodiversity Fund, can streamline access to funding by reducing transaction costs and providing technical assistance [21].

"We need to step out of our investor, grant maker, policymaker, and practitioner siloes to continue these important conversations that create the enabling conditions to collaboratively mobilize resources to fill the gaps."

– Stacy Jupiter, Executive Director, WCS Global Marine Program [21]

Incorporating tools like parametric insurance protects coastal projects from climate-related risks, making them more appealing to cautious investors [20].

Investing in sustainable ocean solutions offers immense returns - every $1 invested can yield at least $5 in benefits by 2050 [23][24]. By diversifying funding strategies, organizations can transform short-term efforts into enduring conservation systems.

Monitoring, Scaling, and Sustaining Blue Economy Strategies

Monitoring progress is more than a checkpoint - it’s the foundation for creating scalable and adaptable strategies that support long-term ocean stewardship. By combining these efforts, NGOs and nonprofits can maintain effective Blue Economy strategies that align with sustainable development goals and promote fairness.

Establishing Monitoring and Evaluation Metrics

Tracking progress happens on three fronts: implementation (like spending and behavioral changes), environmental impact (such as biomass and carbon storage), and long-term socio-economic benefits (economic growth, food security, and equity) [26].

Metrics should go beyond financial results to include non-monetary benefits. For instance, calculate carbon stored in seagrass meadows and mangroves, measure storm protection offered by coastal wetlands, and assess pollution filtration services [2][26]. Success indicators might include reductions in plastic waste, nutrient runoff, and noise pollution [26]. Equity metrics are equally important - these assess whether marginalized groups are involved in decision-making and if Indigenous cultural heritage is safeguarded [3][26].

A practical example comes from The Ocean Foundation’s Sustainability Management System (SMS) for Fundación Tropicalia. This system enabled annual reporting on environmental, social, and economic progress through detailed indicator matrices, ensuring alignment with local socio-economic priorities [2].

"Meaningful blue economy investing must have real, measurable positive outcomes."

– Mark J. Spalding, President, The Ocean Foundation [26]

With well-defined metrics, organizations can confidently expand and sustain regenerative initiatives.

Scaling Successful Initiatives

Scaling efforts often transition from mitigation to full-scale ecosystem restoration. A standout example is the Great Blue Wall initiative, spearheaded by the IUCN and African partners. Launched in 2024, this project aims to protect 30% of the Western Indian Ocean - an area of roughly 772,000 square miles - by 2030. Its ambitious goals include sequestering 100 million tons of CO₂ and creating 2 million jobs through restored mangroves, seagrasses, and coral reefs [4].

Key to scaling is the use of blended finance models. These models combine philanthropic or grant funding to support early-stage reef-positive businesses until they can attract private investment [27]. When expanding to new regions, establishing local nonprofit entities is essential. These organizations collaborate with regional authorities, empowering communities to manage Marine Protected Areas while governments oversee regulations [27].

The Climate Sheroes project in Pakistan offers a powerful example of this approach. By involving over 500 women in mangrove restoration and management, the project linked ecological recovery with social equity. Local livelihoods were diversified through income generated from selling mangrove products, showcasing how scaling can balance environmental and social goals [4].

These initiatives highlight how scaling efforts can pave the way for adaptive management practices that ensure long-term success.

Ensuring Sustainability Through Adaptive Management

Sustainability hinges on continuous learning and adjustments informed by monitoring data. Implementation roadmaps are crucial - they outline specific actions, identify key stakeholders, and evaluate potential revenue alongside time commitments for each project [17]. Budgets should extend beyond standard funding cycles to account for shifting management costs and potential financing gaps over time [17].

A review of Ocean Panel countries revealed that 54% of ocean-related commitments have been completed, with 40% still in progress. This underscores the importance of systematic tracking and accountability [25]. Using a feasibility-versus-revenue matrix can help prioritize funding sources, ranging from philanthropic contributions to sustainable use levies, for short-, medium-, and long-term needs [17].

Adaptive management also involves addressing the true costs of harmful activities, such as plastic pollution and carbon emissions, to reduce financial risks [26]. Evaluating both economic returns and "ocean returns" - like biomass growth and carbon storage - ensures that strategies remain both financially viable and ecologically responsible [26]. Advances in technology, such as AI and satellite monitoring, now make it possible to track ecological changes in real time [4].

"We need to keep in mind what measurable outputs investors can deliver themselves, versus the outcomes that depend on others to occur... and we need to acknowledge our need to measure both."

– Mark J. Spalding, President, The Ocean Foundation [26]

Conclusion: Key Steps for Developing a Blue Economy Strategy

Creating a strong Blue Economy strategy means shifting focus from exploiting ocean resources to adopting regenerative practices that promote human well-being, ensure food security, and support sustainable livelihoods [2]. Start by assessing your internal capabilities, mapping out ocean resources, and identifying any existing gaps, as outlined in earlier sections. From there, craft Sustainable Ocean Plans that connect all sectors - conservation, fishing, shipping, tourism, and more - so that ocean management becomes holistic rather than fragmented [3].

Collaboration is essential. Build multi-stakeholder platforms that bring together scientists, industry leaders, policymakers, and local communities [5]. This approach goes beyond simply gathering input; it ensures decision-making is inclusive. As Micheline Khan and Eliza Northrop from the World Resources Institute state:

"Sustainability and equity are two sides of the same coin. Equity is a prerequisite for a sustainable ocean economy" [3].

Your funding strategy should combine various sources, such as philanthropic grants, concessional financing, and private investments. This blend supports both early-stage initiatives and long-term sustainability efforts while emphasizing non-market benefits like carbon storage, storm protection, and cultural heritage preservation [2]. Highlighting these values strengthens your case for funding and showcases meaningful impacts beyond financial gains.

Emerging technologies and data-driven tools can significantly enhance your efforts. Use innovations like IoT devices and satellite monitoring for real-time tracking of ecological changes [5]. Investing in ocean-related initiatives offers not only ecological benefits but also economic returns, with every $1 spent on key ocean actions generating at least $5 in global value [28].

Adopt flexible management practices that rely on continuous monitoring and timely adjustments. Align your strategy with global goals such as the UN Sustainable Development Goals and the Paris Agreement to ensure your work contributes to larger ocean stewardship objectives [5]. While the ocean economy demands substantial investment and long-term commitment, clear planning, inclusive governance, and innovative solutions can drive meaningful change for communities and ecosystems that depend on the ocean.

FAQs

What’s the difference between the Blue Economy and the ocean economy?

The ocean economy encompasses all industries and activities connected to the ocean, including shipping, fishing, and oil extraction, without necessarily considering their environmental impact. In contrast, the Blue Economy emphasizes the responsible and sustainable use of ocean resources. Its goal is to balance economic growth, support for livelihoods, and the preservation of marine ecosystems, ensuring the health of the oceans for future generations. While the ocean economy focuses broadly on economic activities, the Blue Economy prioritizes practices that safeguard marine environments.

How can our nonprofit measure “ocean returns” like carbon and biodiversity?

Nonprofits aiming to measure "ocean returns" - such as carbon storage and biodiversity - can rely on established frameworks and tools to guide their efforts. For carbon tracking, frameworks like the High-Quality Blue Carbon Principles and tools such as the Progress Wheel are invaluable. These resources help monitor carbon sequestration and evaluate overall ecosystem health.

When assessing biodiversity, focus on ecosystem services, including provisioning (resources like food and water), regulating (climate control and water purification), and cultural benefits (recreational and spiritual value). By aligning these metrics with widely recognized standards, your organization can ensure precise measurement and advance its blue economy objectives effectively.

Which funding option fits our project stage (grants, impact loans, blue bonds)?

Grants work well for early-stage efforts like managing Marine Protected Areas (MPAs) or building capacity. They help cover operational costs until the project can sustain itself financially. Impact loans, on the other hand, are geared toward ventures that have proven their viability and are ready to expand. These loans often fund activities such as enterprises that benefit reefs or initiatives supporting community livelihoods. For larger, well-established projects with steady revenue streams, blue bonds offer long-term funding, making them a strong option for scaling up significant initiatives.

Related Blog Posts

FAQ

01

What does it really mean to “redefine profit”?

02

What makes Council Fire different?

03

Who does Council Fire you work with?

04

What does working with Council Fire actually look like?

05

How does Council Fire help organizations turn big goals into action?

06

How does Council Fire define and measure success?

Mar 21, 2026

How to Develop a Blue Economy Strategy for NGOs & Nonprofits

Sustainability Strategy

In This Article

A practical framework for NGOs to assess readiness, map ocean assets, build partnerships, secure blended finance, and measure Blue Economy impact.

How to Develop a Blue Economy Strategy for NGOs & Nonprofits

The Blue Economy offers NGOs and nonprofits a chance to combine marine conservation with job creation and economic growth. With the ocean economy valued at $2.5 trillion annually, this approach supports livelihoods, strengthens climate resilience, and aligns with global sustainability goals like SDG 14 (Life Below Water) and SDG 13 (Climate Action).

To get started, organizations should:

Assess Readiness: Evaluate internal capacity, gender equity, and stakeholder engagement.

Map Ocean Assets: Identify resources like mangroves and fisheries, including their economic and non-economic value.

Address Gaps: Focus on areas like community inclusion, ocean health, and skilled personnel.

Build Partnerships: Collaborate with governments, private sectors, and local communities.

Secure Financing: Use grants, impact loans, and conservation funds to support projects.

Monitor Progress: Track outcomes like carbon storage, marine biodiversity, and community benefits.

6-Step Blue Economy Strategy Framework for NGOs and Nonprofits

Sustainable Blue Economy

Assessing Your Organization's Readiness for Blue Economy Work

Before diving into Blue Economy initiatives, it's crucial to evaluate your organization's current capabilities. This assessment ensures your operational strengths align with the strategic goals of the Blue Economy. Key areas to examine include internal capacity, engagement with marine ecosystems, and the need for partnerships.

Conducting an Internal Audit

Start by reviewing your organization's readiness using the Blue Economy Capacity Assessment Framework (BECF). This framework evaluates four key areas: Gender Equity (GE), Social License to Operate (SLO), Ocean Health Investment (OHI), and Highly Qualified Personnel (HQP) [9].

Ask yourself some essential questions during this audit. Does your team include individuals trained in ocean literacy and sustainable development? Women make up 85% of the global fisheries workforce, yet they are often underrepresented in leadership roles [3]. Assess whether your leadership promotes gender equity (aligned with SDG 5.5) and if decision-making processes are inclusive (SDG 16.7) [9].

"The blue economy should not be confused with the ocean economy which is measured in terms of the oceans-based industries' contribution to economic output and employment." - Ronnie Noonan-Birch et al., Frontiers in Marine Science [9]

Additionally, evaluate whether your operations prioritize decoupling economic growth from environmental harm, incorporating sustainability metrics (SDG 8.4 & SDG 12.6) [9]. A compelling example of this is The Ocean Foundation's collaboration with Fundación Tropicalia in the Dominican Republic. By developing a Sustainability Management System rooted in UN Global Compact principles and Global Reporting Initiative guidelines, the organization produced five consecutive sustainability reports that documented its adherence to Blue Economy principles [2].

Lastly, consider your ability to engage stakeholders. Securing a "Social License to Operate" requires ongoing approval from local communities impacted by marine projects [9].

This internal review lays the groundwork for mapping your organization's ocean-related assets.

Mapping Ocean-Dependent Assets

Understanding your organization's reliance on ocean resources involves identifying both market and non-market values. While the global ocean economy generates approximately $2.3 trillion annually from market goods [11], it's equally important to account for non-market benefits like carbon sequestration from seagrass and mangroves, storm resilience, and the cultural connections tied to marine ecosystems [11][2].

Tools like Geographic Information Systems (GIS) and environmental assessments can help determine the quality and availability of data for your planning efforts [10]. For instance, in the Caribbean, where over 90% of economies depend directly on the ocean [7], mapping becomes a critical step. Make sure to include marginalized groups, women, and Indigenous communities in your stakeholder analysis to build genuine social license rather than superficial sustainability claims [9][3].

Rhode Island provides a useful example. The state's Blue Economy accounts for 8.8% of its GDP, supporting over 36,500 jobs across industries like defense ($3.16 billion), marine trades ($1.45 billion), and fisheries ($151.5 million) [6]. By conducting thorough mapping, Rhode Island identified specific opportunities and gaps across various marine sectors.

Early stakeholder engagement is essential for defining mandatory standards for resource use and conservation [10]. A notable example is The Ocean Foundation's 2017 training for Philippine government officials. This initiative prepared the country for its ASEAN chairmanship by focusing on sustainable Blue Economy practices and financing coastal and marine resources. The training enabled officials to identify regulatory gaps and establish a cohesive approach to marine resource management [2].

Use these mapped assets to uncover areas where your strategy can be refined.

Identifying Gaps and Opportunities

Building on the insights from your audit and asset mapping, conduct a "Blue Shortcoming" assessment to identify areas for improvement across the four BECF categories [9].

Assessment Area | Key Focus | Strategic Value |

|---|---|---|

Gender Equity (GE) | Leadership roles and women’s participation | Enhances profitability and productivity [9] |

Social License (SLO) | Community acceptance and stakeholder buy-in | Ensures project viability and reduces political risks [9] |

Ocean Health (OHI) | Protection of carbon sinks and habitats | Safeguards critical ecosystem assets driving the economy [9][2] |

Qualified Personnel (HQP) | Skills in sustainability and innovation | Attracts investment and fosters innovation [9] |

In fiscal year 2024, the PROBLUE multi-donor trust fund approved 64 technical assistance proposals totaling $37.8 million [8]. Accessing such resources requires demonstrating strong capacity in these assessment areas.

Your gap analysis should also evaluate your organization's digital readiness. Are you equipped to use tools like the "Aquaculture Digital Roadmap" to enhance marine resource management efficiency? [8] Can you implement Marine Spatial Planning (MSP) to reduce investment risks and improve access to marine resources? [10]

Finally, ensure that Indigenous and local knowledge systems are not just consulted but actively integrated into your governance and scientific practices [9][3]. This approach is essential for achieving equity, a cornerstone of sustainable Blue Economy strategies.

"Equity is a prerequisite for a sustainable ocean economy, where humanity safeguards marine and coastal ecosystems, sustainably uses ocean resources, and ensures equitable distribution of benefits." - Micheline Khan and Eliza Northrop, World Resources Institute [3]

Building Partnerships for Blue Economy Success

Creating successful strategies for the Blue Economy hinges on forging partnerships across various sectors. These collaborations lay the groundwork for effective governance and networking in Blue Economy initiatives.

Engaging Stakeholders Across Sectors

The first step is identifying the right stakeholders. A comprehensive stakeholder map should include:

Public sector: For regulatory guidance and policy alignment.

Private sector: To drive investment and innovation.

Civil society organizations: For community engagement and advocacy.

Financial institutions: To manage investment risks.

Academic partners: For research and technical insights.

A great example of this multi-sector approach is the partnership between the Global Green Growth Institute (GGGI) and the Caribbean Biodiversity Fund (CBF), formed in September 2025. This collaboration, led by CBF CEO Karen McDonald Gayle and GGGI Representative Daniel Muñoz-Smith, aims to unlock funding for coastal restoration in the Caribbean. So far, the CBF has supported over 100 projects across 12 countries, with more than $30 million in funding provided [7].

"This partnership with GGGI empowers us to turn ambition into action, unlocking finance for communities to restore coastal ecosystems, protect biodiversity, and build resilient livelihoods that sustain us all" [7].

Inclusive planning is key. Ensure Indigenous leaders, women, and marginalized groups are part of the decision-making process. This not only promotes fairness but also strengthens local support and regulatory compliance. Stakeholders should work together on a unified plan that balances competing interests like fishing, conservation, shipping, and tourism [3].

When working with private sector partners, consider teaming up with multilateral development banks and insurers to reduce risks through tools like concessional financing and first-loss guarantees [12]. Additionally, identifying "industry clusters" - geographical hubs of interconnected businesses - can help locate infrastructure and research collaborators [6].

Once stakeholder engagement is in place, the next step is establishing a governance framework to ensure these partnerships thrive.

Establishing Governance Frameworks

Governance structures are critical for turning collaboration into results. A strong governance framework should be inclusive, adaptive, accountable, and transparent [1]. This involves creating decision-making processes that involve all relevant local stakeholders, particularly those whose livelihoods depend on marine resources.

Area-based decision platforms can align human and natural resources at the local level [5]. These platforms streamline public and private investments while ensuring ecosystem restoration remains a priority in economic development.

Align governance efforts with international agreements like the UN 2030 Agenda for Sustainable Development and the Paris Agreement. Regional strategies, such as the African Union Blue Economy Strategy, also provide useful blueprints [5]. Indigenous organizations should be granted permanent status and full consultation rights, as seen in the Arctic Council model [3]. This approach ensures Indigenous communities have a genuine role in strategic decision-making [15].

Adopting policies that recognize a clean and sustainable environment as a human right provides a legal framework for protecting communities from environmental harm. This rights-based approach also enhances accountability in partnerships [3].

Leveraging Existing Alliances and Networks

Established networks can amplify the impact of your partnerships and governance structures. Global coalitions like the Blue Prosperity Coalition bring technical expertise and assist governments in implementing sustainable ocean plans across their waters [13]. Regional groups, such as the Northeast Regional Ocean Council (NROC), enable organizations to align objectives, share data, and combine resources for Blue Economy projects [14].

The World Bank's PROBLUE program is another valuable resource. In fiscal year 2024, it approved 64 proposals worth $37.8 million, supporting technical work in over 100 economies [8]. One standout initiative is the "Unleashing the Blue Economy of the Caribbean" (UBEC) project, a $90 million program launched in November 2024. This project, funded by the World Bank and PROBLUE, focuses on empowering women entrepreneurs in the Blue Economy sector [8].

Engaging with international bodies like the Commonwealth Blue Charter or the High-Level Panel for a Sustainable Ocean Economy can help shape global standards for sustainable ocean practices [2]. Using standardized ocean accounting frameworks enables reliable data collection on ecosystem services, which is essential for reducing investment risks and supporting blended finance approaches [16]. When working with data related to Indigenous waters, adhere to the CARE Principles (Collective benefit, Authority to control, Responsibility, Ethics) to ensure Indigenous communities maintain control over their data [15].

Finally, innovation hubs like Blue Tech Week and OceanHub Africa offer opportunities to connect with startups and technologies focused on sustainable ocean use. These platforms foster collaboration and provide access to cutting-edge solutions for tackling shared challenges.

Developing and Implementing Your Blue Economy Strategy

Once partnerships and governance structures are in place, the next step is crafting a strategy that delivers measurable outcomes. The focus should shift from traditional "ocean business" models to regenerative practices that restore ecosystems while supporting sustainable livelihoods [2].

Mapping Ocean Wealth and Setting Goals

Start by using your mapped ocean-dependent assets to establish measurable and integrated targets. This involves collecting both quantitative data - such as the current value of marine activities, resource availability, and funding levels - and qualitative insights, including community interests, iconic features, and political support [17].

"We see value in an economy that has restorative activities. One that can lead to enhanced human health and well-being, including food security and the creation of sustainable livelihoods" [2].